On March 19, 2015, the Cayman Islands Tax Information Authority ("TIA") officially opened the Cayman Automatic Exchange of Information ("AEOI") Portal.

Please click here for a copy of the communication and below for KPMG's comments on the Reporting and Notification process.

Reporting Process

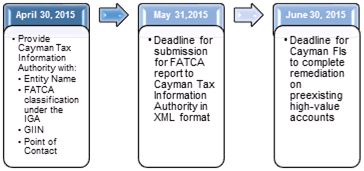

The TIA indicated that the Portal is now available for Cayman Islands Reporting Financial Institutions ("Cayman Reporting FIs") to submit their Notification (due by April 30, 2015) and Reporting (due by May 31, 2015) to the TIA. Refer to the "Key Dates in 2015" section below for details required to be submitted as part of the Notification process.

Key Links:

- The Notification Form can be accessed here.

- The Portal can be accessed here.

- The User Guide to the Portal is available here.

KPMG's Observations

Critically, the TIA has removed the NIL return reporting requirement for Cayman Reporting FIs. To clarify, no US or UK FATCA "nil returns" are required to be filed. For many Cayman FIs they may not have anything to file. The TIA has however noted that the Portal will accept NIL returns.

We note that the Office of the Chief Counsel at the IRS has stated that submitting a NIL return is "best practice" and that it intends to use non-filing for three consecutive years as an indicator of possible noncompliance. As the process to submit a NIL return is straightforward we expect some Cayman Reporting FIs will decide to file a NIL return annually. This will also likely be a key decision prior to liquidating any Cayman FI in an effort to close out any possible obligations.

Notification process is still required

TIA's announcement on March 19, 2015 also noted that even if a Cayman Reporting FI has no reporting requirements it must notify TIA by April 30, 2015.

Why was this change made by TIA to remove the NIL return requirement? We believe the decision by TIA to remove the "Nil Return" filing requirement was significantly influenced by the fact that the OECD Common Reporting Standard ("CRS") which comes into force in 2017 does not require "Nil Returns" to be filed as well as a similar decision made by UK tax authorities on March 11, 2015.

KPMG Cayman can assist with the Notification process including submitting the notification to the TIA on your behalf as well as filing the U.S. FATCA Return for your Reporting FI(s) for 2015. Please contact us for further details.

Have Questions?

KPMG in the Cayman Islands has a FATCA Help Desk for any questions you may have.

Key Dates in 2015:

How can we help?

KPMG in the Cayman Islands offers the following services to assist you in your preparations for FATCA:

- We can provide a detailed written summary of FATCA's impact to a Cayman Islands Financial Institution.

- We can review the FATCA policies you have implemented providing recommendations on improvements.

- We can conduct a review to ensure the process implemented remains appropriate in face of changing legislation and upcoming requirements including the OECD Common Reporting Standard ("CRS").

Click here for more details on KPMG in the Cayman Islands' FATCA services.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.