- within Strategy, Environment and International Law topic(s)

- with readers working within the Aerospace & Defence and Media & Information industries

- The potential for the development of equitybased crowd-funding under the current legal framework

Similar to P2P lending (peer-to-peer lending), equity-based crowd-funding is a kind of public capital raising. Equity-based crowd-funding is a collective effort to provide finance in support of third party projects with a certain portion of equity as reward, incentivizing investors by allowing them a piece of the pie in a budding startup. Crowd-funding is the practice of raising money from the public and is subject to relevant laws governing fundraising, such as The Securities Law, the Criminal Law and various interpretations and opinions on the handling of criminal cases involving illegal fundraising (Fundraising Regulations) by the Supreme People's Court and other organs. Equity-based crowd-funding generally involves the transfer of equity in corporations, and is also regulated by the Corporate Law and other relevant regulations.

- Possible legal space of equity-based crowdfunding under the Fundraising Regulatory framework

Certainly, Article 6 of Interpretation of the Supreme People's Court of Several Issues on the Specific Application of Law in the handling of Criminal Cases about Illegal Fund-raising (Interpretation) is the most directly relevant clause defining equity-based crowdfunding. It states that "whoever, without the approval of the relevant competent department of the state, issues shares or corporate or enterprise bonds to unspecified people, or does so in such disguised form as transferring equities, or issues shares or corporate or enterprise bonds or does so in disguised form to a specified 200 persons or more cumulatively shall be deemed to have 'issued shares or corporate or enterprise bonds without authorization' as prescribed by Article 179 of the Criminal Law. If a crime has been committed, the offender shall be convicted of and punished for the crime of issuing shares or corporate or enterprise bonds without approval." Article 6 of the Interpretation is derived from the definition of the public issue of securities stipulated in Article 10 of the Securities Law1 . Since investors aim to gain a benefit from their investments, crowdfunding is in theory also regulated by the Securities Law2 . The transfer of equity to nonspecific persons and/or to more than 200 specific targets is deemed to be an issue of securities to the public and is subject to approval by state administration. Pursuant to Article 179 of the Criminal Law, constituting the crime of the "issue of shares or company and enterprise bonds without authorization" requires an element of huge amounts or with severe consequences or other serious acts. Based on the relationship among the seven crimes dealing with illegal fundraising,3 issuing shares or company and enterprise bonds in a disguised form not fulfilling the requirements of huge amounts or with severe consequences or other serious acts may still constitute taking deposits illegally from the general public under Article 176 of the Criminal Law.

In China, the qualification requirements and approval standards for the public issue of securities are highly rigorous and thus, it is unlikely that small and medium-sized enterprises (SMEs) and start-up enterprises will be eligible for the public issue of securities. Furthermore, the cost of publicly issuing securities is far too high to be borne by SMEs and start-ups, and is too expensive compared with the amount of the capital raised. Thus, it is unrealistic for SMEs and start-ups, to conduct fundraising by strictly complying with the requirements for a public issue of securities because the approval standards required by the state administration are unlikely to be met. For the purpose of avoiding the risk of being an illegal fundraising, equity-based crowd-funding is better to use private placement, instead of public advertising of the offering. This means the number of investors will be specific and no more than 200.

- Possible legal space of equity-based crowd-funding under the Corporate Law framework

The transfer of shares is also governed by the Corporate Law. Article 24 of the Corporate Law states that "a limited liability company shall be established by no more than 50 shareholders that make capital contributions." In other words, the number of shareholders in a limited liability company cannot exceed 50. Upon the completion of a shares transfer, the transferee will immediately be a new shareholder of the company. So if a company raising funds is a limited liability company, even if it is raising equity privately, at no time can the number of investors exceed 50.

- Summary

Based on the aforesaid laws and regulations, it is almost impossible to conduct equitybased crowd-funding in China as the country's laws have limited the number of investors to no more than 200, which is a fewer number than the number defining an entity required for equity-based crowd-funding. The purpose of crowd-funding is to raise small amount of funds from a large number of people with each person contributing only a small amount to the whole project. It is highly unlikely that a public fundraising can be conducted via a public issue in accordance with the laws and regulations. For that reason, there are only two routes that SMEs and start-up enterprises can take for equity-based crowd-funding, namely through legal private equity funding or an illegal public issue of securities. Assuming that both ways satisfy the financial demands of SMEs and start-up enterprises, entrepreneurs would rationally choose the legal option. However, the main issue is that capital raised by private equity is not usually sufficient for the financial needs of SMEs and start-ups.

- Possible solutions for equity-based crowd-funding under the current legal framework

SMEs and start-up enterprises almost always experience difficulties raising funds publicly and thus private placement tends to be the only legitimate way for equity-based crowd-funding. Private equity has strict requirements regarding promotion, the objects of the fundraising and the number of investors. Firstly, it cannot be promoted in public. Secondly, the fund can only be raised from specific investors, instead of from the public. Lastly, the sum of specific investors must not exceed 200 in total. As discussed previously, for private equity fundraising by a limited liability company, due to the restriction on the number of shareholders, the number of the investors cannot exceed 50.

- Possible solutions to circumvent the restrictions on promoting a fundraising

Subject to the restrictions of non-public promoting and the specific target of placement, most equity-based fundraising platforms are applying a membership system to investors. Investors have to be qualified as members of the platform and must obtain approval before being given information about projects. Approval requirements may vary between different membership systems.

- Possible solutions to circumvent the restriction on the number of investors

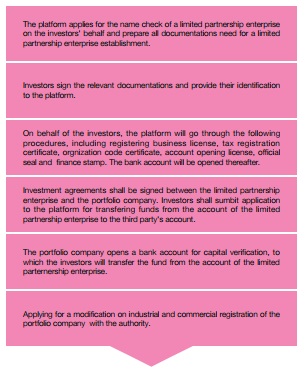

Most platforms generally hold shares in the form of a special propose vehicle (SPV), given that the number of specific investors is limited to no more than 200 and because there is also a limit on the number of shareholders in a limited liability company. Unlike investors in private investment funds who are wealthier, more experienced with investments and have greater capability in managing risk, most investors that invest in SMEs and start-up enterprises are ordinary people with limited funds, limited investing experience and poorer capability in managing risk. Given that the typical amount invested per investor in SMES and start-ups is not substantial, the financial needs of SMEs and start-ups are unlikely be met given that there is a restriction on the number of investors allowed.4 As a result, many platforms will use the SPV to evade regulations such as the Securities Law, the Corporate Law , etc. The process is shown in the following flowchart:

- Legal risks in the operation of equity-based crowd-funding platforms

As mentioned above in section 2, due to the restrictions regarding promoting a fundraising and the number of investors, there are only two routes that platforms can take to get around the restrictions. This section will mainly focus on analyzing the legal risks of using those two methods.

First, in order to satisfy the requirements of a non-public fundraising from specific persons, most platforms select potential investors by way of a membership scheme. However, the Securities Law remains silent on the criteria for selecting qualified investors. Based on the standard practices of other countries, there are three attributes that a qualified investor could possess, namely a. investing experience; b. a special connection to the issuer; and c. an investment threshold.5 The criteria for determining these three attributes will not be discussed further, and only a few platforms have set up their own threshold for membership based on them. For some platforms, the investors can easily obtain a membership by filling out a form which requires their name and ID numbers. Without being able to verify the authenticity of information provided, it is doubtful that the requirement for a non-public promoting of a fundraising from specific targets would be fulfilled.

The other issue is the operation of an SPV. The Interim Measures for the Supervision and Administration on Privately-Raised Funds (Interim Measures) promulgated and effected by CSRC on Aug 21, 2014 may provide some clarification. Article 13.2 of the Interim Measures stipulates that "if the capital of many investors collected in unincorporated entities such as a partnership or by contract are directly or indirectly invested in private funds, private fund managers or private fund distributors, the promoters must verify whether the ultimate investors are accredited investors and must calculate the aggregate number of investors." Furthermore, one of the drafters of the Interpretation also claims that when considering the number of persons that would constitute illegal fundraising stated in Article 3 of Interim Measures, "fund raising by persons on various levels is common in practice. In light of that, the number of persons shall be summed up from all levels".6 For that reason, the ultimate investors in a SPV must be reviewed thoroughly and be calculated cumulatively, in other words, the SPV structure is not workable. If in the future an exemption is given for small scale crowd-funding, the regulations on the number of investors may be loosened or abandoned completely. Using an SPV to attempt to evade restrictions may be illegal at present.

- Analysis of the regulation of equitybased crowd-funding

Unlike equity-based crowd-funding, a public offering tends to raise a larger amount of money. In order to protect the interests of investors, the Securities Law stipulates a series of provisions regulating public offerings, including statutory conditions to issuing, obligations of continuous information disclosure etc. The small amount of money raised by crowd-funding is insufficient to cover the vast cost of a public offering. The risk management for public investors can be achieved in ways other than by approval of a public issue and its strict conditions of information disclosure. Usually in a company involved in a crowdfunding project, the degree of separation between ownership and management is much lower than the one in a public company. Given the small sum of funds invested by each investor in crowd-funding, unfavorable occurrences tend to be easier to handle and deal with. Hence, an exemption system with lower standards for granting approval and less onerous information disclosure could be designed by regulation. In order to manage risk, the investment amount for each individual investor could be capped, instead of the number of investors, and the risk of loss could then be shared by investors accordingly. Instead of the detailed and strict requirements for a large scale capital raising it would be appropriate to loosen the information disclosure and supervision of crowd-funding platforms.

Footnotes

1 The conditions set forth by laws or administrative regulations must be satisfied in the public issue of securities, and such issue must, pursuant to law, be submitted to the securities regulatory authority under the State Council or the departments authorized by the State Council for examination and approval. Without such examination and approval pursuant to law, no entities or individuals shall issue securities publicly.

Any one of the following circumstances shall constitute a public issue:

- issuing securities to non-specific persons;

- issuing securities to more than 200 specific persons in the aggregate; and

- such other issuing activities as may be so prescribed by laws or administrative regulations. Where securities are issued in a non-public manner, no advertising, public solicitation or any other covert ways in disguised form shall be employed.

2 See Legal Structure in Equity-based

Crowd-funding by Peng Bing (in Chinese).

3 See Preventing Legal Risks from Private

Equity by Wang Lixin and Wang Peng (in Chinese).

4 See Major Legal Issues and Risks on Crowd-funding

in e-Financing Era by Zhang Xiaoquan and Zhang Bowen, China

Bulletin Issue No. 77, August, 2014.

5 See Clarifying Margins of Illegal Fundraising:

Commenting on Interpretation of Illegal Fundraising by the Supreme

People's Court by Peng Bing, Legal Professions, Issue No.

6, 2011.

6 See Analysis and Application on Interpretation on

Several Practical Issues of Criminal Cases Trail of Illegal

Fundraising by Liu Weibo, People's Jurisdiction, Issue

No.5, 2011.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.