AN INTRODUCTION

With a view to provide an internationally competitive environment for exports, the Government of India announced the SEZ Policy in April, 2000. The objectives of the SEZ Policy include making available goods and services free of taxes and duties supported by integrated infrastructure for export production, expeditious and single window approval mechanism and a package of incentives to attract foreign and domestic investments for promoting export-led growth.

SEZs in India functioned from November 1, 2000 to February 9, 2006 under the provisions of the Exim Policy/ Foreign Trade Policy and fiscal incentives were made available through the provisions of relevant statutes. This system did not lend enough confidence for investors to commit substantial investment for development of infrastructure and for setting up of the Units for export of goods and services.

In order to give a long-term and stable policy framework with minimum regulatory regime and to provide expeditious and single window clearance mechanism in line with international best business practices, a Central Act for Special Economic Zones was, therefore, found to be necessary.

The Special Economic Zones Act, 2005 ("SEZ Act") was enacted by the Government in 2005. Subsequently, the Special Economic Zones Rules, 2006 ("SEZ Rules") were notified on February 10, 2006, from which date, the SEZ Act comes into operation. The SEZ Policy provides for simplified procedures and single window clearance mechanism to deal with matters under Central/ State enactments. For SEZ developers, different minimum land requirement for different class of SEZs. Every SEZ is divided into a processing area, within which only the SEZ units would come up, and the non-processing area where the supporting infrastructure is to be created.

Salient features of the SEZ Policy

- Simplified procedures for development, operation, and maintenance of the SEZs and for setting up units and conducting business in SEZs;

- Single window clearance for setting up of an SEZ;

- Single window clearance for setting up Units in an SEZ;

- Single window clearance on matters relating to Central as well as State Governments;

- Simplified compliance procedures and documentation with an emphasis on self certification.

Minimum investment/ Net-worth criteria for setting up Special Economic Zone

Minimum investment or Net-worth of the Promoters, all group companies and flagship companies should be as under:

- Multi-Product SEZs - Minimum investment of INR 1,000 crores or Networth of INR 250 crores

- Sector specific SEZs - Minimum investment of INR 250 crores or Networth of INR 50 crores

Administrative set up

- The functioning of the SEZs is governed by a three tier administrative set up. The Board of Approval ("BOA") is the apex body and is headed by the Secretary, Department of Commerce, Ministry of Commerce and Industry, Government of India. The Unit Approval Committee ("UAC") at the Zone level deals with approval of units in the SEZs and other related issues. Each Zone is headed by a Development Commissioner, who is ex-officio chairperson of the UAC.

- Once an SEZ has been approved by the Board of Approval and Central Government has notified the area of the SEZ, Units are allowed to be set up in the SEZ. All the proposals for setting up of units in the SEZ are approved at the Zone level by the Approval Committee consisting of Development Commissioner, Customs Authorities and representatives of State Government.

Setting up of SEZ - Flow chart

Setting up of SEZ Unit - Flow chart

Online filing facility for SEZ proposals

- The Ministry of Commerce and Industry, Department of Commerce

has announced the online filing of SEZ proposals vide Circular F.

No. D.12/13/2008- SEZ dated October 21, 2008. The following online

services are offered through the "SEZ online" at http://

www.sezindia.nic.in/

- Filing of application (Form A) for setting up SEZ.

- Filing of other requests viz. Application for authorized operations, addition of co-developer, application for conversion of in-principle approval to formal approval, application for validity extension of approvals, change in developing entity, change in sector, change in area/ location, land details.

- Inbuilt e-mail box for each developer/ co-developer to enable it to communicate with the Department.

- Online status of requests.

- It may be noted that for filing of new applications, a physical copy of the complete application form after due signatures and authentication has to be submitted along with necessary enclosures.

Fiscal Incentives to SEZ Developers/ Units

| Particulars | Developers/ Co-developers | SEZ Units |

| Development Stage (Capital Goods, Consumables, Components & Spares) & Operation Stage (Raw Materials, Consumables, Components & Spares) |

|

|

| Profit Stage |

|

|

Obligations of SEZ Units

- SEZ Units to achieve positive Net Foreign Exchange ("NFE") in accordance with the formula provided under rule 53 of SEZ Rules, 2006.

- Units required to execute Bond-cum-Legal Undertaking and submit to the Development Commissioner in the prescribed Form-H under SEZ Rules, 2006.

- Unit to submit Annual Performance Report to the Development Commissioner, in the prescribed Form-I under SEZ Rules, 2006.

- Units to abide by local laws, rules, regulations or bye-laws with regard to the area planning, sewerage disposal, pollution control and the like.

- Units to comply with Industrial and Labour Laws, as are applicable locally. It may be noted that the labour laws will apply to all the Units inside the SEZ. However, the respective State Governments may declare Units within the SEZ as public utilities and may delegate the powers of Labour Commissioner to the Development Commissioner of the SEZs.

To sum up...

The SEZ scheme has generated tremendous response from the investors, both in India and abroad. The SEZ scheme generated domestic and foreign investment to the tune of INR 2,36,716 Crore (as of March 31, 2013):

Further, the exports from SEZs have also shown robust growth year after year. The value of physical exports during last three years is as under:

| Export from Special Economic Zones | |||

| Year | Physical Exports from SEZs (in INR – Crores) | Physical Exports from SEZs (in USD – Million)* | Growth rate (over the previous year) |

| 2012-13 | 4,76,159 | 87,546 | 31% |

| 2011-02 | 3,64,478 | 68,769 | 15% |

| 2010-11 | 3,15,868 | 65,806 | 43% |

| 2009-10 | 2,20,711 | 46,521 | 121% |

| 2008-09 | 99,689 | 21,675 | 50% |

| 2007-08 | 66,638 | 16,560 | 93% |

| 2006-07 | 34,787 | 7,629 | 51% |

* Source: EPCES Annual Report

The above facts and statistics endorse the success story of Indian SEZs. In the time to come, the SEZs are going to be biggest growth drivers of Indian economy.

BENEFITS OF SEZ UNIT OVER DTA UNIT

| Description | SEZ Unit | DTA Unit |

| Imports and Exports | License not required for import | License required for import under the provisions of Foreign Trade Policy. |

| All imports on self certification | Imports subject to attestation by customs authorities | |

| No routine examination of export/ import cargo by customs authorities | Unlike SEZ Unit, DTA unit is subject to routine examination by customs authorities | |

| Central Sales Tax | Exemption from Central Sales Tax | Central Sales Tax payable |

| Service Tax | Exemption/ refund of Service tax | Service Tax payable. CENVAT credit available |

| Central Excise | Exemption from central excise on procurement of capital goods, raw materials, consumable spares etc. from the domestic market | Excise duty payable |

| Income Tax | 15-years tax holiday in a phased manner subject to certain conditions. 100% income tax exemption under section 10AA of the Income-tax Act, 1961 for the first 5- years, 50% for the next 5-years and thereafter 50% of the ploughed back export profits for next 5- years. | Income Tax payable |

| Capital gains arising on transfer of assets (machinery, plant, building, land or any rights in buildings or land) on shifting of the industrial undertaking from an urban area to SEZ would be exempt from capital gains tax. The exemption would however be allowed subject to fulfilment of prescribed conditions in this regard. | Chargeable to capital gains tax. | |

| FDI/ FEMA | External Commercial Borrowing (ECB) by SEZ units upto USD 500 million in a year under Automatic Route without any maturity restriction. | Subject to maturity restrictions |

| Stamp duty exemption | Instruments executed by or on behalf of or in favor of the developer or units are exempt from stamp duty | No such exemption |

| Single Window clearance | Single window clearance mechanism to facilitate speedy implementation of SEZ projects | No single window clearance mechanism in place. Subject to lengthy and time taking procedure |

RECENT POLICY REFORMS - SEZS BACK ON GOVERNMENT'S RADAR

The Government is aware that SEZs hold tremendous potential to promote export from India. Presently, 577 formal approvals have been granted for setting up of SEZs, out of which 389 SEZs stand notified and 170 SEZs have become operational. Over INR 2.36 lakh crore have been invested in the Indian SEZs and direct employment of over one million persons has been generated in the SEZs. During the financial year 2012-13, total exports to the tune of INR 4.76 lakh crore have been made from the SEZs, registering a growth of about 31% over the exports for the year 2011-12.

Recently the Government has introduced various measures to give a fillip to SEZ policy reforms. On April 18, 2013, the Commerce Minister while releasing the Annual Supplement 2013-14 to the Foreign Trade Policy 2009-14 made various policy announcements to revive investors' interest in the SEZs. Subsequently, vide notification dated August 12, 2013, SEZ (Amendment) Rules, 2013 have been notified by the Government, thereby implementing the said policy announcements.

The following table provides an analysis of the amendments introduced by SEZ (Amendment) Rules, 2013, effective from August 12, 2013.

| Particulars | Earlier Position | Revised Position | Reason |

| Reduction in minimum land area requirement for setting up of multiproduct and sector specific SEZs |

|

|

In view of acute difficulties being faced by the developers in aggregating large tracts of uncultivable land for setting up SEZs, which is vacant and contiguous, it has been decided to reduce the minimum land area requirement by half for multiproduct and sector specific SEZs. |

| Minimum land requirement for IT/ ITES sector | Minimum land area requirement of 10 hectares + Minimum built-up area requirement of 100,000 sq. mtrs. |

|

IT

Exports constitute a significant part of India's exports and

IT/ ITES SEZs have a major contribution in it. Exports from IT/

ITES SEZs during financial year 2012-13 have exceeded INR 1.40 lakh

crore registering a growth of over 70% over the previous year's

exports. To specifically address the issues to boost growth of this important sector and to give a fillip to employment and growth in Tier-II and Tier-III cities, the present requirement of 10 hectares of minimum land area is being done away with. Accordingly, there would be no minimum land area requirement for setting up an IT/ITES SEZ. Only the minimum built up area criteria would be required to be met by the SEZ developers. |

| Broad banding of a sector specific SEZ on the basis of Graded scale for minimum land criteria | No such provision. | The concept of Graded Scale for minimum land criteria introduced, which would permit a SEZ an additional sector for each contiguous 50 hectare parcel of land. | To

provide greater flexibility in utilizing land tracts falling

between 50 to 450 hectares, it has been decided to introduce a

Graded Scale for Minimum Land Criteria which would permit a SEZ an

additional sector for each contiguous 50 hectare parcel of

land. This proposal will enable more efficient use of the infrastructure facilities created in such an SEZ. |

| Sectoral broad banding (within the same sector) | Sector

specific SEZ generally are not allowed to setup additional units in

similar/ related areas under the same sector unless specifically

mentioned in the letter of approval issued to the developer. Decisions are being taken by the appropriate authority on the facts and merits of each case. |

Setting-up additional units in similar/ related areas under the

same sector in a sector specific SEZ has been allowed. Accordingly, various categories comprising their respective products or services, similar or compatible with each other, including related ancillary services and R&D services of the sector and additional combination of products and services of a similar or compatible nature as approved by the board of approval shall constitute a single sector |

To provide flexibility to setup additional units in a sector specific SEZ is being provided by introducing Sectoral broad banding to encompass similar/ related areas under the same sector. |

| Criteria for 'vacant land' | For vacancy of land, the earlier policy allowed the parcels of land with preexisting structures not in commercial use to be considered as vacant land for the purpose of notifying an SEZ. | The

amendment permits preexisting structures (even though in commercial

use) to be considered as 'vacant land' for the purpose of

notifying an SEZ. Further, the additions to such pre-existing structures and activities being undertaken after notification would be eligible for duty benefits similar to any other activity in the SEZ. |

Additions to such pre-existing structures and activities being

undertaken after notification would be eligible for duty benefits

similar to any other activity in the SEZ. This amendment is likely to provide relief to those developers, who had pre-existing structure (for commercial use) on the proposed SEZ land and they were in a dilemma whether to demolish such structures for the purpose of fulfilling 'vacant land' and notification of the SEZ. |

| Exit route | Under

the SEZ framework, Rule 74 of the SEZ Rules 2006 provided for exit

of unit, subject to payment of applicable duties on the imported or

indigenous capital goods, raw materials, components, consumables,

spares and finished goods in stock. Further, if the SEZ unit didn't achieve positive net foreign exchange, the exit shall be subject to penalty that may be imposed under the Foreign Trade (Development and Regulation) Act, 1992. |

Transfer of ownership of SEZ units, (including sale) permitted

subject to fulfilment of prescribed conditions. New Rule 74A has been inserted to the SEZ Rules, 2006. |

This amendment seeks to facilitate easier exit by a SEZ unit, by way of the transfer of ownership/ sale subject to fulfilment of prescribed conditions |

FREQUENTLY ASKED QUESTIONS ON SEZs

Part-I : Preliminary

Q. What is a Special Economic Zone?

A. Special Economic Zone (SEZ) is a specifically delineated duty free enclave considered to be a deemed foreign territory [within India] for the purposes of trade operations, duties and tariffs. SEZ, thus, is a geographical region where the fiscal and economic laws are more liberal as compared to the business undertakings in the Domestic Tariff Area (DTA).

The entire SEZ area is divided into Processing and Non-processing area.

- Processing Area –in which the core business activities of the SEZ is undertaken by the approved units. Atleast 50% of the SEZ area has to be processing area.

- Non-processing Area –in which the support infrastructure is created, primarily to cater to the needs of the employees working in the SEZ.

- SEZ scheme has following two important constituents:

- Developer/ Co-developer –who establishes the entire SEZ. There can be more than one Co-developer(s). Usually, the infrastructure in the non-processing area is developed by the Co-developer(s).

- Entrepreneur –who sets-up unit in the SEZ.

Q. Who can set up SEZ?

A. SEZ may be set-up either by the Central Government, State Government, or any person or combination thereof.

Q. For what purpose, a SEZ may be setup? What are the various formats of SEZs?

A. SEZ can be established for manufacture of goods or rendering services or for both or as a Free Trade and Warehousing Zone.

The following formats of SEZs are envisaged under the SEZ Act, 2005:

- Sector Specific SEZs (single product or single

service3, viz., Engineering, Gems and Jewellery, IT/

ITES, Biotechnology, etc.)

Various categories comprising their respective products or services, similar or compatible with each other, including related ancillary services and R&D services of the sector and additional combination of products and services of a similar or compatible nature as approved by the board of approval shall constitute a single sector - Multi-product SEZs (combination of two or more products or services)

- Free Trade and Warehousing Zones.

Q. Can a foreign company or a non-resident set up SEZ in India?

A. Yes, a foreign company or a non-resident can set up SEZ in India.

Q. How can foreign companies set up branch offices/ units in SEZ?

A. The Reserve Bank of India has granted general permission to foreign companies to establish branch offices/ units in SEZs to undertake manufacturing and service activities. Foreign companies can establish branch offices/ units in SEZs provided 100 per cent FDI is permitted in the relevant sectors. The said branch offices/ units should function on a stand-alone basis.

Part-II: Setting up of SEZ

Q. How can one apply for setting up of SEZs?

A. Application to be made to the concerned State Government or to the Board of Approval (the 'Board' or the 'BoA') in Form–A prescribed under the SEZ Rules, 2006 indicating therein name and address of the applicant, status of the promoter along with the project report covering the following particulars:

- Location of the proposed SEZ with details of infrastructure facilities that are proposed to be created;

- Area of SEZ, distance from the nearest sea port / airport / rail/ road etc.

- Financial details, including investment proposed, modes of financing and viability of the project;

- Details of foreign equity (if any) and projected repatriation of dividend;

- Types of SEZ –whether the SEZ will allow only certain specific industries/ service providers or will be a multi-products/ multi-services SEZ;

- Declaration and Affidavit [as provided in Form-A].

Further, a duly filled and signed Checklist (in prescribed format) is required to be submitted along with the Application Form.

For indicative procedure of setting up of SEZ, please refer flow chart on page 4.

Q. What are the obligations of the State Government on receipt of proposals for setting up of SEZ?

A. The State Government shall forward proposals received, along with its comments on the following to the BoA to the effect that –

- the area incorporated in the proposed SEZ is free from environmental restrictions;

- water, electricity and other services would be provided as required;

- the units would be given exemption from electricity duty or tax on sale of electricity for self generated and purchased power;

- the generation, transmission and distribution of power within SEZ will be allowed;

- the State Government shall endeavour to provide exemption from State sales tax/ Value Added Tax (VAT), octroi, mandi tax, turnover tax and any other duty/ cess or levies on the supply of goods from DTA to SEZ Units;

- for units inside the SEZ, the powers under the Industrial Disputes Act and other related labour Acts would be delegated to the Development Commissioner and that the Units will be declared as a Public Utility Service under Industrial Disputes Act;

- the State Government shall announce its Policy on SEZ supported by requisite notifications before recommending any proposal for setting up SEZ in the State

- single point clearance system and minimum inspections requirement under State Laws/ Rules would be provided.

Note: It is however advisable to check before hand, availability of single window mechanism in the State in question.

Q. What are the stages involved in the approval process?

A. The proposal incorporating the commitments of the State Government will be considered by the BoA. Thereupon, the approval is granted to the Developer.

There are three stages of approval mechanism, namely –

- In-Principal Approval –

BoA grants in-principal approval (in Form B-1) in cases where the Developer is not having the land in its legal possession (whether by way of ownership or lease). - Formal Approval –

Once the Developer has the legal possession of the land (whether by way of ownership or lease) and submits the requisite details in support thereof to the BoA, formal approval is granted by the BoA (in Form B). - Notification of SEZ –

After formal approval by the BoA, the following information is to be submitted to the Department of Commerce, Ministry of Commerce and Industry, Government of India:

- Details of the land along with survey numbers and location map and certificate from the concerned State Government or its authorized Agency stating that the Developer has legal possession and irrevocable rights to develop the said area as SEZ and that the said area is free from all encumbrances.

- Inspection report of the jurisdictional Development Commissioner of the SEZ.

Upon receipt of the above information, the Government shall notify the SEZ by way of issue of a Notification to that effect.

Part-III: Setting up of unit in a SEZ

Q. How to set-up a Unit in a SEZ?

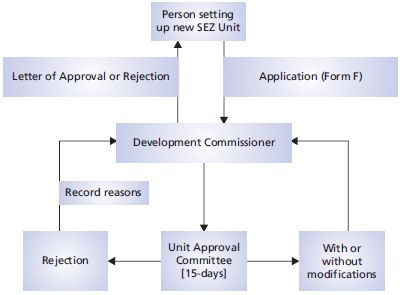

A. Any person, who intends to set-up a Unit in a Special Economic Zone, may submit a proposal to the jurisdictional Development Commissioner in Form 'F' as provided under the SEZ Rules.

For indicative procedure of setting up of SEZ unit, please refer flow chart on page 4.

Q. What is the approval mechanism for the units?

A. All approvals to be given by the Unit Approval Committee headed by the Development Commissioner.

Q. What are the obligations of the unit under the Scheme?

A. SEZ units have to achieve positive net foreign exchange earning as per the formula given in rule 53 of SEZ Rules, 2006. Broadly, the F.O.B. value of exports has to be more than the C.I.F. value of imports over the period of 5- years.

Q. Is inter-unit sale permitted?

A. Yes, inter-unit sale is permitted under the SEZ Act.

Part-IV: Incentives and benefits available to SEZ Developers and Units

Q. What are the incentives/ benefits available to SEZ Developer/ Co- Developer?

A. The major incentives and benefits available to SEZ Developer/ Co- Developer include:

Direct taxes

- 100% income-tax deduction allowed to the Developer under section 80-IAB of the Income-tax Act, 1961 for any consecutive 10 years out of the first 15 years from the date of notification of the SEZ.

Indirect taxes

- Duty free import/ domestic procurement of goods for development, operation and maintenance of SEZ.

- Exemption from/ refund of Service Tax

- Exemption from Central Sales Tax. FEMA/ FDI

- 100% FDI permitted for setting up of SEZ with approval of BoA.

Miscellaneous

- Generation, Transmission and Distribution of power in SEZ allowed.

- Full freedom in allocation of space and built-up area to approved SEZ units on commercial basis.

- Authorized to provide and maintain services, viz, water, electricity, security, restaurants and recreation centers on commercial basis.

Q. What are the incentives/ benefits available to SEZ Units?

A. The major incentives and benefits available to SEZ Units include:

Direct taxes

- 15-years tax holiday in a phased manner subject to certain conditions. 100% income tax exemption under section 10AA of the Income-tax Act, 1961 for the first 5-years, 50% for the next 5-years and thereafter 50% of the ploughed back export profits for next 5-years.

Indirect taxes

- Duty free import/ procurement from domestic sources of all the requirement of capital goods, raw materials, office equipment, etc. for implementation of the project in the SEZ without any licence.

- Exemption from/ refund of Service Tax

- Exemption from Central Sales Tax

FEMA/ FDI

- 100% FDI allowed under automatic route for all manufacturing

activities in the SEZ, except for the following activities.

- Arms and ammunition, explosive and allied items of defence equipment, defence aircraft and warship;

- Automatic substances;

- Narcotics and psychotropic substances and hazardous chemicals;

- Distillation and brewing of alcoholic drinks; and

- Cigarettes/cigars and manufactured tobacco substitutes.

- Sectoral norms as notified by the Government shall apply to the foreign investment in services. The cases not covered by automatic route shall be considered and approved by the BoA. For policy on FDI caps and routes (Government/ automatic) in various sectors, please refer Press Note no. 6 (2013 Series) dated August 22, 2013.

- External Commercial Borrowing (ECB) by SEZ units upto US $ 500 million allowed in a year under Automatic Route without any maturity restriction through recognized banking channels. Export proceeds to be realised and repatriated to India within a period of 12 months from the date of export. Any extension of time beyond the period of 12 months to be granted by RBI on case to case basis4.

- Flexibility to keep 100% of export proceeds in foreign currency account. Freedom to make overseas investment from such foreign currency account.

- Writing-off unrealized export bills allowed.

[Indian] Companies Act, 1956

- Enhanced limit of INR 24,000,000 (Indian Rupees Twenty Four million) per annum allowed for managerial remuneration.

- Exemption from the requirement of being resident in India for a period of 12-months prior to appointment as Managing Director, Whole-time Director or Manager (as defined under the Indian Companies Act, 1956).

Environment related

- SEZs permitted to have non-polluting industries in information technology (IT) and re-creational facilities like golf courses, desalination plants, hotels and non-polluting service industries in the Coastal Regulation Zone Area.

Sub-contracting/ Contract farming

- Units may sub-contract part of production or production process through Units in DTA or through other EOUs/SEZ units.

- Units may also sub-contract part of their production process abroad.

- Agriculture/ Horticulture processing SEZ Units allowed to provide inputs and equipment to contract farmers in DTA to promote production of goods as per the requirement of importing countries.

Q. What are the facilities for Domestic suppliers to SEZ?

A. Supplies from DTA to SEZ to be treated as physical export and the DTA supplier would be entitled to:

- Duty Drawback / DEPB.

- Discharge of export obligation, if any, of the suppliers.

Footnotes

1. Many State Governments have extended exemption from Value Added Tax (VAT). However, for the exact position with reference to any specific State, please refer corresponding exemption notification under respective State VAT Act.

2. Many State Governments have extended exemption from stamp duty. However, for the exact position with reference to any specific State, please refer respective State Stamp Act.

3. SEZ (Amendment) Rules. 2013 notified on August 12, 2013

4. RBI A.P.(DIR Series) Circular no. 108 dated June 11, 2013

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

© 2013, Vaish Associates, Advocates,

All rights reserved with Vaish Associates, Advocates, 10, Hailey

Road, Flat No. 5-7, New Delhi-110001, India.