There has been greater interest in recent years for the use of trusts to hold artwork, particularly as an investment class in its own regard, or a "diversifier" asset class which is less correlated with world stock markets.

Sales of fine art have grown significantly in the last 5 years. Since the market crisis in 2008/9, there has been an increase of nearly two-thirds in the global art market, according to the latest figures from the European Fine Art Foundation (TEFAF). These suggest a figure of $46.1bn in 2011, represented by public auctions and estimates of private sales.

In 2012, $12.3bn was generated at fine art auctions alone, the two main multinational players being Christies and Sotheby, with a combined annual turnover of $5.2bn. A large percentage of their auction revenues are represented by a small number of sales, being only 0.23% of total transactions - where fine art is sold for prices over $1m

INVESTMENT MATTERS

In terms of the performance of art as an investment, the Mei Moses World All Art Index (tracking prices across various genres of art) almost matched returns from the S&P 500 index over 50 years, and actually outperformed the S&P 500 over the last 10 years.

Recent research from JP Morgan has also shown that the volatility of art prices was lower than US and international equities as well as commodities over the last 25 years.

A TURBOCHARGED CHINESE DRAGON...

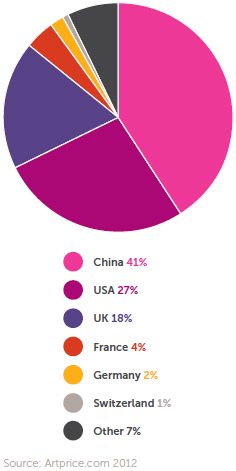

Interest in fine art continues to grow amongst private clients and trustees. There is now significant interest from China, accounting for 41% of all fine art auction turnover, as shown by the following schematic:

2012 FINE ART AUCTION TURNOVER - BY COUNTRY

However, caution has been urged with regard to the increasing number of art-investment products offered by Chinese investment trusts and art exchanges, which have "turbocharged" the Chinese market in recent years. These products include the ability for shares in individual pieces of artwork to be bought and sold.

Commentators have expressed concern regarding loose regulatory oversight of these products, the lack of legal framework and concern that many managers do not have experience of falling art markets. Many funds operate with short maturities up to 2 - 3 years, which could trigger 'sell' pressures into poor markets, should the Chinese economy slow significantly. Last year, the World Bank forecast the weakest Chinese growth in 12 years.

The Chinese government has started to act to prevent overheating of the market, and closed down many art exchanges following very rapid growth in the last 5 years, amidst some reports of excessive price speculation.

Whilst not all people are seeking to buy art purely for speculation, what should settlors and trustees consider when looking to hold artwork in trust structures?

There are a number of key considerations which include:

RATIONALE FOR USE OF A TRUST STRUCTURE

It is important to establish the long-term rationale for holding artwork in trust - some of the benefits may include:

- building an art collection in a trust, as an single investment class - to benefit future generations of beneficiaries

- a diversifier asset class for a trust which holds other conventional investments

- succession planning to ensure a family art collection remains intact after the settlor's death

FORM OF TRUST STRUCTURE

If the structure will be used solely to hold works of art, then a discretionary trust is unlikely to be the most suitable form of trust, given the asset concentration risk for the trustee. A purpose trust, reserved powers trust or foundation may be better suited in this scenario.

TRANSFERRING WORKS OF ART INTO TRUST

There will be a number of matters to consider, including:

- Are there any legal or taxation considerations for the person who will be transferring works of art into the trust - such as gift taxes?

- Provenance and valuation of paintings - confirming identity of the artist, originality of the painting and that there are no issues with previous ownership. It may be necessary to engage art specialists to assist with the relevant enquiries. Defective title insurance can be taken out; this will often be subject to full enquiries being made in advance.

- Changing the ownership of the artwork - legal agreement / gift documentation between donor and trustee

- The trustee will need to arrange suitable insurance; a specialist insurer may be required

- Ensuring careful shipment by fine art shippers and storage of artwork, as necessary

- Ensure a detailed inventory of the artwork is drawn up and kept up-to-date

ONGOING ADMINISTRATION

- Where will the artwork be kept? At the beneficiary's residence, in storage, or loaned to galleries, museums or others - possibly for a fee?

- Ensure whoever holds the art (if not the trustee) fully understands that the trust is the legal owner - prepare agreements as necessary

- If the beneficiary will enjoy the artwork at their residence, will this give rise to any taxable benefit on them?

- Ensure adequate security and insurance for paintings

- Arrange periodic valuations of artwork - usually every 3 years

- Arrange periodic inspections, particularly if older works of art - which may require restoration from time-to-time

- What are the donor's / trustee's views as to the possible sale of the artwork in the future - are there any "trigger events" or price targets? Or will the artwork simply be held for future family enjoyment?

- Liquidity - will there be sufficient cash in the trust structure to meet ongoing costs relating to the artwork, as well as professional fees? Or will pieces need to be sold at some stage?

COLLAS CRILL TRUST

Collas Crill Trust acts as trustee to a number of structures holding works of art. We also work with art advisory firms who can assist in a number of areas, including provenance, valuation, and identifying the most favourable cities and auctioneers for the sale of specific works of art.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.