The following article appeared in Global Custody.net on June 18, 2015.

For hedge fund managers marketing and raising capital in Europe, the rollout of Annex IV has raised a number of questions. Better known to US firms as 'Europe's Form PF', this regulatory reporting requirement under the Alternative Investment Fund Manager Directive (AIFMD), while challenging, should not deter managers from pursuing the rich opportunities that Europe continues to offer.

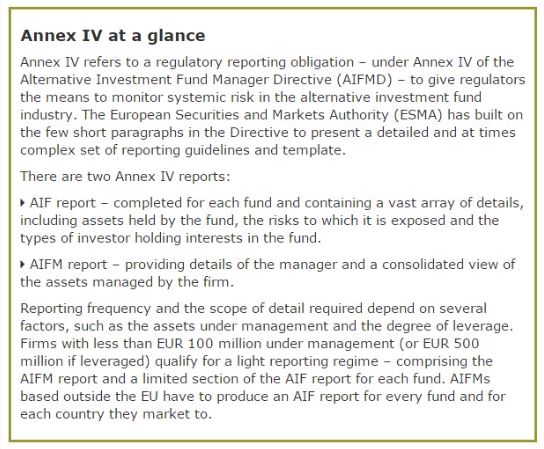

Essentially, Alternative Investment Fund Managers (AIFMs) are subject to Annex IV reporting if they have a presence within the European Union (EU) or European Economic Area (EEA) or if they market into an EU member state.

"The Annex IV reporting obligation is certainly onerous, with added demands where regulators in some countries have taken the template shaped by the European Securities and Markets Authority and adopted 'gold plating' – with even more stringent requirements," says Jason Poonoosamy, Risk Director at DMS Offshore Investment Services (Europe) Ltd.

Dublin-based Mr Poonoosamy distinguishes Annex IV from Form PF, pointing to its much more prescriptive nature and tighter reporting time frames, "typically 30 days after the end of the quarter, against 60 days for the US Securities and Exchange Commission (SEC). But just as with the introduction of Form PF and its commodity equivalent CPO-PQR, the infancy of Annex IV has seen many issues emerge." In discussion, we consider seven pertinent matters.

Data protection and confidentiality

Like their US counterparts, European regulators have clearly stated that their aim in collecting Annex IV data is to monitor and understand systemic risk within the global financial system. Consequently, all data is solely for regulator use.

Lack of clear definitions and guidelines

The subjective nature of some items, such as geographical exposure, unencumbered cash and risk sensitivities may result in inconsistencies when aggregating data at a European level; this will skew any conclusions and may compromise the regulators' aim of industry-wide risk monitoring. Clear dialogue between industry and regulators is needed.

Inapplicability of some 'required' answers

For a private equity or infrastructure fund, reporting stress test and value-at-risk results is not meaningful. Real estate funds should not be treated in the same vein as those investing in financial securities, and so Annex IV should be tailored accordingly.

Assets under management and leverage

The prescriptive nature of computing these metrics can result in inflated values, and hence higher reporting frequency and more onerous filing requirements for some. An approach that requires managers to report along the lines adopted for internal and investor purposes is more effective.

Filing frequency: over-complex decision tree

The self-assessment requirement and automated notification process of many regulator reporting portals – which are not necessarily accurate – have meant that many managers are unsure of when they need to submit. Straightforward, simplified and logical criteria are needed to ensure that managers are properly fulfilling their obligations.

Disparate submission methods across regulators

Some regulators are only accepting certain file types (e.g. XML), while others require submission through their portals. Ideally, a single portal for all submissions should be made available. From a regulator's perspective, this simplifies the aggregation process and easily permits the dissemination of data as applied at a national level.

Feeder-level reporting

Initially, there was no requirement for feeder funds to look through to the master when reporting. However, it appears that some regulators – most notably those in Luxembourg and Belgium – have since sought a clearer picture of each fund's effective exposure. As with the SEC's Form PF, ESMA should mandate aggregate master-feeder reporting.

In conclusion, Mr Poonoosamy notes: "The eagerness of managers to provide accurate and consistent data should be embraced by regulators, with an open, interactive forum for discussion. Such an approach will result in meaningful insight for regulators, and help them ultimately achieve their goals."

In terms of immediate needs, managers may want to explore the resources available to help them efficiently and accurately meet their Annex IV requirements. Choices between in-house versus outsourced solutions should be carefully considered, taking into account existing arrangements for other reporting requirements. Furthermore, the cost of Annex IV should be considered in the context of a firm's European strategy – for example, whether to register and report in multiple jurisdictions or use a third-party management company and hence avail the firm of the accompanying fund passport.

As with any industry-changing initiative, AIFMD has introduced inevitable challenges and questions. During these early stages, managers should continue to remain mindful of the enhanced investor confidence generated by the regulations and the consequential rewards this will bring.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.