Governments have long been trying to connect performance with budgeting. Along the way we have seen everything from a focus on publicly available annual plans and reports to the use of performance measures in budget documents and the carrying out of sweeping reviews of operations, services and programs. At the heart of all this is the desire for information about how government works and about its successes, along with its failings, to then make decisions about funding, staff and other resources. But how to make this happen?

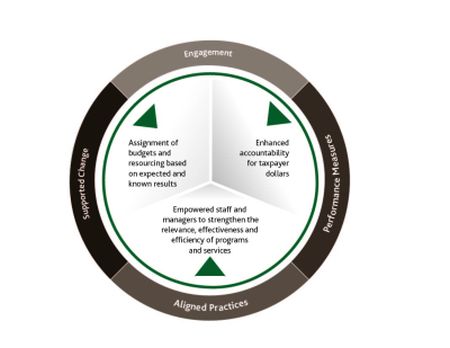

Legislation or a clear mandate is surely a starting point. In our experience, though, the answer to successful performance-based budgeting goes beyond this, encompassing engagement, performance measures, aligned improvement practices and supported change, as shown in the model below.

Engagement

Engagement includes communicating on a regular basis with managers and staff to address the always-present concerns that "it's only about cost cutting." It is vital to communicate and re-communicate that the broader objective of linking performance with budgeting is to assign budgets and resources based on planned as well as known results that are seen as priorities.

Engagement is also about facilitating collaboration between divisions, departments and agencies in the pursuit of shared goals. It is important to understand the audiences for the performance information being generated and to ensure that what is provided is straightforward and usable for making budgetary decisions.

Performance Measures

Another part of the answer is found in the use of performance measures. There must be a practice of identifying current and potential measures of performance and related reporting requirements, with the objective of answering the questions, "Do these tell the story of both progress and results?"; "Can the information be sourced and relied upon?" and "What is required to sustain the use of these measures?"

Alignment of Improvement Practices

A third part of the answer is alignment of performance-improvement practices, be they Lean processes, enterprise risk management, audits or consultations, in order to find synergies in answering critical questions like "Are needs and commitments changing?"; "In what ways are the desired results being realized?"; "How are the issues that influence success being managed?" and "Are we making the best use of financial, human and other resources?"

Supported Change

The fourth part of the answer is found in supported change, namely through the implementation of the recommendations that result from program and service reviews for their current and future relevance, effectiveness and efficiency. This depends, in turn, on the willingness to put necessary supports in place to achieve intended improvements.

With these four elements in place, and in a way that fits with the key decision points in government, the benefits of tying performance to budgeting can be realized.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]