- within Wealth Management topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Business & Consumer Services, Healthcare and Technology industries

Copyright 2009, Blake, Cassels & Graydon LLP

Originally published in Blakes Bulletin on Environmental/CleanTech, June 2009

Canadian businesses need to assess their greenhouse gas emissions and consider options for reducing such emissions in light of the recently released NRTEE report.

On April 16, 2009, the National Round Table on the Environment and the Economy (NRTEE) issued its Achieving 2050 proposal for a Canadian carbon pricing policy, which includes a comprehensive and in-depth assessment of how to most efficiently reduce greenhouse gas (GHG) emissions in Canada. The NRTEE is an organization that was created in 1988 to generate and promote sustainable development solutions to advance Canada's national environmental and economic interests simultaneously, through the development of innovative policy research and advice.

The goals of Achieving 2050 are a carbon pricing policy that meets the Canadian government's medium and long-term GHG emission targets with the least economic cost, and to minimize adverse impacts on regions, sectors, and consumers. NRTEE aims to achieve maximum GHG emission reductions at the lowest cost through the implementation of comprehensive and integrated approach for developing and implementing a Canadian carbon pricing policy.

Achieving 2050 proposes a national carbon pricing policy that would establish a unified carbon price across all emissions, policies, and jurisdictions, and send a credible long-term price signal sufficient to drive new investment and technology development. NRTEE estimates that a unified carbon price across all emissions, policies, and jurisdictions would allow for a steady-state carbon price of C$300 per tonne of carbon dioxide equivalents (CO2e) some time after 2030, rather than a price in excess of C$350/tonne of CO2e that would result from a fragmented policy. Achieving 2050 submits that a credible long-term carbon price signal that generates confidence in the marketplace would result in lower GHG emissions overall, compared to alternatives which involve uncertainty about the future carbon policy and prices.

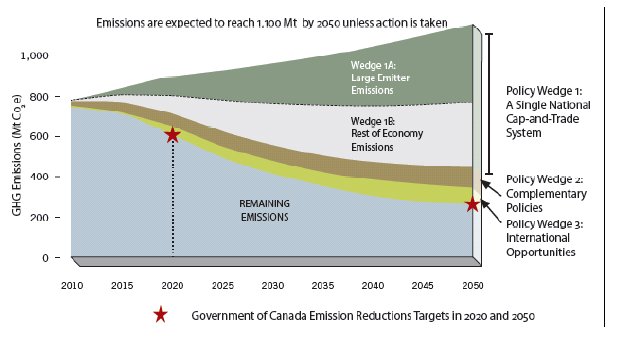

Policy Wedges

The proposed carbon pricing policy involves three main components or "policy wedges", as illustrated in the figure below. The first policy wedge is a single national cap-and-trade system, the second is complementary regulations and technology policies, and the third is international opportunities. The first policy wedge, which accounts for the majority of the GHG emissions, is targeted both at "large emitters" emissions (wedge 1A), and "rest of economy" emissions (wedge 1B) from buildings, households, transportation, and light manufacturing.

The cap-and-trade system underpinning the first policy wedge is a system whereby the government sells a fixed number of permits to people who emit GHGs. The number of permits owned determines the amount of GHGs that may be emitted by a person, in excess of which such person will have to purchase offset credits under the system. As discussed in the first part of this bulletin, unregulated businesses and other organizations which reduce their GHG emissions may obtain offset credits which they can sell to businesses that wish to exceed their permitted GHG emission levels as determined by their permits allocated from the government. Since there are a fixed number of permits in the marketplace, the amount of GHGs that will be emitted is also fixed or "capped". And since permits can be purchased/sold by entities that emit more/less GHGs than their permitted allowance, the system is characterized as a "cap-and-trade".

For more detailed discussions of what the trading of permits might entail, see the Blakes Bulletins entitled The Role of Emissions Offset Trading in North American Greenhouse Gas (GHG) Emissions Regimes and Making Sense of Carbon Transactions: The Nuts and Bolts of an Emissions Trade.

The main disadvantage of a cap-and-trade system is that there is uncertainty with respect to the market price of permits. If GHG emissions are much greater than what is permitted based on the number of permits available, then the price of each permit will be high, because the demand for such permits will exceed their supply. The main alternative to a cap-and-trade system, and the way to achieve price certainty, is a pure carbon tax, whereby the government sets a tax on all GHG emissions. However, while a pure carbon tax may provide certainty for the cost of GHG emissions, it does not provide certainty for the quantity of GHG reductions.

In addition to the cap-and-trade system, the proposed carbon pricing policy includes a policy wedge of complementary regulations and policies to expand the policy coverage and address technology barriers. Specific regulations can broaden the coverage of the carbon pricing policy by targeting emissions in certain sectors that do not respond efficiently to a carbon price signal alone, such as in the transportation, buildings, oil and gas, and agriculture sectors. Technology barriers can be addressed with policies that support technology innovation, adoption, and deployment. Some of the technologies that are likely to help Canada reach its GHG emission reduction targets include increased energy efficiency, carbon capture and storage (CCS), and fuel switching to electricity and renewables.

The final policy wedge in the proposed carbon pricing policy involves low-cost international carbon abatement opportunities. Such opportunities allow for purchases of real and verifiable international carbon permits through links between the Canadian trading system and other systems. The result of this third policy wedge, if applied to 30% of Canada's targeted reductions by 2050, is that the steady-state carbon price could be reduced from C$300/tonne of CO2e to below C$200/tonne of CO2e. However, if Canadian entities are purchasing permits abroad, then the amount of GHGs actually emitted from Canada will still be greater than Canada's targets, because the fixed number of permits initially sold by the Canadian government will be supplemented by other permits obtained elsewhere. Furthermore, it is not yet clear how Canada will integrate its cap-and-trade system with its key trading partners such as the United States.

A governance framework is proposed to develop, implement, and manage the unified carbon pricing regime over time. This governance framework calls for ongoing collaboration between federal, provincial, and territorial governments, an expert Carbon Pricing and Revenue Authority with a regulatory mandate, and an independent, expert advisory body to provide regular and timely advice to government.

Comparisons and Challenges

Achieving 2050 is based on abatement goals set by the federal government, which appear increasingly out of step with the global scientific consensus around the need for greater reductions. The federal government has targeted a 20% reduction in GHG emissions by 2020 and a 65% reduction by 2050, relative to 2006 levels. Canada's equivalent targets relative to 1990 levels are a 3% reduction by 2020 and a 58% reduction by 2050. Canada's abatement goals are significantly less ambitious than those of the European Union, the United Kingdom, or the United States (based on President Obama's election proposal), all of which are targeting up to an 80% reduction in GHG emissions by 2050, relative to 1990 levels. (For a more detailed discussion of proposed GHG legislation in the United States, see the Blakes Bulletin entitled A Bold Step Forward: What the Draft U.S. Clean Energy and Security Act of 2009 Means for Canadian Industry.) Achieving 2050 is based upon Canada's current targets and would need to be recalibrated in the event that these targets were to change.

According to Environment Canada, Canada's GHG emissions have increased steadily from 592 Megatonnes (Mt) of CO2e in 1990 to 747 Mt CO2e in 2007. Kyoto called for the reduction of GHG emissions to below 1990 levels by 2012, which for Canada meant a reduction in GHG emissions to 556 Mt CO2e. However, Canada's 2007 GHG emissions were 34% above the Kyoto target. Even with the federal government's current plan of reducing GHG emissions to 577 Mt CO2e by 2020, Canada would still be above its Kyoto commitment for 2012.

Canada's GHG emissions levels are already higher than most countries, particularly on a per capita basis. According to The Conference Board of Canada, the average Canadian emitted 22.6 tonnes of CO2e in 2005, compared to 21.7 tonnes of CO2e emitted by the average American, 10.9 tonnes of CO2e emitted by the average Briton, and 8.1 tonnes of CO2e emitted by the average French or Italian. This higher level of per capita GHG emissions, combined with Canada's less ambitious targets for reducing GHG emissions, suggests that Canadians may continue to be among the world's greatest producers of GHGs and contributors to global warming.

While Achieving 2050 proposes a carbon pricing policy that would help to reduce Canada's GHG emissions, it is not as effective as proposals and legislation in other countries. For example, the United Kingdom's Low Carbon Industrial Strategy, including its "Budget 2009", has established concrete measures to achieve significant reductions in GHG emissions, with more than £60-billion (or C$100-billion) of low-carbon investment from now until 2011. As of April 1, 2009, the United Kingdom gas tax was increased to £0.5419/litre (or C$0.96/litre), which is more than the current price of gas in Toronto. Since 2.4 kg of CO2 is produced for every litre of gasoline used, a gas tax of C$0.96/litre is equivalent to an additional cost of C$400/tonne of CO2. The Canadian government should not only consider implementing the recommendations in Achieving 2050, but it should also consider realigning its initial targets and objectives with international best-practices.

It also remains to be seen if a unified and national system, as proposed in Achieving 2050, will replace the provincial and regional systems that are either emerging or currently in place:

- For Ontario, see the Green Energy Act, discussed in the Blakes Bulletin entitled Ontario's New Green Energy Act Set to Energize the Province with Renewable Energy;

- For Alberta, see the Specified Gas Emitters Regulation, discussed in the Blakes Bulletin entitled Calibrating Your Climate Change GPS – How to Navigate Alberta's New Emissions Reduction Regime;

- For British Columbia, see the Mandatory Reporting of Greenhouse Gas Emissions Regulation, discussed in the Blakes Bulletin entitled A New Era of Reporting Obligations: British Columbia Proposes Mandatory Reporting of Greenhouse Gas Emissions for 2009, and 11 other pieces of provincial legislation introduced last spring, discussed in the Blakes Bulletin entitled British Columbia Makes Major Changes to Environmental and Energy Law; and

- For the Western Climate Initiative (WCI), see the Blakes Bulletin entitled Designing the Western Carbon Frontier: WCI Announces Proposed Framework for Regional Cap-and-Trade Program.

As these various policy and legislative initiatives move forward, Canadian businesses will need to assess their GHG emissions and consider options for reducing such emissions in order to comply with current and proposed legislation. It is becoming increasingly clear that there will inevitably be a cost to emit GHGs, and the cost may be expected to increase substantially over time. As the cost of GHG emissions increase, the value of GHG emissions permits and offset credits will become an increasingly important economic factor for Canadian businesses.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.