- within Privacy topic(s)

Employees are an important asset to companies and thus, making them feel valued is imperative to enhance employee retention efforts. There are a plethora of employee benefit mechanisms adopted by employers to reward their employees for their hard work ranging from monetary compensations such as bonuses to non-monetary compensations such as healthcare benefits. Another attractive employee reward scheme that has gained traction amongst employers is the employee share option scheme ("ESOS").

ESOS is a scheme where shares are offered to employees by employers to recognise the role of employees in the development of the company by inculcating a sense of belonging amongst the employees in that they too have rights in the company by holding shares in that company.1

In this type of scheme, an employer will usually issue share options to their employees who have met a certain eligibility criteria to subscribe for new shares in the employing company. These shares offered to employees may include shares in the employing company itself, shares in the employer's holding company or shares in the employer's subsidiaries.2

Under this scheme, the employees would not be able to exercise the share options immediately but rather at a future date and at a pre-determined price. Employees will only have an absolute right on the shares when the shares are fully vested.3 Pursuant to this, most ESOS would typically provide for a vesting period before the share options can be exercised.4 These shares are only considered fully vested upon fulfilment of certain pre-conditions imposed under the ESOS which must be fulfilled by the employee in order to have the right to purchase or exercise the option to acquire the shares.5

Tax Chargeability of ESOS

The Income Tax Act 1967 ("ITA 1967") provides that income upon which tax is chargeable under the ITA includes gains or profits from an employment6and dividends, interest or discounts.7

Section 13(1)(a) of the ITA 1967 clarifies that gains or profits from an employment includes "any wages, salary, remuneration, leave pay, fee, commission, bonus, gratuity, perquisite or allowance (whether in money or otherwise) in respect of having or exercising the employment."8 Perquisites in relation to an employment of a Malaysian tax resident, according to the Public Ruling (PR) No 5/2019 issued by the Inland Revenue Board of Malaysia, means "benefits in cash or in kind that are convertible into money received by an employee from the employer or third parties in respect of having or exercising the employment." The Inland Revenue Board of Malaysia has further clarified that perquisites have the following characteristics9:

(a) Perquisites can be received regularly or casually.

(b) Perquisites can be received in cash or in kind. If it is received in kind, such items must have money's worth and are convertible into money. The phrase convertible into money means that when the items are provided to the employee, they can be sold, assigned, transferred or convertible into cash.

(c) Perquisites can be received by an employee in respect of an employment contract entered into by him or is given by the employer or a third party voluntarily.

(d) A perquisite is subject to tax only if it arises in respect of having or exercising an employment.

Premised on the fact that ESOS are a type of employment benefit, they are tax chargeable. Since the gains realised by the employees after exercising their share options is acquired as result of having or exercising the employment, these gains are tax chargeable as perquisites under Section 4(b) of the ITA 1967.

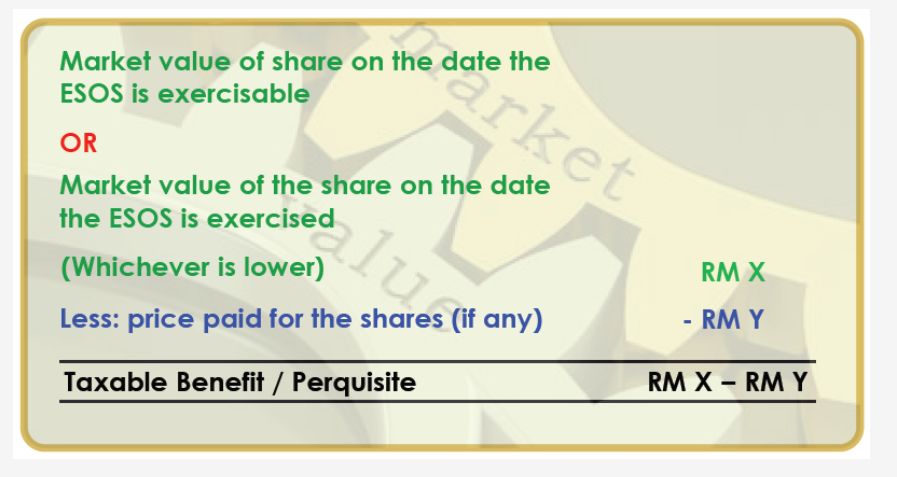

Calculation of Taxable Benefit

The taxable benefit calculated from the gains realised through the exercise of share options is the difference between the market value (i.e., share price on the day the option is exercised or share price on the first day the option is exercisable, whichever is lower) and the offer price by the employer on the date the option was awarded.10 The calculation of the taxable benefit is as shown on Table 1.

Table 1

However, it must be noted that although the benefit from the share scheme may only be realised on the date of exercise of the share option, the assessment for tax purposes would be calculated based on the year of award.11 It is also important to highlight that any gains from the subsequent sale of the shares acquired (i.e. the employee may subsequently sell the shares and realise a gain), would be regarded as a capital gain. As at the date of this article, capital gains are not taxed in Malaysia.12

Who Will be Taxed?

Since ESOS are taxable for the benefits gained after having or exercising the employment, only an employee shall be chargeable with tax from the gains realised from exercising the share options under the scheme.

A determination on whether such person falls under the category of 'employee' will be a case-to-case basis. However, some guidance can be found in Paragraph 4.5 of PR No. 11/2012 where 'employee' in relation to an employment, is defined as the subsistence of a master-servant relationship, or where the relationship does not subsist, the holder of the appointment or office which constitutes the employment. Other evidence that may qualify a person as an 'employee' also includes the existence of a contract of service or apprenticeship with an employer, regardless whether the contract is expressed or implied or is oral or in writing.

Employer's Perspective: the Tax Deductibility of ESOS

In an ESOS arrangement, employers are also bound to pay tax. The tax to be paid by employers is levied based on the expenditure incurred in making available the ESOS to its employees. This was the status quo until it was recently reviewed in the Court of Appeal case of Ketua Pengarah Hasil Dalam Negeri v Asia Energy Services Sdn Bhd13. In this case, the employer's as part of the Employee Stock Based Compensation package offered to its employees share options and in the process the employer has incurred some expenses. The Appellant argued, amongst others, that (1) ESOS expenditure is not deductible under section 33(1) ITA 1976 as it is capital in nature and therefore not wholly and exclusively incurred in the production of gross income, and (2) capital nature expenses involve the assets of the company which includes the expenses on the employees wherein the employees are assets of the company. However, such arguments were rejected by the Court of Appeal. The Court of Appeal agreed with the High Court that where a compensation (i.e., the Employee Stock Based Compensation package) is given by the taxpayer/employer to its employees as a reward for services rendered, the value of the compensation is a cost to the taxpayer/employer. As the employees' services are rendered directly to produce income for the taxpayer/employer, the compensation would therefore be deductible under section 33(1) of the ITA 1976. Another recent development which further strengthens the position that expenses incurred for ESOS are tax deductible can be seen in the High Court caseofDialog Catalyst Services Sdn Bhd v Ketua Pengarah Hasil Dalam Negeri and other cases.14

In this case, the Applicants offer to its employees share options to purchase shares in its ultimate holding company, Dialog Group Berhad, as part of its employee remuneration structure. Consequent to audits conducted on the Applicants in 2021, the Respondent found that the expenses claimed by the Applicants for the ESOS were not allowable for deduction on the ground that it is capital and caught by Section 39(1)(c) of the ITA 1976. According to the Applicants, the share options are employment benefits to its employees.

In order for the Applicants to provide employment benefits to its employees, the Applicants had to incur and pay this cost. The High court held that it cannot be disputed that employers do get a deduction for employment costs and employees need to bring employment benefits to tax. The Applicants, as part of its employee remuneration structure, offers to its employees share options to purchase shares in its ultimate holding company, Dialog Group Berhad. In the process of offering the ESOS to employees, there is a cost to the employer and the High Court held that said costs to the employer are tax deductible.

Tax Treatment of Foreign ESOS

There are certain scenarios in which foreign ESOS may be taxable in Malaysia. Where foreign ESOS are offered to foreign employees prior to their secondment to a Malaysian employer, it is necessary to determine whether the benefit from share schemes are in respect of employment exercised in Malaysia or overseas.15In the event the scope of work of the foreign employee are exercised in Malaysia (e.g., through secondment) and the income derived from the employment is taxable in Malaysia, then a charge to Malaysian tax is likely to arise on the benefit from the exercise of the share schemes offered by the employer overseas but exercised while in Malaysia.16

Additionally, a charge to Malaysian tax is also likely to arise in the event the foreign employee who is offered a share scheme by their foreign employer prior to their secondment in Malaysia only exercises their right to the share scheme after they return to their home country.17

Nevertheless, where foreign income received in Malaysia has been taxed overseas either through withholding tax or income tax, the recipient of the foreign income may claim bilateral or unilateral tax credit under Sections 132 and 133 of the ITA 1967.18 The Inland Revenue Board of Malaysia has also introduced the Income Tax (Exemption) (No. 5) Order 2022 for foreign income which provides that any foreign source of income received in Malaysia from 1 January 2022 to 31 December 2026 is exempted from any tax liability provided that the individual shall have been subjected to tax of a similar character to income tax under the law of the territory which the income arises.19 This exemption applies in the context of dividends earned from shares (arising from the exercise of a share option) being brought into Malaysia up to 31 December 2026.

Conclusion

In conclusion, ESOS are tax chargeable in Malaysia. As such, employers offering ESOS and employees holding ESOS should be aware of their tax obligations under the ITA 1967, specifically under Sections 4(b) and 33(1) of the ITA 1967. Foreign ESOS holders based in Malaysia should also be aware of their tax obligations under the ITA 1967 and the tax reliefs offered under the Income Tax (Exemption) (No. 5) Order 2022.

Footnotes

1. Paragraph 5.1 of Public Ruling No. 11/2012.

2. Paragraph 5.4 of Public Ruling No. 11/2012.

3. Paragraph 4.15 of Public Ruling No. 11/2012.

4. N/A. "Employee Share Schemes." ACCA Global, March 31, 2015. https://www.accaglobal.com/gb/en/student/exam-support-resources/professional-examsstudy-resources/p6/technical-articles/employee-share-schemes.html.

5. Ibid.

6. Section 4(b) of the ITA 1967.

7. Section 4(c) of the ITA 1967.

8. Paragraph 3.9 of Public Ruling 5/2019.

9. Paragraph 5.3 of Public Ruling 5/2019.

10. Section 32(1A) of the ITA 1967.

11. N/A. "Malaysia — Public Ruling No. 11/2012." Deloitte, January 18, 2013. https://www.deloitte-tax-news.de/arbeitnehmerentsendung-personal/aktuelles-ausland/files/gesnewsflash-malaysia-18012013.pdf.

12. N/A. "Employee Share Schemes." ACCA Global, March 31, 2015. https://www.accaglobal.com/gb/en/student/exam-support-resources/professional-examsstudy-resources/p6/technical-articles/employeeshare-schemes.html.

13. W-01(A)-117-03/2019.

14. [2022] MLJU 3000.

15. Paragraph 6.1 of Public Ruling No. 12/2012.

16. Paragraph 6.2 of Public Ruling No. 12/2012.

17. Paragraph 6.2 of Public Ruling No. 12/2012.

18. Paragraph 5.1.4 of the Inland Revenue Board of Malaysia's Tax Treatment in Relation to Income Received from Abroad (Amendment) LHDN.AG.600-1/7/3.

19. Order 3(2) of the Income Tax (Exemption) (No. 5) Order 2022.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.