1. Digital Economy – The new Economy

'Digital Economy' is based on digital computing technologies. It constitutes of various evolving business models such as e-commerce, online advertising, app stores, online payments modes and social media. India is one of the fastest growing e-commerce markets in the world, home to some of the giant players such as Flipkart, Paytm, Amazon, etc. What makes it successful? - advanced, evolving, inexpensive and accessible connectivity and technology solutions, which are the main enablers for the global success of this industry and increasing popularity of digital economy, challenging international physical borders and outpacing the principles of traditional economy.

2. Taxing the Digital world – Need for change

Consider an e-commerce giant, headquartered abroad and operating e-commerce websites across countries, including India. In India, the e-commerce company interacts with sellers and consumers digitally, over e-mails, website and other digital means, without maintaining any physical presence in India.

An Indian trader enters into an agreement with the Company for advertising his products, as a measure to boost sales. In view of the provisions of the domestic tax laws and tax treaties, the advertisement and sales facilitation revenue earned by the foreign e-commerce company may not be subject to tax in India, as it does not have any physical presence in India, thus resulting in a loss of tax revenue for the Indian government.

Now, contemplate, that the foreign e-commerce company routes its transactions through a low-tax jurisdiction, i.e. where the corporate tax rate is low or nil, as compared to other jurisdictions. This may lead to double non-taxation, as income is neither taxable in the source country, nor in the country of residence.

Therefore, it is apparent that where the existing global tax policies, essentially crafted for the traditional economy, are applied to the digital economy, it may lead to non-taxation of income, due to base shifting and jurisdictional arbitrage or in simple words profit shifting.

In view of the increasing role of digital economy globally, a paradigm shift in the international tax policies was the need of the hour. This would bring equilibrium on the tax front and empower nations to collect their legitimate share of taxes.

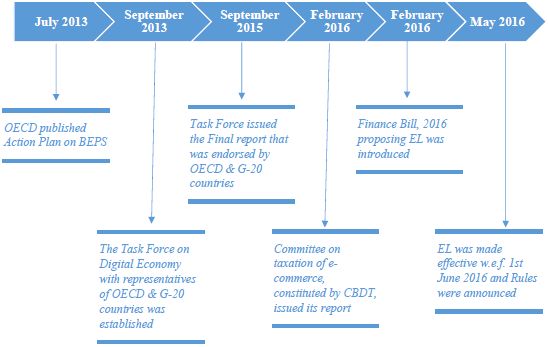

3. Genesis of Equalisation Levy – India's Google tax

4. Developments in India – Some judicial precedents

The Indian tax authorities have been grappling to tax the income of companies engaged in provision of digital advertising space for online advertisement much before the OECD and G-20 members joined hands to find ways and means to tackle the issue of income going untaxed in such cases.

In the year 2011, the Mumbai Bench of the Tribunal in the case of Yahoo India (P) Ltd vs DCIT: 140 TTJ 195 held the payment made by assessee to Yahoo Holdings Hong Kong Ltd ('YHHL'), for the services rendered for uploading and display of banner advertisement of the Department of Tourism of India, on its portal, was not in the nature of royalty as defined in the Indian Income tax Act. The Tribunal held the consideration received by YHHL to be in the nature of business profit and in the absence of any PE of YHHL in India, it was held to be not chargeable to tax in India.

Likewise, in ITO vs Pubmatic India (P) Ltd: 60 SOT 54, the Mumbai Bench of the Tribunal held remittance made to a US company towards purchase of advertisement space fell under Article 7 of India-USA DTAA and in absence of a PE of such company in India, income was not taxable in India.

It was held similarly by the Mumbai Bench of the Tribunal in Pinstorm Technologies (P) Ltd vs. ITO: (2012) 154 TTJ 173 and eBay International AG vs. DDIT: (2012) 151 TTJ 769.

In the case of ITO vs. Right Florists: 154 TTJ 142 before the Kolkata Bench of the Tribunal, the assessee, a florist carrying out business in India, for the purpose of generating business used online advertisement services of Google Ireland and Yahoo USA. Whenever anyone does a web search on the respective search engines for a particular website/ service and uses certain keywords, the advertisement of assessee was shown along with the searched results. During the relevant year, the assessee made payments to Google Ireland and Yahoo USA for such advertisement display services without deducting tax at source on the understanding that these entities did not have a PE in India. During the assessment proceedings, the AO disallowed business deduction of payments made to Google Ireland and Yahoo USA on the ground that payment for the aforesaid online advertisement services was taxable and the assessee was required to withhold tax therefrom, which it failed to do. On appeal, the CIT(A) deleted the disallowance made by the AO and held that in absence of PE of Google Ireland and Yahoo USA such payments were not taxable and accordingly assessee was not under any obligation to deduct tax at source.

Placing reliance on Mumbai Tribunal's order in case of Yahoo India and Pinstorm Technologies (supra), the Tribunal held that payments made for online advertisement was not in the nature of 'royalty' both under the Income tax Act and the relevant Double Tax Avoidance Treaty. Relying on OECD Commentary, the Tribunal further observed that a search engine which only has presence by way of a website cannot be held as PE unless its servers are located in same jurisdiction. As regards "business connection", the Tribunal held that there is nothing on record to demonstrate or suggest that the online advertising revenues generated in India were supported by/ serviced by/ connected with any entity based in India. It was further held that in absence of human intervention/ element in rendering such advertisement services, the payments made to Google Ireland and Yahoo US could also not be taxed as 'fee for technical services'.

As would be observed, the attempts of the Indian Revenue to bring to tax payments for online advertisers within the ambit of tax by applying the existing provisions of the Indian Income tax Act and the Double Tax Treaty, were not successful before the Tax Tribunals. Similar challenges were faced by other countries as well. A new law or levy approach was thus required to bring such payment to tax.

5. BEPS Action Plan 1 - New international tax practices for the Digital Economy

The OECD, an international economic organization, has sought to address the tax challenges of the Digital Economy in its Action Plan 1 of the Final Report on 'Base Erosion and Profit Shifting' (BEPS). The reason why OECD sought to address these issues was in response to growing concerns raised by political leaders, media outlets and civil society around the world about tax planning by multinational enterprises that makes use of gaps in current tax laws to artificially reduce their tax liabilities.

BEPS Action Plan 1 identifies and analyses various tax models in relation to transactions in the Digital Economy, such as modification to 'Permanent Establishment (PE) related Rules to include significant economic presence, withholding tax on digital transactions and equalisation levy — similar to withholding taxes.

OECD in its Final Report on "Addressing the Tax challenges of the Digital Economy", has stated as under:

"Broader tax challenges raised by the digital economy

...........

- None of the other options analysed by the TFDE, namely (i) a new nexus in the form of a significant economic presence, (ii) a withholding tax on certain types of digital transactions, and (iii) an equalisation levy, were recommended at this stage. This is because, among other reasons, it is expected that the measures developed in the BEPS Project will have a substantial impact on BEPS issues previously identified in the digital economy, that certain BEPS measures will mitigate some aspects of the broader tax challenges, and that consumption taxes will be levied effectively in the market country.

- Countries could, however, introduce any of these three options in their domestic laws as additional safeguards against BEPS, provided they respect existing treaty obligations, or in their bilateral tax treaties. Adoption as domestic law measures would require further calibration of the options in order to provide additional clarity about the details, as well as some adaptation to ensure consistency with existing international legal commitments.

...............

276. .............In this context, the application of a withholding tax on digital transactions could be considered as a tool to enforce compliance with net taxation based on this potential new nexus, while an equalisation levy could be considered as an alternative to overcome the difficulties raised by the attribution of income to the new nexus.

7.6.4. Introducing an "equalisation levy"

302. To avoid some of the difficulties arising from creating new profit attribution rules for purposes of a nexus based on significant economic presence, an "equalisation levy" could be considered as an alternative way to address the broader direct tax challenges of the digital economy. This approach has been used by some countries in order to ensure equal treatment of foreign and domestic suppliers. ........

..................."

6. India adopts Equalisation Levy....

In light of the aforesaid developments, the Central Board of Direct Tax (CBDT), had constituted a 'Committee for Taxation of E-commerce Transactions' to suggest an appropriate mechanism, for taxation of e-commerce transactions. The Committee, taking into consideration the BEPS Action Plan 1, suggested adoption of a new levy, viz., 'Equalisation Levy', which is independent of the domestic income tax provisions. The equalisation levy was thus introduced through the Finance Act, 2016 and was made applicable w.e.f. 1st June 2016.

7. Equalisation Levy – Salient features

|

Chargeability [section 165(1) of Finance Act, 2016] |

Equalisation levy is to be deducted @6% on amount paid to a non-resident, not having a PE in India for "specified services" |

| Specified

services [section 164 - clause (i)] |

|

|

Payer [section 165(1)] |

|

|

Exclusions [section 165(2)] |

|

| Payment due

date [section 166(2)] |

7th day of the immediately following month |

| Requirement to

furnish statement of specified service [section 167] |

|

| Manner of

processing of statements [section 168] |

|

| Rectification of mistake

apparent from record [section 169] |

|

|

Non-compliance [section 170-172] |

|

| Appeal to

CIT(A) [section 174] |

|

| Appeal to

Tribunal [section 175] |

|

| Amendments made in the Income tax Act, 1961 | |

| Exclusion from total income | Income subject to EL shall not be included in total income of the payee in terms of section 10(50) of the Income tax Act |

| Deductibility of expenses | New sub-clause (ib) has been inserted in section 40(a) of the Income tax Act as per which the consideration paid for specified service on which EL was leviable would not be deductible if EL has not been deducted or after deduction, not been paid before the due date of filing the return of income. Deduction may, however, be claimed in the year in which EL is deducted/ paid. |

8. Equalisation Levy Rules, 2016

CBDT issued Equalisation Levy Rules vide Notification dated 27th May, 2016. A brief snapshot of the Rules, which provides the procedural framework for the compliances to be undertaken and appeal process, is given below:

| Particulars | Section | Rule | Description |

| Payment of EL | 166 | 4 |

|

| Furnishing of statement of specified services/ annual return | 167 | 5 & 6 |

|

| Processing of statement of specified services | 168 | 7 |

|

| Filing appeal with the CIT(A) | 174 | 8 |

|

| Filing appeal with the ITAT | 175 | 9 |

|

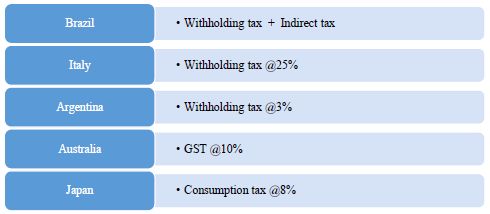

9. Development in other countries

With the introduction of equalisation levy, India joins the ranks of the below mentioned countries who have introduced taxes on digital transactions.

10. Some debatable issues

The introduction of equalisation levy raise various issues, some of which are as follows:

- Since the conditions relating to

income accruing or arising in India are not mentioned in the

provisions relating to EL, following issues may arise:

- Whether EL will apply on payment made

by a branch of an Indian entity based outside India to a

non-resident?

Ans.: May be levied since payment is being made by a resident to a non-resident. No exemption has been provided for services used outside India - Whether EL will apply on payment by a

head office of a foreign company (having a PE in India) for its

overseas business?

Ans.: May not be levied due to absence of territorial nexus with India

- Whether EL will apply on payment made

by a branch of an Indian entity based outside India to a

non-resident?

- Whether the threshold limit of Rs.

1,00,000 is applicable with reference to the payer or payee?

Ans.: In terms of section 165(2)(b) and section 166(1), it appears that the threshold of Rs. 1,00,000 shall have to be seen qua each payee, each payer vis-à-vis each payee in each financial year. - Whether exemption under section

10(50) of the Income tax Act will be available in cases where EL is

not charged by virtue of payment falling below the exemption

threshold?

Ans.: No, since such consideration/ income will not be chargeable to EL under Chapter VII. Normal provisions of the Act or DTAA should apply in those cases. - Whether surcharge and/ or education

cess would apply on EL?

Ans.: EL rate should not be increased by surcharge or education cess in absence of any such provision. - What would be the plausible course of

action in the absence of any appeal remedy provided against the

intimation issued under section 168?

Ans.: The assessee may approach the High Court by way of writ petition. - Whether EL would apply on composite

contracts wherein payment is made for multiple purposes, i.e., for

online advertisement and non-advertisement purpose?

Ans.: In case of composite contracts, payer shall have to make a fair and reasonable allocation of the consideration for determining which part is liable for EL. - Where EL has to be borne by the

payer, whether the levy has to be grossed up?

Ans.: Chapter VIII does not prescribe any requirement of grossing up of EL similar to the requirement for grossing up of tax provided in section 195A of the Income tax Act. However, it would be advisable to gross up the levy @6.383% where contractually the entire sum is required to be remitted. Else, there may be an issue as regards allowability of deduction under section 40(a)(ib) of the Income tax Act, considering that EL is treated as per law to be a 'deduction'. - Whether deduction would be allowed in

respect of EL borne by the payer?

Ans.: Yes, it should be treated as an allowable expenditure and the amount of EL forming part of the grossed up amount should not be subject to disallowance under section 40(a)(ii) of the Act. - What would be the recourse in a

situation where EL is deducted on the presumption that the payee

does not have a PE in India but payee is held to have PE by the

Revenue and above income is found to be effectively connected to

such PE?

Ans.: Unfortunately, there is at present no mechanism for seeking set off/ credit of EL against tax paid on PE's income and this may lead to excess tax payment. - Whether a tax treaty would apply in

cases that are subjected to EL?

Ans.: No, unless Article 2 (taxes covered) specifically includes such levy within its scope. - Whether the payee or the payer can

approach the Authority for Advance Rulings to ascertain the

liability of EL?

Ans.: The non-resident payee can explore the option of approaching the Authority by raising the question of availability of exemption under section 10(50) of the Income tax Act. - What is the scope of PE definition

provided in section 164(g)?

Ans.: The definition provided in clause (g) of section 164 is identical to the definition of PE provided in section 92F(iiia) of the Income tax Act.

The Supreme Court in the case of DIT (International Tax) vs. Morgan Stanley & Co: 292 ITR 416 explained the difference between the definitions of PE under the Income tax Act and the DTAA as follows:

"However, vide Finance Act, 2002 the definition of PE was inserted in the Income tax Act, 1961 (for short, 'IT Act') vide section 92F(iiia) which states that the PE shall include a fixed place of business through which the business of the MNE is wholly or partly carried on. This is where the difference lies between the definition of the word PE in the inclusive sense under the Income tax Act as against the definition of the word PE in the exhaustive sense under the DTAA. This analysis is important because it indicates the intention of the Parliament in adopting an inclusive definition of PE so as to cover service PE, agency PE, software PE, Construction PE etc."

On the basis of the observations made by the apex Court on the scope of the term "permanent establishment" w.r.t. identical definition given under the Income tax Act, it will be reasonable to argue that definition of PE in section 164(g) is confined not only to fixed place PE but would also include other forms of PE, such as Service PE, Agency PE, Construction PE, etc. - Whether the payer will be entitled to

interest on refund of EL claimed in the annual statement?

Ans.: Presently, there is no provision for interest on such refund - Whether the non-resident payee would

be subjected to MAT liability in respect of income on which EL

applies?

Ans.: As per Explanation 4 to section 115JB of the Income tax Act, MAT is not applicable to foreign companies not having place of business / PE in India, therefore in such cases MAT would not apply even if the non-resident payee is in receipt of any income from specified services. However, in a situation where the non-resident payee has a PE in India and income from specified services is not effectively connected with such PE, such income would be exempt under section 10(50) of the Income tax Act. By applying clause (ii) of Explanation 1 to section 115JB(2), income exempt under section 10 of the Income tax Act [other than arising under section 10(38)] is to be reduced from book profit and consequently MAT provisions would not apply in such cases too.

11. The Way Forward

The digital economy is evolving rapidly. It is imperative that international tax policies/ provisions keep pace with these developments in order to ensure that there is no loss of tax revenues as a whole merely because tax laws/ concepts made for brick and mortar economy cannot be applied to the digital economy.

In India, the introduction of Equalisation Levy, in relation to online advertisements is a first step towards taxation of the digital economy. It is expected that in the times to come the scope of such levy will be expanded to include other online / electronic transactions.

However, in order that equalisation levy does not result in increasing the transaction cost for Indian businesses, the Indian Government should evolve a mechanism whereby the non-resident payee of income can avail credit of such levy. Also, it would help businesses if CBDT were to clarify the various issues raised hereinabove in relation to applicability / procedure/ mechanism of levy of equalisation levy.

© 2016, Vaish Associates Advocates,

All rights reserved

Advocates, 1st & 11th Floors, Mohan Dev Building 13, Tolstoy

Marg New Delhi-110001 (India).

The content of this article is intended to provide a general guide to the subject matter. Specialist professional advice should be sought about your specific circumstances. The views expressed in this article are solely of the authors of this article.