With many firms and companies targeting wealthy families and individuals in the wave of the considerable increase in philanthropy, as part of a continuing series on the uses of Trusts, this article, which will be presented in two parts, will consider what constitutes a charitable trust and their uses allowable under Common Law.

To put this subject into context, it is estimated that in the next fifty years the transfer of wealth between the generations of families is to be between $60-170 trillion dollars. Various forecasts for global philanthropic giving range into the billions of US dollars by the end of the decade and between $12 and $15 trillion over the next 20 years.1 With all this money being given to worthy causes, many have contemplated establishing a Trust to hold the assets and to manage the ultimate grants or gifts that are to be made. Surprisingly, it may seem that there are considerable restrictions on what is considered as a "Charitable Trust" under the Common Law and those jurisdictions that follow the Anglo-Saxon legal system.

In an earlier article for the "Profiler"2 I explained that for a trust to exist there has to be certainty of object, in other words, it must be possible to identify the beneficiaries of a trust for that trust to exist. This clearly causes difficulty when we consider that many charitable intentions do not identify an individual or even necessarily a group of people, but some purpose, then under this strict interpretation the Trust could not be established. As trusts are a creation of the English Law of Equity which was based upon doctrines of fairness, this would seem harsh.

If we look historically at this position, it is clear that in medieval times, symbolized by pious and charitable acts, the ecclesiastical courts at that time sought, wherever possible, to uphold these charitable gifts. Of course, at this time, most of these gifts, commonly tracts of land, went to the religious orders that dominated the lives of individuals and it may be such that an element of self-interest existed. However under the rules of mortmain 3 and in an attempt to limit the power of the religious orders whilst preserving the taxes and dues that arose to the King and to his Lords on such land, the legislature had a policy to restrict such gifts.

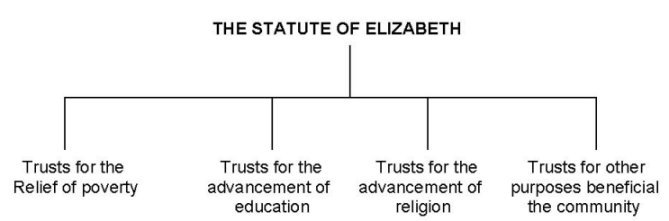

Following the reformation of Henry VIII, the religious orders had been banished or destroyed and their lands seized, this stopped a channel for such pious acts and charitable gifts. The Crown, in realizing the potential damage this could cause, passed legislation to promote such gifts 4 . This important piece of law, commonly referred to as "The Statute of Elizabeth" had a preamble that set out what were considered to be the most important causes that would be accepted as charitable.

Whilst the Statute of Elizabeth has been repealed 5 and is thus no longer law, the preamble was preserved for a considerable time until repealed in 1960 6 but the intentions and sentiment that it expressed remain principally through case law 7 which over time has modified the original sentiment to reflect more accurately the intentions and attitudes of proceeding generations.

Whilst the preamble to the Statute of Elizabeth is full of Elizabethan prose, it is possible to summarise what are held to be the four charitable causes:

For a charitable trust to exist, the trust must firstly be of a charitable nature in the spirit and intendment of the Statute of Elizabeth, it must promote a public benefit and it must be wholly and exclusively charitable. It will no doubt come as no surprise that there has been much debate as to what these four headings actually mean, and their interpretation may be best explored by example where the cause has been held charitable, and where it has not.

For a trust to be accepted under the relief of poverty, it must be intended for persons who are actually poor. Thus in the case Re Sanders’ Will Trust 8 a gift to provide for the "working classes" was held not to be charitable as the expression "working classes" did not indicate poor persons. It has become an established principle of law that where the gift is of a size that the benefit derived from it is such that only a poor person will receive genuine benefit from the gift, this is an acceptable guide. Thus in the case Re Niyazi’s Will Trusts 9 the gift of £15,000 to build a working men’s hostel in Famagusta in Cyprus was held to be charitable as the term "working men’s hostel" connoted poverty as the sum available would only fund a very modest hostel and would only provide the basic facilities and amenities, thus only the relatively poor would occupy it. This was again the position held in Re Lucas 10 where a gift of 5/- (five shillings) per week was to be given to the "oldest respectable inhabitants of Gunville".

Importantly, in the preamble to the Statute of Elizabeth it refers to the "Relief of aged, impotent and poor People" but it has been established that these expressions should be read disjunctively in that aged and impotent people qualify as objects of charitable cause and need not be poor. But, for these areas to be considered charitable, there has to be some means of qualifying under these headings. If it were not so, it would be quite possible for abuses of the various laws governing charities to occur.

All of these points have been considered through the courts and it is held that when dealing with impotence, there must some form of relief of that impotence 11 . In these cases, impotence is held to be some form of infirmity or ailment, such as paralysis, blindness or mental disorders. The courts are prepared to give a very wide interpretation to such causes, to include, for example, charities established to provide relief to families of individuals affected by such conditions 12 . In turn, the question must be asked what is aged? It has been established, that for the interpretation of this point, aged is to mean someone in there sixties or older, although no precise age has been identified.

The second category established under the preamble is education. Again turning to the wording contained in the Statute of Elizabeth, these purposes are to include "Maintenance of… Schools of Learning, Free Schools and Scholars in Universities…". In an important case in this area, Incorporated Council of Law Reporting for England and Wales v Attorney-Genera 13 l it was held that the term implied to the improvement of education and its dissemination.

In looking at examples where the courts have had to decide on the validity of charities intended to benefit and promote education, an interesting case was that of a trust established by the Irish author George Bernard Shaw in which a research programme was to be funded to determine whether there was benefit in adding further letters to the established English alphabet and to report on such findings.14 The court rejected this as a genuine charitable cause as it did nothing to increase education but merely to increase knowledge. Interestingly, in an earlier decision, a trust established by the Author’s widow had been held as charitable where its objects were for:

"the making of grants, contributions and payments to any foundation…having as its objectives the bringing of masterpieces of fine art within the reach of the people of Ireland of all classes in their own country…. The teaching promotion and encouragement in Ireland of self control, elocution, oratory, deportment, and the arts of personal contact, of social intercourse and the other arts of public, private, professional and business life."

The precise definition of education has been challenged on a number of occasions. It is now well established that it does not simply mean the provision of schools, teaching and instruction. It includes the improvement of a useful branch of human knowledge and its public dissemination 15 and subject to certain provisions, it can include research 16 , but see above with reference to George Bernard Shaw’s case. There have been interesting interpretations of these conditions and it has been held that a search for missing manuscripts to identify whether Sir Francis Bacon or William Shakespeare wrote the plays and sonnets attributed to the latter was held to be charitable 17 as was the maintaining and support of a choir 18 .

One area that has vexed the courts is whether sport is to be regarded as a charitable purpose. It has been held that if the sporting event or tuition is conducted by a school or university it will be a valid trust under this head 19 . The promotion of sport purely for sport’s sake is in general not charitable and these cases must be distinguished from the above position as in IRC v McCullen. This position is now somewhat assisted by the Recreational Charities Act 1958.

It is thus essential in all of these cases to determine whether a trust is for the advancement of education. This, as can be seen above, can lead to considerable difficulties and it is very important when considering creating a charitable trust under common law that very specific advice is sought.

In the next part if this article, we will seek to explore the remaining two areas to be covered under the Statute of Elizabeth and will consider what is the public benefit, something that has to exist for a charitable trust to be accepted by the courts.

"Charity suffereth long, and is kind; charity envieth not;

charity vaunteth not itself, is not puffed up……

Beareth all things, believeth all things,

Hopeth all things, endureth all things.

Charity never faileth"

I Corinthians ch. 13, v. 4

1 Source: The Philanthropic Initiatives, Inc. Spring 2001

2 "The Three Certainties or: when is a trust not a trust" December 2001

3 Mortmain – "dead hand", where the assets are no longer owned by an individual and thus beyond the reach of

any taxation and feudal dues.

4 The Statute of Charitable Uses 1601 (43 Eliz 1 c4)All ER 101 19 IRC v McMullen [1981] AC1

5 Mortmain and Charitable Uses Act 1888

6 s 38(4) Charities Act 1960 as amended by the Charities Act 1993

7 See McGovern v Attorney-General [1982] Ch 231 and the discussion by Lord Reid of its effect in Scottish

Burial Reform and Cremation Society v Glasgow Corporation [1968] AC 138

8 [1954] Ch 265

9 [1978] 1 WLR 910

10 [1922] 2 Ch 52

11 IRC v Baddeley [1955] AC 573

12 see Re Dean’s Will Trusts [1950] 1 All ER 882

13 [1972] Ch 73

14 [1957] 1 WLR 729

15 Incorporated Council for Law Reporting for England and Wales v Attorney-General [1972] Ch 321

16 McGovern v Attorney-General [1982] CH 321

17 Re Hopkins Will Trust [1965] Ch 669

18 Royal Choral Society v IRC [1943] 2 All ER 101

19.IRC v McMullen [1981] AC1

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.