This Client Alert looks at some of the recent changes, issues and challenges facing those interested in the derivatives market in the PRC and Hong Kong. We look at the recent draft regulations issued by the CBRC, the CIRC's decision to allow all insurers to enter into interest rate swaps, possible changes that are ahead for the NAFMII Master Agreement, signs of development in the CDS market in the PRC and recent changes ISDA have announced to its credit derivative novation process.

CBRC Releases Revised Draft Regulations on Derivatives

Regulators around the world are taking a closer look at the use and regulation of derivative products. We are seeing this with the Dodd-Frank Act in the US and proposals for new measures in the EU, the UK and Australia - and China is no exception.

In July 2009, the national banking supervisory body, the China Banking Regulatory Commission (CBRC) promulgated the Notice on Further Strengthening Risk Management for Derivative Transactions between Banking Financial Institutions and Corporate Clients (CBRC Circular No. 74) which imposed restrictions on the ability of onshore (domestic) banks to engage in derivative transactions with their corporate clients and a significant ongoing administrative burden on both those banks and their clients, including an enhancement of client suitability verifications and risk disclosure measures (click here for a copy of CBRC Circular No. 74).

Now, following increased concern in China about the trading of leveraged, complex and what are termed "opaque" derivatives, as well as a disquiet about derivatives transactions that are felt to be "irrelevant to the needs of the real economy", the CBRC is considering imposing further regulation and has recently issued the draft Administrative Regulations on Derivative Products Transactions Business of Financial Institutions (金融机构衍生产品交易业务管理办法) (the Draft Regulations) to solicit public comments.

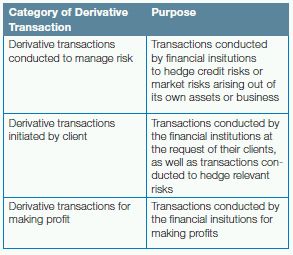

In summary, the main amendments proposed by the Draft Regulations are:

- clarifying that the regulations governing derivatives apply to financial instruments with embedded derivatives and spot transactions with delayed settlement of not less than three days;

- classifying derivative transactions into one of three

categories, depending on its purpose:

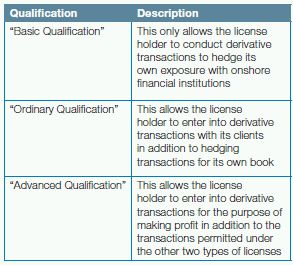

- classifying derivative licenses into one of three

categories:

- requiring a financial institution to obtain a "no objection" letter from the CBRC before selling complicated financial products which are new to the domestic market; and

- requiring that a financial institution obtain the license to trade on the spot market of the relevant reference assets before it may enter into FX, equity, commodity derivatives or exchanged traded products.

Coming only six and a half years after the CBRC promulgated China's first ever procedures to address the regulation of derivatives trading (with the promulgation of the Administration of Trading of Derivatives by Financial Institutions Tentative Procedures in March 2004), this shows remarkable progress and it is anticipated the Draft Regulations, which also incorporate the requirements in the CBRC Circular No. 74, will be formally published later this year.

We have a copy of the Draft Regulations and an English translation - clients and other interested parties can contact any of the O'Melveny & Myers lawyers listed on cover if they would like a copy.

CIRC: All Insurers Now Permitted to Enter into interest rate swaps

Following the conclusion of a four-year pilot programme during which selected insurers were authorized to enter into interest rate swaps (IRS), in July 2010 the China Insurance Regulatory Commission (CIRC) promulgated The Circular on the Engagement in Interest Rate Swaps by Insurance Institutions (中国保险监督管理委员会关于保险机构开展利率互换业务的通知) (the Circular) which allows all insurance institutions to enter into IRS.

An IRS is defined in the Circular as "a financial contract whereby both parties to the transaction agree to exchange interest calculated according to the agreed principal and interest rate within a certain time period in future" (Article 1). The Circular states that insurers are only to use IRS as a hedging tool to avoid interest rate risk (and not for speculative purposes or leveraged transactions) and requires the insurer to have proven risk management capability and prior approval from its board of directors. Limits have also been imposed on the nominal amounts involved (which should not exceed 10% of an insurer's fixed-income assets (including bank deposits, bonds and other debt instruments) at the end of the preceding quarter, with a further cap for IRS with the same counterparty) (Article 5).

Changes Ahead for the NAFMII?

In the Spring of 2009, the National Association of Financial Market Institutional Investors (NAFMII) published its China Inter-bank Market Financial Derivative Transactions Master Agreement to much acclaim. This Agreement was designed to replace both the previous version of the NAFMII Master Agreement (published in 2007) and the National Interbank Foreign Exchange Market RMB-FX Exchange Derivatives Master Agreement released by China Foreign Exchange Trading System (CFETS) in 2007. Having two sets of documentation had created issues for the market (including possible confusion, administrative burden and costs and netting concerns) and the single NAFMII master agreement addressed many of these.

The NAFMII Master Agreement, which governs all financial derivative transactions in China, was widely taken up but has recently faced criticism that it needs greater technical depth (for example, NAFMII Definitions are just over 20 pages in length whereas the similar definitions from the International Swaps and Derivatives Association (ISDA) stretch to over 140 pages) and to cover more asset classes (in particular, the NAFMII Master Agreement doesn't cover commodity derivatives, a booming market in the PRC).

In August 2010, NAFMII met with certain key members (including onshore and offshore banks) as a result of which it is expected that several key working groups will be set up to look at these issues.

CDS: Coming Soon to A Market Near You?

There are reports that China's central bank is considering rules to foster the creation of new derivative products. One area where we are seeing this is the nascent development of credit default swap (CDS) products. In the past, plans for a CDS pilot project in China have been postponed in the face of various concerns, including worries that the country's bond market is too immature (in a recent speech, Zhang Guangping, deputy director-general for the CBRC in Shanghai, said he believes three conditions need to be met in China before allowing CDS to trade onshore: a deeper corporate and enterprise bond market, a more active interest rates derivatives market and for credit rating agencies to be better developed). However, there are no doubts that the that bond market in China is expanding rapidly (reports state that in the first half of 2010, corporate debenture issues on China's interbank bond market totalled RMB 780 billion and debenture bonds under custody hit RMB 3 trillion) and the People's Bank of China (PBOC) and other regulatory bodies, including the CBRC and NAFMII (which would have responsibility for drafting the definitions for onshore credit derivative transactions) have been studying the feasibility of developing a credit derivatives market to hedge and mitigate credit risks, in response to market needs.

At the end of July 2010, Shi Wenchao, secretary general of NAFMII, announced that China was expected to launch its first CDS products this year. This was quickly followed by the launch of a pilot CDS project named "Optional CBIC 1". According to press reports, the product was designed by China Bond Insurance Co. Ltd., issued to Chongqing Chemical & Pharmaceutical Holding Group Co. on 13 July 2010 and underwritten by Industrial Bank Co. Ltd.

Nevertheless, some of the Chinese regulators including the CBRC, are still reported to have concerns and not many market participants expect that these shall be to be addressed any time soon.

ISDA Announces Changes to Its Credit Derivative Novation process

On 25 August 2010, the International Swaps and Derivatives Association (ISDA) announced a new project to streamline the novation process for credit derivative trades. This will be done by way of ISDA's "Credit Consent Equals Confirmation" project which will implement a process allowing parties to provide consent to and legal confirmation for a novation simultaneously by an automated, single-step process (rather than the existing two-step process of consent plus confirmation).

ISDA has published Additional Provisions for Consent to, and Confirmation of, Transfer by Novation of OTC Derivative Transactions on its website. These provisions amend the rules in the ISDA Novation Protocol to allow the changes to the novation process to take effect without requiring parties to re-adhere to the Novation Protocol.

The project will go live on Thursday, 30 September 2010 and more details (including the Provisions referred to above) are available on the ISDA website (click here).

O'Melveny & Myers LLP routinely provides advice to clients on complex transactions in which these issues may arise, including finance, mergers and acquisitions, and licensing arrangements. If you have any questions about the operation of the applicable statutory provisions or the case law interpreting these provisions, please contact any of the attorneys listed on this alert.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.