- within Wealth Management topic(s)

Quick Read

The Stock Exchange of Hong Kong Limited (SEHK) published its "Consultation Conclusions on Environmental, Social and Governance Reporting Guide" (Consultation Conclusions) on 31 August 2012 in response to its corresponding consultation paper published on 9 December 2011. For details of the consultation paper, please refer to our previous Legal Update "Consultation on Environmental, Social and Governance Reporting Guide".

SEHK decided to implement the Environmental, Social and Governance (ESG) Reporting Guide (Guide) which will be appended to the Rules Governing the Listing on The Stock Exchange of Hong Kong Limited (Listing Rules) as a recommended practice.

The Guide will apply to issuers with financial years ending after 31 December 2012. Subject to further consultation, SEHK intends to escalate the obligation level of some recommended disclosures in the Guide to "comply or explain" by 2015.

The Guide

WHERE SHOULD ESG DISCLOSURE BE MADE?

An issuer can choose to make ESG disclosure in its annual report (which must be of the same period covered in the annual report) or in a separate report (free to report on any period although reporting on the same period in the annual report is encouraged). It can do so in print or on its website.

WHO SHOULD BE INVOLVED IN THE ESG DISCLOSURE?

The board of directors is primarily responsible for the ESG reporting although it may delegate the task of compiling the ESG report to its employees or a committee that reports to the board.

In addition, an issuer should engage stakeholders periodically to identify material aspects and key performance indicators (KPIs) (please see below for explanation) and understand their views. Stakeholders include parties such as shareholders, business partners, employees, suppliers, subcontractors, consumers, regulators and the public that have interests in or are affected by the decisions and activities of the issuer.

WHAT ESG DISCLOSURE CAN BE MADE?

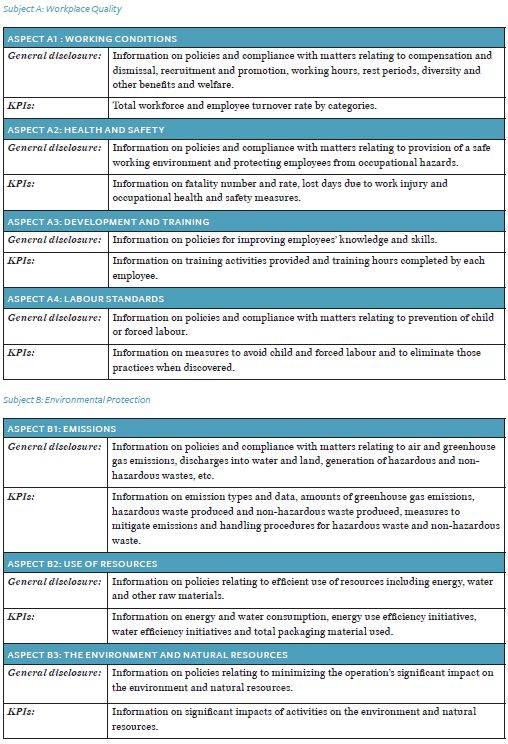

The Guide sets out subject areas, aspects, general disclosure and KPIs on a level-by-level basis which an issuer can report on. There are four ESG subject areas: Workplace Quality, Environmental Protection, Operating Practices and Community Involvement. Under each subject area, there are various aspects. For each relevant aspect, there are requirements on general disclosure and KPIs.

The Guide is not comprehensive and is designed for issuers with limited knowledge on ESG matters as a starting point for ESG reporting. Issuers are encouraged to adopt international guidelines instead if they are capable of doing so.

The subject areas, aspects, general disclosure and KPIs specified in the Guide are summarised below:

No definition is provided for KPIs. An issuer is encouraged to explain how the KPIs are calculated and include information that is necessary for interpreting the KPIs.

WHAT IS THE SCOPE OF DISCLOSURE?

An issuer is not required to report on all subject areas, aspects and KPIs and is encouraged to identify and report on relevant ESG subject areas, aspects and KPIs which are material to it. It is also encouraged to prioritise ESG subject areas, aspects and KPIs and emphasize material areas in the ESG report.

Also, an issuer is not expected to make ESG disclosure on all of its operations/subsidiaries from the start and can commence reporting on its major operations/subsidiaries only. It is encouraged to explain the scope and identify which entities in the group and/or which operations have been included in the ESG report. If there is any change in the scope, the issuer is encouraged to provide explanation and reason for such change.

WHAT IS THE PATTERN OF DISCLOSURE?

An issuer is encouraged to report on a regular basis once it has started its reporting. The aspects and KPIs reported may be consistent for each period with explanation provided for any changes. An issuer may also explain why some aspects and KPIs are not reported.

You may download copies of the Consultation Conclusions via the link below:

http://www.hkex.com.hk/eng/newsconsul/mktconsul/Documents/cp201208cc.pdf

Originally published 17 September 2012

Keywords: SEHK, listing rules, Environmental Social and Governance Reporting Guide, ESG disclosure,

Learn more about our Hong Kong office and Corporate & Securities practice.

Visit us at www.mayerbrown.com

Mayer Brown is a global legal services organization comprising legal practices that are separate entities (the Mayer Brown Practices). The Mayer Brown Practices are: Mayer Brown LLP, a limited liability partnership established in the United States; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales; Mayer Brown JSM, a Hong Kong partnership, and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2012. The Mayer Brown Practices. All rights reserved.

This article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein. Please also read the JSM legal publications Disclaimer.