INTRODUCTION

Welcome to our second report on China's Foreign Direct Investment (FDI) and outbound mergers and acquisitions (M&A) activity. In this edition we set out an overview of the movement of FDI and how this translates from an offshore perspective.

Price swings in the stock markets, and a surprise currency devaluation in China in August, have fuelled fears that the Chinese economy may be slowing more sharply than was expected, putting Beijing's 2015 growth target of 7% at risk. Despite this recent volatility and continued slowdown in growth, we believe that in the medium term China will stabilise.

The OECD suggests that slowing real estate and business investment will be countered to some extent by stepped-up infrastructure investment. Consumption is set to remain robust. Urbanisation and the rapid expansion of service industries will generate employment and keep unemployment low. Enduring overcapacity in certain heavy industries should keep producer price inflation negative, and consumer price inflation down.

China's future is not without challenges, but it continues to propel itself forward. According to leading economists ANZ, by 2030 China's middle class will reach about 93% of the urban population. Ernst & Young1 predict that as many as 500 million new middle class will emerge in the next decade, and by 2030 as many as one billion people in China could be middle class, with impressive spending power lifting consumption share in GDP.

China's business and regulatory environment also continues to evolve and it has matured and grown rapidly over the past decade. China is making significant moves in liberalising its financial sector, by opening up its bond markets and introducing a fund recognition scheme between Hong Kong and China for example. Chinese policymakers' ability to manage domestic liquidity while ensuring healthy economic growth; together with the build-up of offshore RMB and guiding its gradual return onshore will also be key factors in managing liquidity going forward.

Overseas Chinese M&A expanded rapidly in 2014, and so far 2015 looks to continue this trend. There have been 281 deals publicly recorded in the first half of this year, almost as many as there were across all of 2013. Deal value is currently at USD39bn, ahead of the first six months of 2014.

Publicly declared Chinese outbound M&A deals look set to increase in size and number, as the government's 'going out' policy to encourage Chinese enterprises to expand internationally continues to gain momentum. We believe that International Financial Centres (IFCs) such as Hong Kong, Cayman, the BVI and Mauritius for example, will continue to play significant roles in this outgoing investment.

We hope that you find the information and analysis on the following pages of interest. As 2015 nears its end and Appleby further develops its business with Chinese enterprises and others based in China seeking offshore legal advice and services, we hope to bring you further analysis.

Please do not hesitate to get in touch should you wish to discuss anything further.

IN BRIEF: FOREIGN DIRECT INVESTMENT (FDI)

Foreign Direct Investment (FDI) is an investment that acquires a significant and lasting stake in an enterprise, operating in an economy not of the investor. FDI is reported both from an inward perspective (i.e. which countries are investing into Country X) and an outward perspective (i.e. Country X is investing into which countries).

FDI statistics measure two different concepts - flows and stocks:

Flows: a measure of annual levels of investment; tend to vary significantly year-on-year.

Stocks: a measure of the total value of investments by or in a country at year-end. These are therefore subject to changes in exchange rate and valuation in company accounts.

CHINESE OUTWARD FDI

FDI Flow

According to the World Investment Report produced by the United Nations Conference on Trade and Development (UNCTAD), global FDI inflows in 2014 declined 16% to USD1.2 trillion, following recent lack-lustre growth in the global economy. In contrast to this, China's outbound direct investments rose 14% year on year to USD123 billion in 2014, according to figures provided by MOFCOM the Chinese Ministry of Finance. This follows last year's landmark, when China's outbound FDI exceeded USD100 billion for the first time. Just 10 years earlier, outbound investment was only USD3 billion. The outbound increase eclipsed the growth in FDI into China, which means China became a net capital exporter for the first time.

China's overseas investment has historically been dominated by state-owned enterprises (SOEs), but the role of private firms surpassed centrally-administered SOEs for the first time in non-financial outbound direct investments (ODI) in 2014. Private enterprises do not always have the same access to incentives and state support as SOEs, but they are often seen as being more dynamic and quicker to adjust to market conditions.

Though mining remained the number one sector with the most ODIs, the volume plunged 48% to USD17.9 billion due to the continuous depression of the global commodity market. Outbound acquisitions and investments in manufacturing and the energy supply sector were notable stand outs in 2014.

Last year, China relaxed regulations for the management of outbound investment, streamlining procedures and allowing domestic enterprises to invest in more sectors abroad. With the relaxation of these rules, China's outbound investment is likely to continue to rise.

Hong Kong remains the largest single recipient of Chinese FDI, providing a well-recognised launch-pad for further international investment. Adjacent Asian economies also do well and together with the Middle East account for more than USD14bn of investment. North America and Europe have both seen a surge of investment into them.

In its Outlook for China 2015 report, Ernst & Young has forecast that China's outbound direct investment will maintain an annual growth of more than 10% in the next five years, thanks to on-going economic reforms and favourable government policies. Early figures for 2015 from MOFCOM appear to support this, showing that non-financial outbound direct investment alone rose to USD77 billion, for the first eight months of the year. China's slowing economy and market volatility is driving domestic firms to acquire foreign brands and technology, as well as diversifying. Companies are also looking to buy overseas financial institutions that are yielding strong cash-flow and providing an international presence and market share.

Hong Kong accounted for USD71bn (58%) of the 2014 total. This is, of course, in part due to its role as an intermediary of flows between China and the rest of the world. It is extremely likely that further Chinese offshore investment continues to be routed through Hong Kong, which invests the vast majority of its own FDI into offshore jurisdictions and mainland China. Acquisitions by China that are conducted through outside regions like Hong Kong are not reflected in China's outward FDI.

FDI Stock

By the end of 2014, China's accumulated outward FDI stock volume stood at USD883bn. As the development of China's outward FDI is fairly contemporary, its size is far less than that of developed countries; only 56% of the UK's for example. Nevertheless, it is increasing rapidly and is now ranked number eight globally, surpassing Canada and Switzerland.

By the end of 2014, China's outward FDI stock had spread across 186 countries. Hong Kong alone accounts for USD510bn, followed by the British Virgin Islands and the Cayman Islands.

The profile of Mauritius has been gradually rising within China. An agreement was recently signed that will allow for 56 flights a week between the two countries, as business and tourist links continue to strengthen. Chengdu has become the fourth Chinese city to have a direct flight to Mauritius, following Beijing, Shanghai and Hong Kong.

The Crown Dependencies of Guernsey, Jersey and the Isle of Man are not reported separately from UK data, so their share remains unknown.

HONG KONG FDI

The latest available figures for Hong Kong are from 2013 and show that FDI inflow into Hong Kong resumed growth, reflecting the relative improvement in the global investment climate after the European debt crisis and US fiscal cliff subsided. The positions of direct investment into and out of the jurisdiction remained large relative to the size of the economy. This is a manifestation of Hong Kong's competitive strength as an international financial and business centre.

Mainland China continued to feature prominently in Hong Kong's external direct investment, both as a source and as a destination, accentuating Hong Kong as an ideal platform for both Chinese companies to enter the global markets and large multinationals looking to expand their business within the People's Republic of China (PRC). Looking ahead, we believe that investment activities between China and Hong Kong will continue to grow amid the deepening economic reforms to the Chinese economy, strengthening economic integration between China and Hong Kong and further development of offshore Renminbi business in Hong Kong.

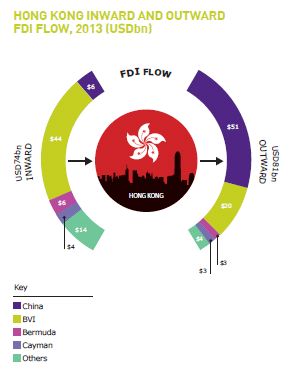

FDI Flow

The BVI was the main source of Hong Kong's FDI inflow in 2013, followed by the PRC. Hong Kong Enterprise Groups (HKEGs) involved in investment and holdings, real estate, professional and business services attracted the largest amount of FDI inflow for the year.

Banking remained popular while insurance returned to positive growth following a retrenchment the previous year.

China accounted for a predominant share of Hong Kong's FDI outflow in 2013, also with HKEGs engaged in investment and holdings, real estate, professional and business services taking up the largest amount.

After the BVI and China, Bermuda and Cayman were the next most active countries, both for flow into and out of Hong Kong.

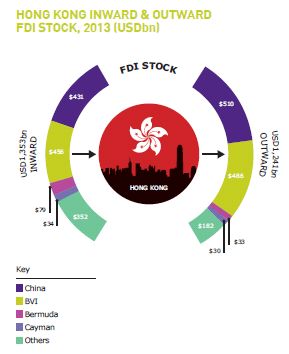

FDI Stock

Analysed by immediate source of investment, at the end of 2013 the British Virgin Islands was the most important source for Hong Kong's inward direct investment stock, making up a third of the total. China was the second largest source of investment, accounting for 32%.

When analysed by major economic activity, HKEGs engaged in investment and holding, real estate, professional and business services claimed the largest share of Hong Kong inward FDI as at the end of 2013, with just over two-thirds of the total position. The increase in the position of FDI stock in 2013 was mainly attributable to the positive FDI outflow from HKEGs to enterprises outside Hong Kong.

Looking at the immediate destination of investment, China was the top destination for Hong Kong's outward direct investment stock, with a share of 41% of the total. In particular, Guangdong Province remained a key location for Hong Kong's investment in the PRC. The most common economic activities undertaken by Hong Kong's direct investment enterprises in China were import/export, wholesale and retail trades; information and communications; investment and holdings, real estate, professional and business services; and manufacturing. The BVI was the second largest destination for investment, accounting for 39% of the total position of Hong Kong's outward FDI stock at end 2013.

Both inwardly and outwardly, Bermuda and Cayman were the most popular jurisdictions after China and the BVI, followed by a variety of other countries including the USA, Singapore and the UK.

CHINESE M&A ACTIVITY

Overseas Chinese M&A expanded rapidly in 2014, and so far 2015 looks to continue this trend. There have been 281 deals publicly recorded in the first half of this year, almost as many as there were across all of 2013.

Publicly declared Chinese outbound M&A deals look set to increase in size and number, as the government's 'going out' policy to encourage Chinese enterprises to expand internationally continues to gain momentum. This M&A activity has traditionally centred on mining and manufacturing targets as these provide the most obvious returns as they directly benefit the Chinese growing economy and its massive demand for resources and consumer products. However, future M&A is likely to extend to US and European marquee brands and technology firms. These provide Chinese firms with established overseas brands to quickly build market share and advanced technology to bring superior products back home for its 1.3 billion consumers. Notable examples include the acquisitions of Pizza Express and Club Med by Hony Capital and Fosun respectively.

After the United States, Hong Kong is a top target of overseas deals, as it continues to provide a safe and well-structured outlet for Chinese investment, and an excellent infrastructure to support its 'gateway to the world' reputation.

In a similar vein, the offshore locations of Cayman, Bermuda and the BVI continue to provide an important service to Chinese outward investment, providing legal stability, access to international capital, financial security and a neutral venue, all of which cannot be guaranteed on the Chinese mainland. Elsewhere, there are familiar targets such as Australian mining companies and European manufacturing companies. Interestingly, there is also investment in these countries in the supporting finance industries, with stakes being taken in banking and insurance.

IPO Activity

Offshore IPO activity in 2015 remains buoyant and the data shows that the vast majority of offshore IPOs announced or debuted in this period, headed to the Hong Kong Stock Exchange (HKEx). We will watch carefully the impact of the stock market votality and devaluation of the RMB that commenced in the middle of Q3 2015.

A wide variety of companies choose to list on the HKEx. Recent offshore examples include Dali Foods Group Co., Ltd, a snacks manufacturer which announced in June of its decision to list and raise up to USD 1.5 billion, IMAX China Holding Inc., a cinema operating holding company which may raise around USD300 million and Suchuang Gas Corporation Ltd, a provider of gas transmission services making 25% of its shares publically available for approximately USD50 million.

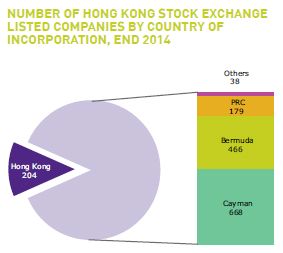

Bermuda and Cayman incorporated companies make up three quarters of listings on the HKEx. The Cayman Islands and Bermuda are the two offshore jurisdictions whose shareholder protection regimes are considered comparable to Hong Kong's, which in practice means that companies incorporated there do not have to go through a long, expensive process to establish the "acceptability" of their jurisdiction prior to listing.

Footnote

1. ‘Hitting the sweet spot’ EY report on the growth of the middle class in emerging

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.