The new tax policies introduced by the Canadian Federal Government on July 18, 2017 (we'll refer to these policies as the "Fair Tax Plan")1 appear likely to materially harm the Canadian economy including, as will be discussed below, by exposing Canadian small business owners to tax rates of 93% or even more.2

The Fair Tax Plan

In Finance Minister Bill Morneau's letter to all Canadians introducing the Fair Tax Plan he states:

"And it starts by making sure that we all pay our fair share of taxes – with no exceptions."

We don't think that exposing Canadian small business owners to tax rates of 93% or more is fair, and we trust that Canadians would agree.

The measures in the Fair Tax Plan do not just impact the "1%". In fact, the Fair Tax Plan undermines all Canadian small business owners, which, according to the Federal Government's own statistics, comprised over 97% of Canadian businesses in 2015 and include restaurant owners, franchisees, real estate agents, plumbing contractors and a broad range of other small businesses.3

The mere proposal of these changes has already thrown the Canadian private business owner tax system into turmoil, and, unfortunately, the Government and the Department of Finance do not seem to appreciate and possibly do not understand the extent of the damage that the Fair Tax Plan will cause to Canadian business owners, employees of their businesses, and the economy as a whole.

Combined with rising labour costs,4 among other things, the interaction of the changes in the Fair Tax Plan (some of which took effect as of July 18, 2017) will (a) undermine retirement and succession planning in ways that are often retroactive, punitive and could result in an effective confiscation of a small business owner's property; (b) burden estates with double or more levels of taxation; (c) negatively distort the market for private business owners seeking to sell their businesses, including in ways that may effectively take away their capital gains exemptions; and (d) create a new crushing compliance burden for any person or entity carrying on anything but a public or foreign business. The result is that many businesses will likely close and take with them the jobs they had created for the people whom the Liberal Government is trying to help.

There are some policy measures in the Fair Tax Plan that are fair and difficult to argue against, such as curbing planning that can allow the capital gains exemption to be enjoyed by taxpayers in ways far beyond the intent of the legislation. However, there are better ways to address such issues than through the wide net of the Fair Tax Plan.

Some may suspect that we are exaggerating the impact of the Fair Tax Plan. To them, we would ask if a tax system that can confiscate the hard-earned income of a business owner at a tax rate of over 93% is fair? This could be the result if the Fair Tax Plan is implemented.

For more detail as to how the 93% tax rate has been calculated, we encourage you to review the example in Annex I to this article. We also invite you to read through the discussion that suggests that the Fair Tax Plan may jeopardize the ability for private business owners to sell their shares and use their capital gains exemption found in Annex II to this article.

Conclusions

The individual proposals in the Fair Tax Plan are extremely complicated and their complexity increases as the interactions between the proposals and the rest of the Income Tax Act,5 are considered. The Department of Finance has invited Canadians to provide comments and allowed only 75 days to do so. Given that these proposals collectively are perhaps the most transformational changes in over 50 years, this amount of time to respond is wholly inadequate.

Regardless of the time provided for comments, as illustrated in the examples in the Annexes to this article, we believe that there is no way to work with the Fair Tax Plan and that it should simply be abandoned before any of it is enacted into law.6

Even though our proposal is to abandon the Fair Tax Plan, there are elements of the Canadian income tax system that do need to be improved and made more fair for all Canadian taxpayers. Hopefully, the Government will restart the process of making those changes by first better-defining its legitimate tax objectives and then spending time to properly consult with the tax community and affected constituents. We believe that it is possible to build a legislative plan that will be fair to all Canadians and will ensure the ongoing success of our economy.

With what we know today of the Fair Tax Plan, it seems very likely that it will materially harm the Canadian economy. We can only imagine what other tax implications will be discovered once the greater tax community has had the time to fully review and understand the interaction of the proposed changes being made by the Fair Tax Plan with the rest of the Act. Provided the Fair Tax Plan is abandoned, we hope to never find out.

Annex I - The Fair Tax Plan – An Example7

Stage 1 – Building Value

Imagine a situation involving Marie, the owner of an incorporated small business that provides landscaping services ("Gardenco"), who took legitimate steps to allow her only child, Justice, who is not active in the business carried on by Gardenco to acquire nominal value common shares of Gardenco.8 Now let's fast forward 10 years. Over that time, Justice's shares of Gardenco have become valuable, because Marie successfully ran the business (and employed her friends and neighbours).

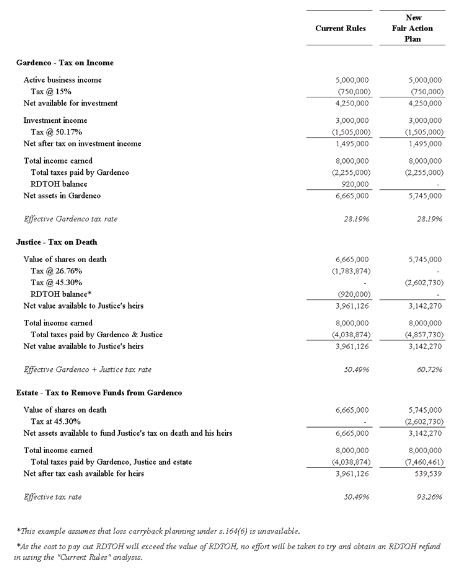

Let's say that during the 10-year period, Gardenco earned taxable profits totaling $5,000,000 ($500,000 per year). As the profits qualified for the combined federal and Ontario 15.00% small business rate (provided to create an incentive to entrepreneurs to create businesses and jobs), Gardenco paid tax of $750,000.9

Gardenco paid Marie a reasonable salary over those 10 years (Marie paid tax at top Ontario tax rates of 55.48%, including Ontario employer health taxes). Gardenco was also able to retain after-tax profits of $4,250,000 for reinvestment. Over the 10-year period, those investments generated $3,000,000 of income and Gardenco paid $1,505,000 in taxes on this income.

A portion of Gardenco's investment taxes ($920,000) are eligible to be refunded, provided sufficient dividends are later paid by Gardenco.10 However, because it is assumed that the recipients of such dividends will be taxed at the highest tax rates and will pay more than $920,000 in personal taxes in connection with such dividends, it has been decided to defer the corporate refund as the funds are being continuously invested.

As a result of its success, the value of Gardenco has increased by $6,665,000 (this value includes the $920,000 refundable tax asset in Gardenco) over the 10-year period,11 which has also increased the value of Justice's shares to $6,665,000. In addition, Gardenco has paid $2,255,00012 in income taxes on $8,000,000 of net taxable income for an effective corporate tax rate of about 28.19%.

So far it's looking pretty good for Marie and her family – but it should be kept in mind that before Gardenco became a success, Gardenco could not afford to pay Marie. Therefore, she drew out her RRSP savings, she mortgaged her house, and she even drew on her spouse's assets. Marie had no pension fund or savings to provide her with a safety net. Her efforts also enabled Gardenco to employ multiple employees. Regardless of Marie's personal situation, the salaries and source deductions of Gardenco's employees were paid, as were numerous other business fees and taxes.

Stage 2 – Death – Pre-Fair Tax Plan

As part of succession planning, we always have to assume someone will die (as we all will) to determine the tax consequences that will occur on death. For the purpose of this example, we will assume that Justice is no longer alive.

Subject to limited exceptions, under Canadian tax law, the death of a taxpayer causes a deemed disposition of the taxpayer's assets at fair market value, giving rise to income tax on the previously unrealized capital gains.13 In this case, in the absence of changes and proposed changes under the Fair Tax Plan, the deemed capital gains on Justice's nearly $6,665,000 of Gardenco shares would typically be expected to give rise to taxes of nearly $1,784,000 and to increase the cost base in Justice's shares of $6,665,000.14

If this were the end of the story - and under the pre-Fair Tax Plan system, it might be15 – the total income taxes paid by Justice and Gardenco on the $8,000,000 of net taxable income would have been almost $4,039,00016 for an effective combined corporate and personal income tax rate of 50.49%. While this tax rate is approximately what the average top-tax-rate employee would pay, the ability to defer almost $1,784,000 of this tax until Justice's death is a tax advantage enjoyed by Marie and her family when compared to an employee – but, again we mustn't forget that Gardenco has paid a host of other business taxes, created jobs for Canadians and that Marie and her family have faced more than their fair share of risk and adversity to build a successful small business.

Stage 2.1 Death under the Fair Tax Plan

Now let's add in the impact of the Fair Tax Plan. Instead of the just under $1,784,000 of tax payable on Justice's death, the taxes will increase to more than $2,602,500,17 increasing the total taxes payable by Gardenco and Justice on that $8,000,000 of net taxable income to just over $4,857,50018 – or an effective tax rate of nearly 60.72%.

It's beginning to look pretty bad for Marie and her family and we wish this was the end of the story, but it's not. To pay for this additional nearly $2,602,500 of income tax, the executors of Justice's estate will need to come up with money. However, the money is still in Gardenco and the Fair Tax Plan may have eliminated the ability for Justice's executors to remove the money from Gardenco without additional tax becoming payable.19

If the executors can sell the shares to an arm's length party, they could come up with the money. But that means the end of the next generation's involvement in the business – not a great policy result. We'll say a few words about the distortion of the sale market for private company shares below in Annex II to this article.

You may be asking yourself how the executors can get the cash to pay this approximately $2,602,500 additional tax liability. The answer is that they will need to cause Gardenco to pay taxable dividends on the shares to the estate. Assuming that the $5,745,000 of cash in Gardenco is distributed by way of taxable dividends to the estate, the estate will be liable for over $2,602,500 of additional taxes.20

In the pre-Fair Tax Plan discussion, we mentioned that Gardenco would have a refundable tax asset of just over $920,000. However, the Fair Tax Plan proposes to eliminate this tax refund for private corporations that use their active business income profits to earn income from passive investments. As a result, this refund will not be available to Gardenco.21

What is the total tax bill for Gardenco, Justice, and the estate as proposed? You may recall that Gardenco paid a total of $2,255,000 in income taxes on the $8,000,000 of net taxable income it earned. On Justice's death, further taxes of more than $2,602,500 will be payable and, to access the money in Gardenco, Justice's estate will also be required to pay more than $2,602,500 in taxes. Based on these calculations, the total tax payable by Gardenco, Justice and his estate to earn $8,000,000 of taxable income in Gardenco is a staggering amount of just over $7,460,000 – or 93.26% of the income earned by Gardenco!

One would have to wonder why Marie even bothered to go into business at all. Quite frankly, given the risks she and her family have taken and the sacrifices they have made, her family would likely have been better off if she'd gone to work for someone else. Unfortunately, her community, her province and Canada as a whole would be far worse off in almost every way imaginable (fewer jobs; fewer source deductions, business fees and taxes; spin-off benefits, etc.).

Annex I.1 - The Fair Tax Plan – An Example

Annex II – Distortion of the Sale Market for Shares

Even if a sale can be completed, will it be possible to find a purchaser who is willing to buy shares?

Unfortunately, other changes introduced in the Fair Tax Plan may result in buyers avoiding the purchase of shares.22 This is because if buyers use their after-tax dollars to buy shares, they might not be able to extract the purchase price from Gardenco without tax.

Assume that Wylie, an individual who deals at arm's length with Justice, is considering buying Justice's estate's shares of Gardenco for $5,745,000. It would appear that if Wylie purchased the Gardenco shares with his own after-tax dollars, he may need to pay taxes of over $2,602,500 to be able to extract the money back from Gardenco.23 Therefore, Wylie would instead offer to purchase Gardenco's assets for $5,745,000,24 unless the estate offered to sell its shares with a substantial discount.25

An unintended consequence of the Fair Tax Plan is that individual shareholders may have difficulty claiming their capital exemptions. Purchasers, such as Wylie, will be further incentivized to purchase assets, in lieu of shares, since they may no longer be able to monetize the cost base of purchased shares. Furthermore, even if the seller offered a price reduction on the shares in order to claim the capital gains exemption, the discount required to compensate the potential inability to monetize the cost base of a purchaser, such as Wylie, will outweigh the savings from utilizing the capital gains exemption.

Footnotes

1 The "Related Products" section using the Department of Finance link http://www.fin.gc.ca/n17/17-066-eng.asp includes the "Fair Tax Plan" documents referred to in this article.

2 Although not dealt with in this article, Mac Killoran has run other examples that show the total tax payable can actually exceed 100% of the taxable income earned in certain situations.

3 For more on this statistic please click the link https://www.ic.gc.ca/eic/site/061.nsf/vwapj/KSBS-PSRPE_June-Juin_2016_eng.pdf/$FILE/KSBS-PSRPE_June-Juin_2016_eng.pdf.

4 Minimum wage rates are rising in many jurisdictions across Canada and are set to rise dramatically in Ontario where the provincial government has controversially announced hikes in the minimum wage from to $11.40 to $14.00 on January 1, 2017 and to $15.00 an hour (indexed for inflation) on January 1, 2019.

5 Unless otherwise noted in this article and the Annexes, all statutory references are to the Income Tax Act (Canada) R.S.C. 1985, as amended ("Act").

6 There is past Canadian precedent for our Federal Government abandoning a major tax overhaul: in 1981, then Liberal Finance Minister Alan MacEachen introduced an "ambitious" overhaul of the Canadian income tax system, which was ultimately abandoned. Interestingly, the Prime Minister at that time was Pierre Elliot Trudeau.

7 See Annex I.1 for a breakdown of all of the numbers in this example.

8 These steps are sometimes referred to as an estate freeze.

9 All tax rates utilized in this article are based on combined Federal and Ontario tax rates. It is assumed that top combined Federal and Ontario marginal tax rates apply to all personal income tax amounts.

10 The refundable tax regime in the Act is intended to ensure tax fairness so that investment income earned in a corporation is taxed at approximately the same rate that it would be if it were earned directly by an individual.

11 The increase is due to $1,495,000 of after-tax investment profits plus $4,225,000 of after-tax operating profits plus just over $920,000 of refundable taxes.

12 An aggregate of $750,000 of active small business corporation taxes and $1,505,000 of corporate investment taxes.

13 See subsection 70(5).

14 As the Gardenco shares will not qualify for the lifetime capital gains exemption under the Fair Tax Plan or under the pre-Fair Tax Plan regimes, we have assumed that the full amount of the increase in value will be treated as a capital gain and that the full gain would be taxable at capital gains tax rates of 26.76%.

Whenever possible certain post-mortem planning under subsection 164(6) should be considered as it could be tax advantageous in specific circumstances. However, this planning exception is only available to special types of estates that qualify as "graduated rate estates", GRE for short, and can only be implemented during the first taxation year of the estate (which is far too short a time period for estates of any complexity). Since not all estates will be able to qualify for this tax reduction, these potential tax savings will be ignored in this example.

15 Using a technique that is often referred to as "pipeline planning," it might be possible for Justice's estate and/or heirs to use the cost base in the shares Justice owned, to remove up to $6,665,000 of cash from the corporation without additional tax being paid. Other approaches could be used and different tax results would arise. Such other approaches are ignored in this article.

Steps to refund the $920,000 of refundable tax should also be considered as there may be tax advantages to doing so. Such planning and any attempt to value such tax advantages is beyond the scope of this article.

16 An aggregate of $2,255,000 of corporate taxes and nearly $1,784,000 of personal taxes.

17 Changes to the rules relating to sprinkling of income using private corporations will cause the deemed gain to be taxed as if it was a dividend (see draft section 120.4 changes and, in particular, changes to section 120.4(4)), which for purposes of this example will be taxed to Justice at a tax rate of 45.30%. We have assumed that the changes to the taxation of holding private investments inside a private corporation have also been implemented such that there is no refundable tax in Gardenco. As a result, the value of Gardenco for purposes of determining Justice's dividend tax liability will only be $5,745,000 and not $6,665,000 under the prior regime.

If Justice had inherited the Gardenco shares from Marie certain exceptions to these rules might apply so that tax of nearly $1,784,000 would have been payable (draft clause 120.4(1.1)(e)(ii)(C)). However, this tax would have been payable at the time of Marie's death.

18 An aggregate of $2,255,000 of corporate taxes and over $2,602,500 of personal taxes.

19 Changes to the rules converting a private corporation's regular income into capital gains (see proposed changes to section 84.1 and new section 246.1) may have eliminated pipeline planning effective July 18, 2017. These changes will have far ranging consequences on many taxpayers – many of them retroactively exposing taxpayers to double or triple taxation.

20 We have assumed that the dividend tax rate would be 45.30%. It would appear that if certain post-mortem planning under subsection 164(6) is employed that it could be possible to effectively reduce the deemed dividend tax under subsection 120.4(4) from about $2,602,500 to a bit more than $1,060,000 (the amount of the reduction could be more depending on the sources of other income earned by Justice in his terminal taxation year). However, for reasons noted when discussing the pre-Fair Tax Plan regime, it is assumed that subsection 164(6) planning is unavailable in this situation.

21 Changes to the rules regarding holding a passive investment portfolio inside a private corporation. A consequence of this change will be to tax such income when it is distributed from certain private corporations at a 72.74%effective tax rate.

22 Changes to the rules converting a private corporation's regular income into capital gains (see proposed changes to section 84.1 and new section 246.1).

23 Due to the application of section 246.1, Wylie would appear to be unable to use pipeline planning to remove funds from Gardenco without giving rise to deemed dividends. Arguments might be made that this result could be avoided through careful planning if Wylie were to buy the shares through a corporation owned by him. However, there appears to be no certainty that such planning will be successful since in applying the rules in section 246.1, Finance's comparative norm to determine if the rules are engaged is that tax should be paid as a dividend. We have applied a dividend tax rate of 45.30% to calculate this tax liability.

24 A sale of assets won't help Justice's estate to fund its tax liability as the money will still be in Gardenco. Also, depending on the assets in Gardenco, a sale of the assets could give rise to a further level of taxation – that is a further subject that we will ignore for purposes of this article.

25 In general, purchasers prefer to buy assets to avoid a number of legal and tax complications when shares are purchased and will request a discount off the price that would otherwise be offered to purchase assets when acquiring shares. The additional tax issues raised by draft section 246.1 appears likely to severely increase the discount that purchasers will request.

The rules in section 246.1 appear to have been written broadly enough to apply to any type of purchaser. However, by virtue of the purpose test in paragraph 246.1(2)(d), it appears to be more likely that section 246.1 will apply to smaller more unsophisticated purchasers, like Wylie, than to larger and more sophisticated purchasers, such as a public company. While it may still be too early to definitively conclude on this point, it would appear that the rules in section 246.1 could place such smaller unsophisticated purchasers at a disproportionate disadvantage in their ability to compete on an even playing field with some larger purchasers.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.