关联方及关联交易的认定及披露一直是证监会、交易所、证监局等监管部门关注的重点,根据去年11月份的证监会发行部发行审核业务的培训要求以及今年3月份的《首发业务若干问题解答》,不难看出审核实务中,监管部门一方面是原则上尊重企业合法合理、正常公允且确实有必要的经营行为,但另一方面需要发行人及中介机构准确认定关联方以及充分完整地披露关联交易,并对关联交易的必要性、公允性、合法性、合理性以及程序性进行核查并发表意见。尽管对关联方的认定有诸多规定,但实务中对关联方的认定及披露尺度还是存在一定的差异,尤其是对参股公司作为关联方的认定及披露的标准不一。因此,本文仅就参股公司作为关联方的认定及披露问题进行阐述,供抛砖引玉。

一、"关联方"的法律定义及核查思路

在IPO当中,关于参股公司是否作为关联方来认定及披露问题,笔者认为首先需要确定"关联方"的法律定义,然而我国却没有对"关联方"有一个明确的法律概念,而是通过列举式或概括式的立法[1]模式来认定"关联方",具体的规定详见本文的附件。《公司法》第二百一十六条只是明确了"关联关系",通常来说,若与发行人存在这种关联关系的,我们会将其作为关联方来披露,但是该定义一方面将主体限制的过窄,另一方面又显得过于模糊,实务中不好把握。《企业会计准则第36号--关联方披露》(以下简称《会计准则》)以列举式的方式来认定,其中包括了母子企业、合营企业、联营企业等,当然《会计准则》对于关联方认定的标准核心还是在于是否有"施加重大影响""实施共同控制"等情形。证监会及交易所则通过列举式+概括式的立法模式确定关联方,这种立法模式在很大程度上解决了关联方的认定以及核查问题,正因如此,实务中券商、律师中介机构往往是根据证监会及交易所的规定来认定关联方及关联交易,会计师更多是参照《会计准则》来披露关联方,而且往往披露有交易的关联方。

然而,在实务反馈意见中,证监会要求发行人及券商、律师根据《公司法》《会计准则》以及证监会的规定来认定并披露关联方,正如前文所述,《会计准则》关于关联方的认定与证监会及交易所有不同,例如关于子(孙)公司是否作为关联方来披露,实务中操作不一,笔者也检索了相关案例的《招股说明书》《律师工作报告》,大部分是将子(孙)公司作为关联方来披露的,但是因合并报表,合并范围的交易未作为关联交易来披露。

就参股公司而言,实务中就参股公司披露的标准问题一直是存在差异的,而之所以将参股公司作为关联方来披露是参照《会计准则》第四条的规定,即联营企业构成企业的关联方。根据《民法通则》的规定,联营有三种模式,分别是公司型联营、合伙型联营、契约型联营。《企业会计准则第2号--长期股权投资》也规定了投资方能够对被投资单位施加重大影响的,被投资单位为其联营企业。重大影响,是指投资方对被投资单位的财务和经营政策有参与决策的权力,但并不能够控制或者与其他方一起共同控制这些政策的制定。在实务当中,"重大影响"有至少有以下几个重要的体现:一是发行人委派代表参与对参股公司的实际经营,比如股东会或董事会,通过在参股公司的实际经营决策实施重大影响;二是若发行人直接或间接持有参股公司20%-50%的股权,一般认为对参股公司具有重大影响,除非有明确的证据表明该种情况下不能参与参股公司的生产经营决策,不形成重大影响;三是发行人与参股公司之间签署能够实施重大影响的协议或存在其他类似安排,比如托管协议。

需要注意的是,若发行人与参股公司的其他大股东签署的协议约定一起对参股公司实施共同控制的,则根据《企业会计准则第40号--合营安排》[2]的规定,该"参股公司"应当根据实质重于形式的原则认定为合营企业而非联营企业,当然不管是联营企业还是合营企业,根据《会计准则》都应认定为关联方。

因此,判断参股公司是否是上市公司的关联方,除了根据证监会、交易所规定关于认定关联方的基本情形之外,还需要从会计角度判断的"重大影响""共同控制"以及"利益倾斜"等情形来综合判断。而这些判断的基础需要中介机构本着勤勉尽责、谨慎核查、实质重于形式的原则,充分收集参股公司的工商资料、出资凭证以及结合外部网络核查,对参股公司的股东、董监高以及财务人员与发行人及其股东、董监高之间是否存在股权代持、近亲属等关联关系或其他利益输送等方面进行访谈确认,若参股公司与发行人在报告期内每年都大量的购销交易,则中介机构更需要格外注意其是否属于潜在的关联方或者关联交易非关联化。

二、案 例

(一)间接持股未超过20%不认定为关联方——青岛蔚蓝生物股份有限公司

根据蔚蓝生物首次公开发行股票招股说明书,蔚蓝生物通过子公司、孙公司间接参股三家公司,如通过子公司青岛蔚蓝生物集团有限公司持有青岛易家禽农牧发展有限公司19.50的股权,但都没有被认定为关联方。但是,根据谨慎性原则,发行人将发行人子公司的销售人员设立的公司视同为关联方并将双方交易按照关联交易披露。

沈阳凯奥生物科技有限公司(以下简称"沈阳凯奥")成立于2016年1月25日,系发行人子公司原销售人员盛柱及董兴刚出资设立的生物制品销售公司,该公司在沈阳地区掌握了一定的销售渠道,发行人为了开拓该地区的业务,与其建立合作关系。2016年、2017年和2018年上半年,发行人分别向沈阳凯奥销售生物制品141.81万元、341.42万元和55.33万元,占营业收入的比例为0.18%、0.43%和0.14%,销售价格与无关联第三方总体无重大差异,交易价格公允。

(二)委派人员为联营公司的董事认定为关联方——深圳市赢时胜信息技术股份有限公司

根据该公司2016年11月18日披露的《关于公司对外投资暨关联交易的补充公告》,该公司认为公司派驻中层人员任联营公司董事后,根据实质重于形式原则,将参股联营的公司算作公司关联方。

具体披露情况:"公司于2016年7月28日召开的第三届董事会第六次会议及2016年8月12日召开的2016年第三次临时股东大会审议通过了《关于参股公司东吴在线(苏州)金融科技服务有限公司增资扩股的议案》同意公司使用自有资金出资人民币40,000万元,参与东吴在线的融资,认购东吴在线增加的注册资本,投资完成后公司占东吴在线28%股权,属于联营企业,在公司对东吴在线进行增资后公司委派公司中层管理人员担任东吴在线的董事一职。根据实质重于形式原则、根据《深圳证券交易所创业板股票上市规则》、《企业会计准则-关联方关系及其交易的披露》的规定,为了更好的保护投资者的利益,公司认定东吴在线属于公司的关联方,故本次共同投资构成关联交易。"

(三)持股比例超过20%认定为关联方——陕西省天然气股份有限公司

根据该公司2017年5月5日披露的《关于预计2017年度日常关联交易的补充公告》,陕天然气对咸阳市科技产业投资有限公司持股35%,陕西然气根据实质重于形式、可能造成公司对其利益倾斜的原则,并依据《深圳证券交易所股票上市规则》:"(五)中国证监会、本所或者上市公司根据实质重于形式的原则认定的其他与上市公司有特殊关系,可能或者已经造成上市公司对其利益倾斜的法人或者其他组织。"的规定将参股的公司算作公司关联方。

(四)持股比例低于20%,但是派驻董事,因此认定为关联方——漱玉平民大药房连锁股份有限公司

根据公司2018年12月14日披露的《漱玉平民大药房连锁股份有限公司首次公开发行股票招股说明书(申报稿2018年12月11日报送)》,发行人将发行人对有重要影响的三家直接或间接参股公司认定为关联方。所谓"有重要影响"的认定标准:虽然直接或间接持股比例低于20%,但是发行人实际控制人在参股公司任职董事、高管或发行人派驻董事。因此,将参股公司作为关联方来披露。

三、总 结

根据上述规定和案例,笔者认为,判断参股公司是否是关联方需要本着实质重于形式的核查原则,以重大影响、共同控制、利益倾斜为方向,以公司股权表决权、经营权、人事任免权为基础的核查思路来综合判断:

(一)如果发行人只是单纯地参股投资一家公司,且持股低于20%,不涉及对所参股公司的财务、经营决策进行干预以及其他特别协议安排或人员派驻情况,那么可以不认定为关联方,但是有其他证据表明发行人对参股公司实施重大影响、利益倾斜的,则也需要认定为关联方。

(二)尽管发行人对参股公司持股比例低于20%,但是发行人对参股公司有人事任免权,则视为对参股公司有重要影响,那么基于实质重于形式的原则,应将参股公司认定为关联方。

(三)若发行人对于参股公司持股高于20%,则同样视为对于参股公司有重要影响,应作为关联方披露。

(四)根据证监会及交易所关于关联方认定的其他情形,比如发行人实际控制人的近亲属在参股公司任职。

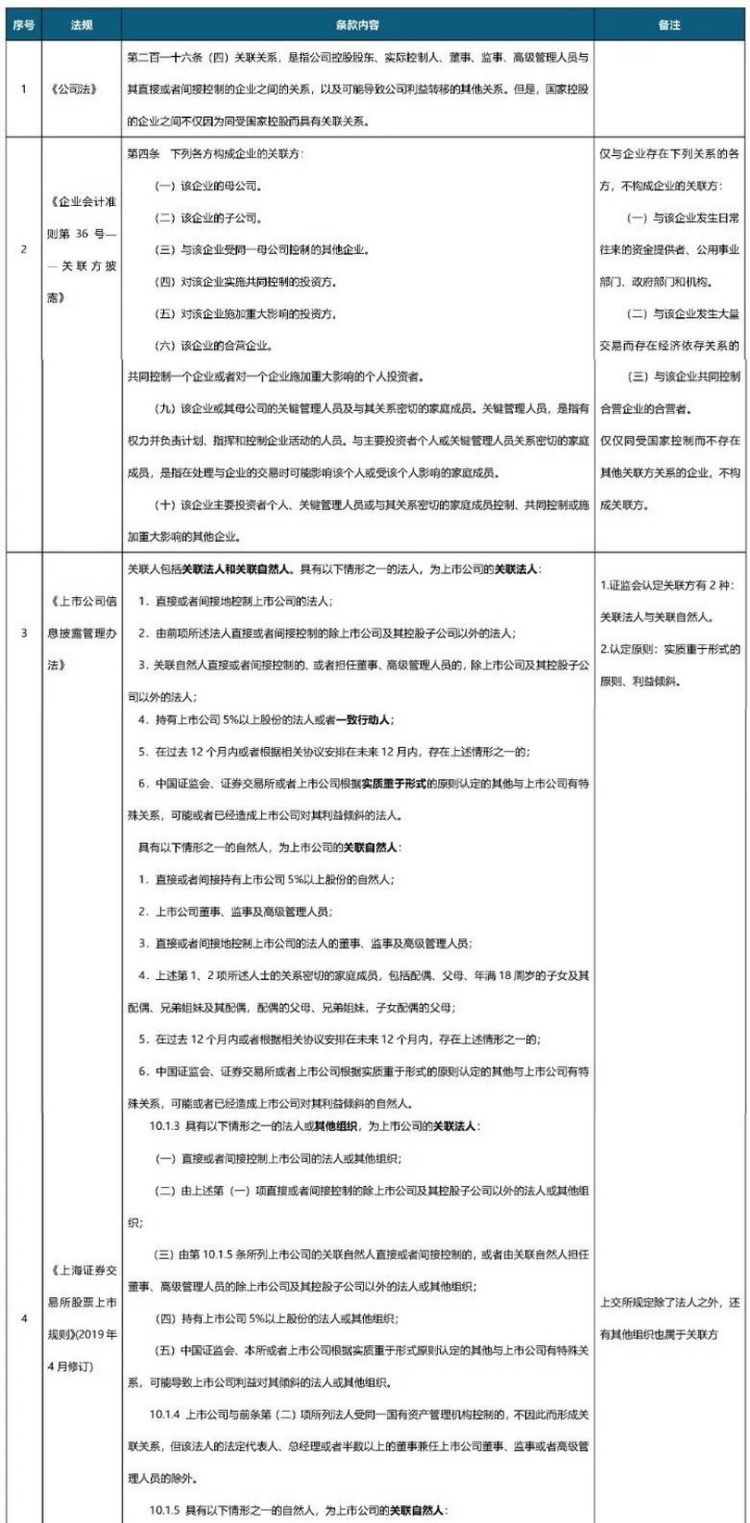

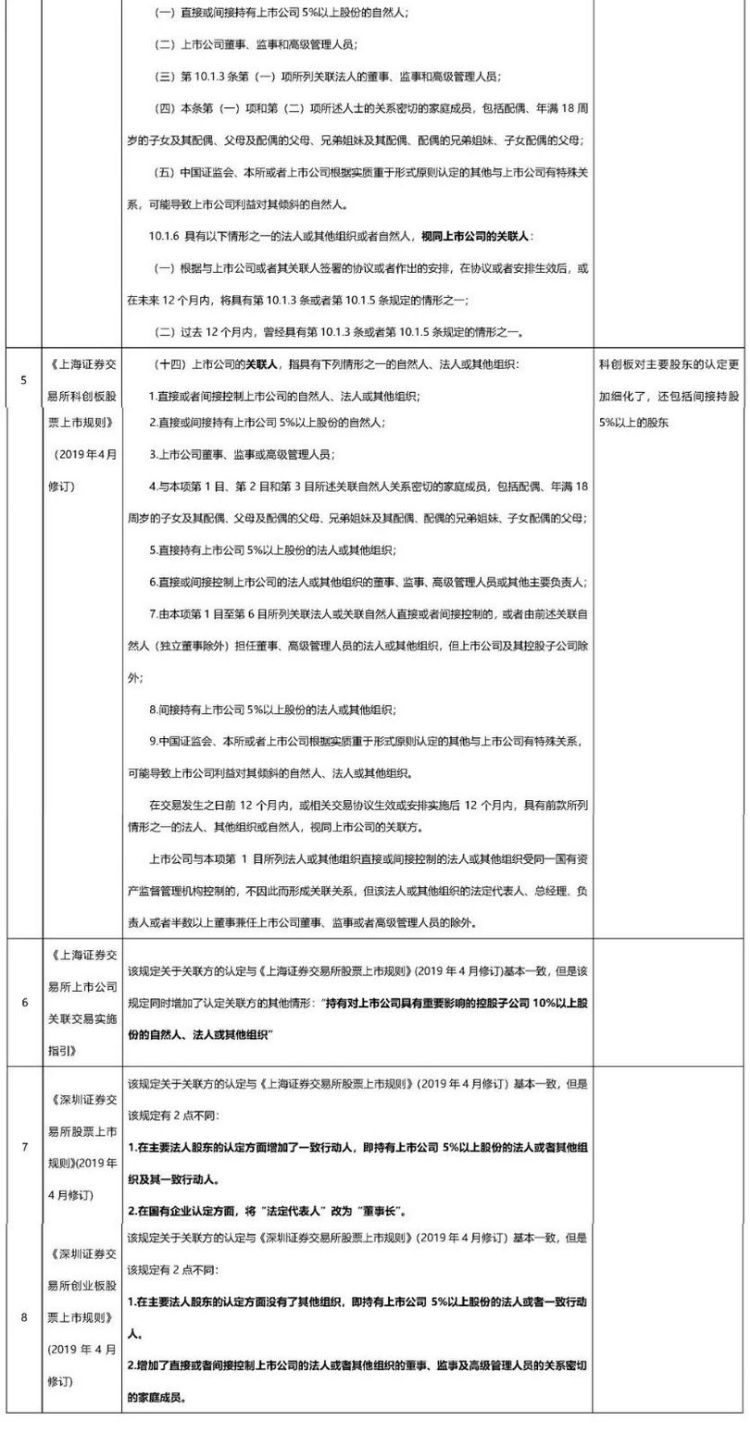

附件:"关联方"认定的主要规定:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.