Les nouvelles indications des ACVM mettent en évidence l'importance des obligations d'information liées au changement climatique pour les autorités en valeurs mobilières et les investisseurs et elles ont pour objet d'aider les émetteurs à cerner les risques importants posés par le changement climatique et à améliorer l'information qu'ils fournissent à cet égard.

Les Autorités canadiennes en valeurs mobilières (les « ACVM ») ont publié dernièrement l'Avis 51-358 du personnel des ACVM, Information sur les risques liés au changement climatique (l'« Avis »). L'Avis a été motivé par l'intérêt accru de la part des investisseurs, particulièrement les investisseurs institutionnels, à l'égard des risques liés au changement climatique, l'information existante des émetteurs sur le changement climatique qui, selon les ACVM, pourrait être de meilleure qualité, le grand nombre de rapports publiés sur la communication d'information liée au changement climatique et d'autres sujets de gouvernance environnementale au cours des dernières années.

L'Avis ne crée pas de nouvelles obligations légales, mais se veut le prolongement des indications sur la communication d'information continue liée au changement climatique préalablement fournies dans l'Avis 51-333 du personnel des ACVM, Indications en matière d'information environnementale.

Facteurs à prendre en considération par les administrateurs et dirigeants

L'Avis met en évidence les rôles respectifs de la direction et du conseil (y compris son comité d'audit) concernant la planification stratégique, la surveillance des risques, ainsi que l'examen et l'approbation des documents annuels et intermédiaires déposés par l'émetteur en vertu de la réglementation. Dans l'Avis qui se veut uniquement un outil informatif, il est suggéré de façon générale au conseil d'administration et à la direction de l'émetteur d'adopter les pratiques suivantes :

- Veiller à ce que le conseil d'administration et la direction possèdent ou puissent obtenir l'expertise appropriée sur le changement climatique propre au secteur pour comprendre et gérer le risque lié au changement climatique.

- Établir des contrôles et procédures de communication de l'information conçus pour recueillir et communiquer de l'information sur le changement climatique à la direction, afin de permettre l'appréciation de l'importance relative et, le cas échéant, la communication de l'information en temps voulu.

- Se demander si les risques et occasions liés au changement climatique sont intégrés au plan stratégique de l'émetteur.

- Déterminer si les systèmes et la méthode de l'émetteur, y compris ceux qui relèvent de la responsabilité de l'unité d'exploitation, permettent de cerner, communiquer et gérer convenablement les risques liés au changement climatique.

- Éviter les formules vagues ou toutes faites dans la communication de l'information sur les risques liés au changement climatique.

- Passer en revue les questions pertinentes formulées par les ACVM à l'intention du conseil et de la direction afin d'étayer l'évaluation des risques liés au changement climatique.

L'importance relative appliquée au changement climatique

La réglementation des valeurs mobilières canadienne rend obligatoire la communication de l'information importante et établit des principes directeurs d'évaluation de l'importance relative. Il ressort clairement de l'Avis que l'évaluation de l'importance relative appliquée aux risques liés au changement climatique n'est pas différente.

Dans l'Avis, on insiste sur le fait que les risques liés au changement climatique et leurs répercussions financières éventuelles font partie des enjeux courants du monde des affaires. Même si les risques liés au changement climatique peuvent différer des autres risques d'entreprise puisque notre compréhension de ces risques évolue, qu'il peut être difficile de les quantifier et que leurs répercussions éventuelles se font sentir à plus long terme, le conseil et la direction devraient prendre des mesures appropriées afin de les comprendre et d'en apprécier l'importance relative pour leur entreprise.

L'Avis met en évidence certains facteurs précis à prendre en considération pour évaluer l'importance relative des risques liés au changement climatique :

- Moment choisi – L'émetteur ne devrait pas limiter son évaluation de l'importance relative aux risques à court terme. L'incertitude et l'horizon temporel de la réalisation du risque pourraient avoir des répercussions sur l'évaluation de l'importance du risque, mais non sur la nécessité d'en apprécier et d'en analyser l'importance relative.

- Évaluation – Le conseil et la direction devraient évaluer les répercussions financières actuelles et futures des risques importants liés au changement climatique sur les actifs, les passifs, les produits, les charges et les flux de trésorerie à court, à moyen et à long terme. Si possible, les émetteurs doivent quantifier et communiquer les répercussions potentielles, notamment financières des risques liés au changement climatique, y compris leur ampleur et leur horizon temporel.

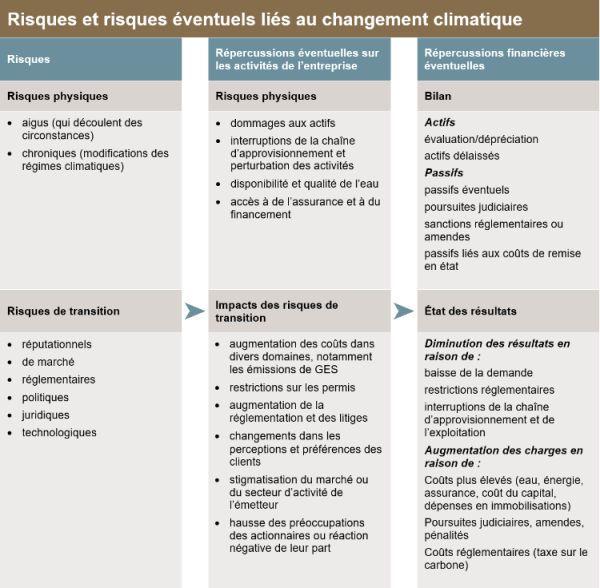

- Catégorisation du risque et répercussions éventuelles – L'Avis donne des pistes de réflexion utiles sur les risques liés au changement climatique et leurs répercussions financières, opérationnelles et commerciales, comme il est illustré dans le tableau ci-après :

Conclusion

Même s'il ne crée pas de nouvelles obligations de communication de l'information, l'Avis, dans la foulée de l'intérêt accru des investisseurs institutionnels et d'autres intéressés pour les risques liés au changement climatique, annonce peut-être d'autres initiatives réglementaires axées sur le changement climatique et les marchés des capitaux. Dans le cadre de leur programme permanent d'examen des documents d'information continue, les ACVM continueront à surveiller les informations présentées sur le changement climatique.

Entretemps, le conseil et la direction devraient continuer à examiner leurs pratiques existantes relativement à la collecte et à la communication de l'information sur le changement climatique et à l'évaluation et la présentation de l'information sur les risques liés au changement climatique. En outre, les émetteurs doivent se demander quelles incidences ces nouvelles indications des ACVM pourraient avoir sur les rubriques des facteurs de risque de leurs rapports de gestion trimestriels et annuels et de leurs notices annuelles à l'avenir.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.