- within Employment and HR and Insurance topic(s)

Take Care – EMIR Impacts Cayman Funds

As managers of Cayman Funds are coming to grips with the reporting requirements of AIFMD1, a second wave of European legislation, namely EMIR2, approaches the Cayman Islands. EMIR will have to be navigated by Cayman Funds trading derivatives both with European Union counterparties, and in certain circumstances, even when trading with non-European Union counterparties.

Although the provisions of EMIR principally impact European entities which are financial counterparties3 ("FC's") and non-financial counterparties4 ("NFC's") as defined in EMIR, managers of Cayman funds will need to be aware of EMIR and how it might impact their funds when trading with European counterparties. In addition, provisions of EMIR relating to Extraterritoriality and Equivalence will impact third country entities, including Cayman Funds, in certain circumstances, even when they are trading with non-European entities.

What is EMIR?

EMIR is European legislation which aims to fulfil European Regulators' G20 commitments that all standardised OTC derivatives should be cleared through central counterparties ("CCPs") and that OTC derivative contracts should be reported to trade repositories ("TRs"). EMIR is also intended to address related commitments to a common approach to margin rules for un-cleared derivatives transactions.

EMIR entered into force on 16 August 2012 bringing about a new era for OTC derivatives markets and introducing the following obligations:

- risk mitigation requirements for non-centrally cleared trades; reporting to TRs;

- clearing obligations relating to standard OTC derivatives; and requirements for CCPs and TRs.

Cayman Funds trading with European Counterparties

Article 4(1)(a)(iv) of EMIR provides that OTC contracts executed outside the EU are subject to the clearing or risk mitigation measures of EMIR where one counterparty is established in the EU (and is an FC or an NFC which has exceeded the clearing threshold ("NFC+")) and the other counterparty is in a third country (ie a third county entity, "TCE",), provided that the TCE would have been subject to the clearing obligation if it were established in the EU (i.e. it would be an FC or NFC+ if established in the EU).

In the case of a Cayman Fund, it will be indirectly affected because it is not possible to clear only half a transaction. If the OTC trade is not cleared through a central counterparty ("CCP"), the Cayman fund will be required to comply with the risk mitigation measures of EMIR. This is because an FC or an NFC which transacts with a Cayman Fund will, in order to facilitate their own compliance with EMIR, be obliged to ensure that those Cayman Funds, being TCE's, comply with the risk mitigation measures of EMIR.

The risk mitigation requirements with which the TCE must comply are the requirements for (i) portfolio reconciliation; (ii) dispute resolution; (iii) timely confirmation and (iv) portfolio compression.

Extraterritoriality, Cayman and EMIR

EMIR provides that the clearing obligation and the obligations relating to the risk mitigation techniques for non-centrally cleared OTC derivatives may apply to OTC derivative contracts entered into between non-EU counterparties. In cases where TCEs that would be subject to EMIR if they were established in the EU enter into OTC derivative contracts, the clearing obligation and the obligations relating to the risk mitigation may apply if the contract has a direct, substantial and foreseeable effect within the EU or where such an obligation is necessary or appropriate to prevent the evasion of any provisions of EMIR.

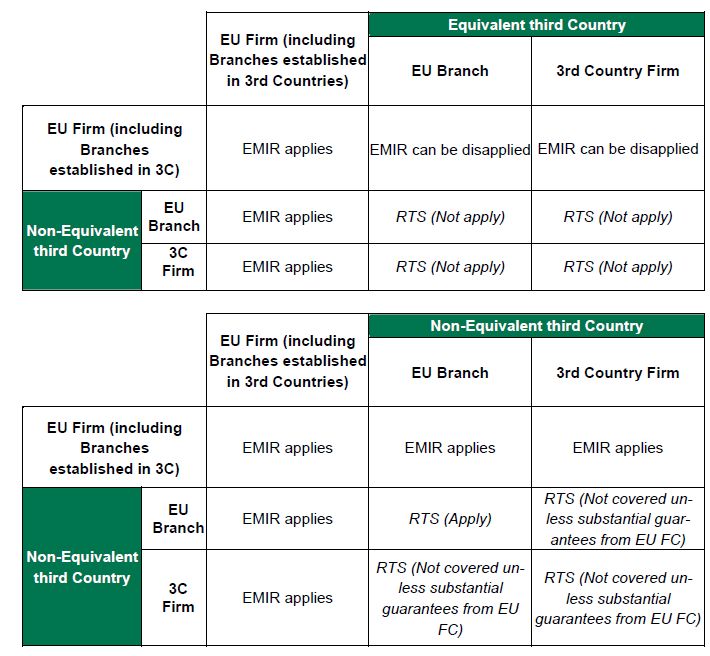

In light of this requirement, the European Securities and Markets Authority ("ESMA") is obliged pursuant to EMIR to draft formal Regulatory Technical Standards ("RTS") specifying both the contracts that are considered to have a direct, substantial and foreseeable effect within the EU and the cases where it is necessary or appropriate to prevent the evasion of any provision of EMIR. Although these RTS are not yet finalised, on 17 July, 2013 ESMA published a consultation paper containing draft RTS (the "Consultation Paper"). The Consultation Paper proposed that EMIR's clearing and risk mitigation requirements apply to transactions between TCEs when rules in both jurisdictions are not considered to be equivalent to EMIR and either:

a) one of the two TCEs is guaranteed by an EU financial counterparty for at least €8bn of the gross notional amount of OTC derivatives entered into and for an amount of at least 5% of the OTC derivatives exposures of the EU financial counterparty; or

b) both TCEs execute the transaction via their EU branches.

A summary of the scope of the application of EMIR to TCEs under the draft RTS included in the Consultation Paper and Article 13 of EMIR is as follows:

ESMA has invited comments on the Consultation Paper and will consider all those received by 16 September 2013. It is intended that ESMA will update the draft RTS following a consideration of responses to its Consultation Paper and will then send its final report to the European Commission for endorsement.

Equivalence, Cayman and EMIR

Under EMIR, the European Commission may adopt implementing acts declaring that the legal, supervisory and enforcement arrangements of a non-EU country are equivalent to the requirements laid down in EMIR relating to the clearing, reporting, non-financial counterparties and risk mitigation obligations under EMIR.

In this regard, EMIR clarifies that any implementing act on equivalence shall imply that counterparties entering into a transaction subject to EMIR shall be deemed to have fulfilled the above detailed obligations where at least one of the counterparties is established in that third country.

How Dillon Eustace Can Help

Leveraging off its European team, Dillon Eustace Cayman offers a unique perspective for its Cayman clients on EMIR.

Dillon Eustace will keep its clients and contacts up to date on EMIR developments and how they will affect Cayman funds as the consultation process is finalised. Please don't hesitate to contact Derbhil O'Riordan or Matt Mulry with any queries you might have on this or other legislative developments, Cayman, European or otherwise, where you have any concerns on the impact on your Cayman funds5.

Footnotes

1 Impacting Cayman Funds being marketed in the EU. See http://www.dilloneustace.ie/download/1/AIFMD%20Implications%20for%20Managers%20of%20Cayman%20Funds%20HFM%20Weekd%20Article.pdf .

2 EU Regulation No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories

3 The term FC is broadly defined in EMIR as a person authorised under one of the EU's financial services directives, thereby excluding Cayman Funds.

4 The term NFC is defined in EMIR as "an undertaking established in the Union", again excluding Cayman Funds.

5 Further publications on EMIR can be found at: http://www.dilloneustace.ie/download/1/EMIR%20-%20Key%20Points%20and%20Dates..pdf

http://www.dilloneustace.ie/download/1/EMIR%20-%20Update%20and%20Next%20Steps.pdf .

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.