- with Finance and Tax Executives

- with readers working within the Accounting & Consultancy industries

In difficult economic times, businesses need to make the best use possible of their resources. This includes any tax attributes available to them to offset taxable income or gains they may have. This BLG Bulletin discusses some of the planning opportunities that a Canadian corporation may have for using tax losses of a related Canadian corporation. Such planning is especially important in Canada, because the Income Tax Act (Canada) (ITA) does not contain rules for group relief that simply consolidate one corporation's losses against income of a related corporation.

TYPES OF LOSSES

Canadian tax law distinguishes between capital losses and non-capital losses. Non-capital losses arise from operating a business or an investment property (i.e., the tax version of an operating loss). A non-capital loss represents the excess of allowable expenses over revenues for the year, as calculated under the ITA. Generally, the non-capital loss for a year can be applied against any income from other sources (including capital gains) realized by the taxpayer in the same year, the three preceding taxation years or the 20 following taxation years.

A capital loss arises from a disposition of capital property, when the taxpayer's cost of the property plus any sale expenses exceed the sale proceeds. A capital loss realized in a year may be deducted against any capital gains realized in that year, the three preceding taxation years or any later taxation year. Capital losses may only be deducted against capital gains.1

Accrued losses on a capital property are generally realized only where there has been a disposition of the property (i.e., a sale or other transfer). As a general rule, the ITA denies or suspends recognition of capital losses on transfers of property between related parties, or where the taxpayer (or a related party) acquires an identical property within 30 days before or after the time the loss property is disposed of. The principle is that losses should only be recognized for tax purposes where there is a disposition of the relevant property outside of the corporate group. Loss denial rules also apply to certain specific property, such as shares on which the taxpayer has received certain tax-advantaged dividends or loans not made for the purpose of earning income.

INTRA-GROUP LOSS PLANNING

In general terms, the Canada Revenue Agency (CRA) considers tax planning to use losses between related parties to be acceptable, while planning to allow one taxpayer to use the losses of an unrelated taxpayer is viewed as contrary to the scheme of the ITA and impermissible. This reasoning is based on the existence of various rules in the ITA that allow losses to be used in some circumstances and not others, and on the restrictions on losses that apply to a corporation that undergoes an acquisition of control.2

This means that there are significant opportunities for two or more related Canadian corporations3 to maximize the use of losses within the group. In 2010 the federal government announced its intention to study the idea of introducing a loss transfer system or consolidated filing procedure for corporate groups (such as exists in the U.S. and many other countries), whereby entities within a related group can simply use one another's losses without having to take any steps to actually shift income or gains from one corporation to another.4 However, historically such proposals have gone nowhere (a previous initiative in the 1980s died) and it is uncertain at best if this attempt will be any different.

There are various ways in which Canadian corporations within a related group can optimize the use of the group's available tax attributes such as losses. While such planning is not per se offensive to the CRA, there are certain aspects of particular strategies that the CRA does object to, and a number of technical tax issues must also be considered to ensure that the desired results are obtained without tripping up. It is useful to review the most common techniques for enabling a Canadian corporation with income or gains (Profitco) to access the accumulated losses of a related Canadian corporation (Lossco), and to understand the limitations and technical issues associated with these strategies.

WIND-UPS AND AMALGAMATIONS

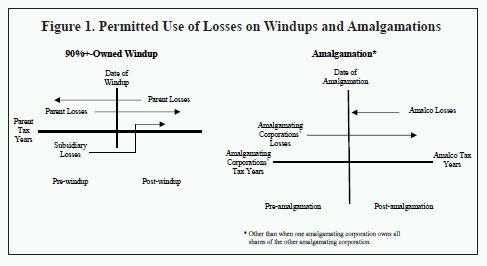

In some cases the desired results can be achieved by winding up Lossco into Profitco or amalgamating Lossco and Profitco. The loss utilization rules applicable to qualifying wind-ups and amalgamations are depicted in Figure 1.

Normally where a Canadian corporation is wound up, its losses cease to exist. An exception is where one Canadian corporation owns all of the shares of the Canadian corporation that is winding up. In those circumstances, the parent corporation can use the subsidiary's capital and non-capital loss balances going forward, but cannot carry the subsidiary's loss balances back to any pre-wind-up parent taxation year. The parent can of course carry any of its own losses forward or back against its own taxable income, subject to the usual three-year carryback limit. A wind-up of Lossco into Profitco allows Profitco to use Lossco's accumulated losses on a go-forward basis against Profitco's future income or gains.

Canadian corporations can also be amalgamated on a tax-deferred basis, and where they are related, no acquisition of control (and associated loss use restrictions) should occur. The new corporation resulting from the amalgamation (Amalco) can use the loss balances of its predecessors (Profitco and Lossco) going forward, but losses incurred by Amalco cannot be carried back and used in pre-amalgamation periods of its predecessors. The only exception is where one amalgamating corporation owns all the shares of the other: in those circumstances Amalco can carry post-amalgamation losses back against pre-amalgamation income of the parent corporation (but not the subsidiary) subject to the usual three-year carryback limit, i.e., the same result as a wind-up above. An amalgamation of Lossco and Profitco is another way of allowing Lossco's accumulated losses to shelter Amalco's post-amalgamation income from Profitco's assets.

BUSINESS TRANSFERS TO/INVOLVING LOSSCO

In some cases merging entities or winding them up is undesirable. There are other ways of allowing Lossco's losses to be used against Profitco's income or gains. For example, Profitco can sell a business or income-producing asset to Lossco, such that the income generated by the business or asset is absorbed by Lossco's accumulated losses. Lossco may pay for the business or asset by issuing shares of itself to Profitco (if the transfer needs to be tax-deferred so that Profitco realizes no gain or income) or with non-interest bearing debt (such that Profitco is not being taxed on interest income).

Where there are concerns about exposing Profitco's assets to Lossco's liabilities, Profitco and Lossco may form a partnership. Profitco transfers the business to the partnership on a tax-deferred basis in exchange for an interest in the partnership, and Lossco transfers other valuable consideration (e.g., existing assets, dividends received from a subsidiary, or property received from its shareholder on a share subscription) into the partnership in exchange for a partnership interest. This structure allows a portion of the partnership's income to be allocated to Lossco commensurate to the value of Lossco's contribution to the partnership. While having Lossco realize only part of the business' income is less tax-efficient than having Lossco realize all of such income, in appropriate circumstances this may still be a useful form of planning.

ROUTING GAINS THROUGH LOSSCO

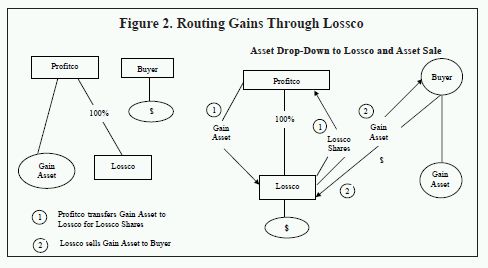

To the extent that Profitco is proposing to sell assets outside the corporate group in a transaction that will produce capital gains or recaptured depreciation for tax purposes, it is usually possible to structure the sale so that the assets are transferred first to Lossco in exchange for Lossco shares on a tax-deferred basis (see Figure 2). The gain assets are then sold by Lossco to the arm's-length third party. This results in the gains or income being realized within Lossco, where they can be sheltered by its losses. The sale proceeds are then typically distributed to Profitco as a dividend, or retained in Lossco and used to generate further taxable income that can be sheltered with losses.

LOSSCO ASSET SALE

To the extent that Lossco has valuable assets that are not generating significant taxable income (e.g., shares of a subsidiary), these can be sold to Profitco in exchange for interest-bearing debt. So long as Profitco is acquiring the property for the purpose of gaining or producing income (which may not necessarily be immediate income) and the rate of interest is commercially reasonable, interest on the debt should be deductible to Profitco, and Lossco can absorb the interest income with its losses.

INTER-COMPANY CHARGES

There may be opportunities in some cases for Lossco to provide services or property to other members within the corporate group. For example, Lossco may have (or can acquire) property that could be leased or licensed to other members of the corporate group for bona fide use in their businesses (e.g., real estate or IP), or the necessary personnel can be hired by Lossco to provide management, finance or other services to group members. Commercially reasonable fees for services or property should be deductible expenses for the other group members, and Lossco's losses offset the fee income.

LOSSCO DEBT REFINANCING

Where Lossco has external interest-bearing debt, Profitco can borrow money from a bank and subscribe for common shares of Lossco. Lossco in turn uses the subscription funds to repay its external debt. If there is a reasonable (but not necessarily immediate) prospect of Profitco earning dividends from its new Lossco shares, interest on Profitco's new debt should be deductible to it, and the refinancing effectively shifts Lossco's interest expense deductions to Profitco.

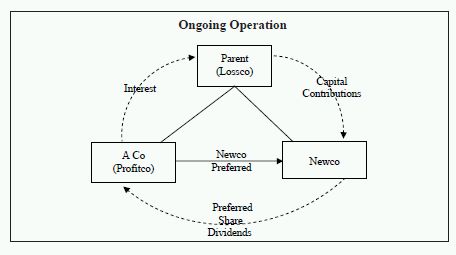

INTEREST EXPENSE/DIVIDEND LOSS CONSOLIDATIONS

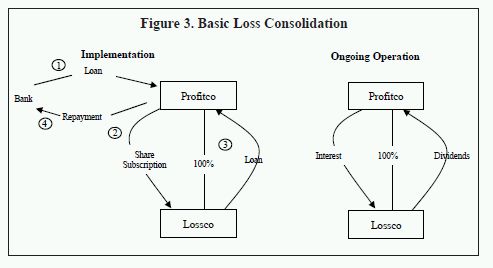

A somewhat more complex form of loss consolidation planning involves generating interest expense deductions in Profitco via a circular intra-group subscription for shares of Lossco. This form of planning does not transfer property out of Profitco, but rather leaves the existing income there and creates deductions within Profitco. The key elements of such planning are that generally (1) dividends received by one Canadian corporation from another Canadian corporation are 100% deductible in computing taxable income (i.e., are received tax-free), and (2) interest on debt incurred to purchase shares of a corporation is tax-deductible so long as there is a reasonable prospect of earning dividend income.

In its simplest form (where Profitco owns all the shares of Lossco), this type of loss consolidation is achieved as follows (see Figure 3):

- Using funds borrowed from a bank under a "daylight loan" (i.e., repaid that day), Profitco subscribes for preferred shares of Lossco that pay dividends at a fixed annual rate;

- Lossco uses the funds received to make an interest-bearing loan back to Profitco, at a rate of interest that is slightly less than the dividend rate on the Lossco preferred shares, such that Profitco is earning a positive spread on its preferred share investment; and

- Profitco uses the loan proceeds to repay the daylight loan.

The result is that Profitco has incurred debt to acquire shares; the debt satisfies the interest-deductibility test of having been incurred for the purpose of producing income, since Profitco earns dividend income on its investment even net of interest expense. Preferred share dividends are received by Profitco on a tax-free basis due to the inter-corporate dividend deduction in subsection 112(1) ITA. Lossco earns interest income, which is absorbed by its losses. Effectively, a portion of Lossco's losses have been shifted to Profitco.

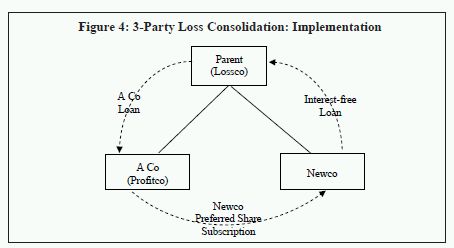

There are other variations of this structure: for example, where Lossco is the parent corporation, it is usually necessary to employ a three-corporation structure in order to meet corporate law requirements (see Figure 4). There are also variations that result in losses being accumulated in a new corporation over a number of years, which is then amalgamated into a Profitco for use in future years. However, the basic technology remains the same: the making of interest-bearing loans to subscribe for dividend-paying shares within a circular intra-group structure.

Numerous technical issues and CRA administrative concerns must be observed in creating and operating these kinds of tax-driven structures. These include the following:5

- Interest rate: the rate of interest on the Lossco loan to Profitco must be commercially reasonable in the circumstances;

- Borrowing capacity: to prevent situations where huge amounts of intra-group debt and preferred shares are created in order to speed up the generation of deductions in Profitco, the CRA limits the amount of interest-deductible debt that may be created in these structures to an amount reflecting the external borrowing capacity of the corporate group;

- Foreign loss importation: the CRA objects to any structure that amounts to importing losses from outside of Canada into Canada; and

- Inter-provincial effects: in situations where these structures result in a significant shift of taxes from one province to another due to differences in the inter-provincial income allocation of Profitco and Lossco, the CRA and provincial revenue authorities have raised concerns in the past. Indeed, provincial objections have historically been a major impediment to the creation of a formal loss transfer system.

When using these structures, it is extremely important to consult tax counsel who are very experienced in working with them, as these transactions must be planned, implemented, documented and eventually unwound with precision. Often the facts of a particular case raise unique or unusual concerns or issues, and it is vital to understand the CRA's views on such matters and to plan accordingly. The CRA's policies on various aspects of these loss consolidations have changed over time, and there are a number of subtle issues that are easy to overlook. In appropriate cases, an advance tax ruling from the CRA may be advisable.

CONCLUSION

Canadian corporations are well-advised to make the best possible use of their tax attributes. For Canadian corporate groups (including groups of Canadian subsidiaries of foreign parent corporations), intra-group loss planning is an essential element of legitimate tax minimization.

Footnotes

1 An exception is a special form of capital loss (an "allowable business investment loss") arising from the disposition of shares or debt of a Canadian-controlled private corporation all or substantially all of whose property is used in an active business carried on in Canada.

2 For example, the Department of Finance Technical Notes to s. 245 ITA (the general anti-avoidance rule) note the following: "Another example involves the transfer of income or deductions within a related group of corporations. ... There are explicit exceptions intended to apply with respect to transactions that would allow losses, deductions or credits earned by one corporation to be claimed by related Canadian corporations. In fact, the scheme of the Act as a whole, and the expressed object and spirit of the corporate loss limitation rules, clearly permit such transactions between related corporations where these transactions are otherwise legally effective and comply with the letter and spirit of these exceptions."

3 E.g., one corporation controls the other, or both are controlled by the same person or group of persons.

4 See the Department of Finance website: http://www.fin.gc.ca/activty/consult/tcc-igs-eng.asp

5 These issues were discussed in detail at a presentation by Steve Suarez of BLG and Wayne Adams, Director General (Income Tax Rulings Directorate) of the CRA, entitled "Intra-Group Loss Consolidations – Staying On-Side," at the Toronto Centre CRA & Professionals Consultation Group meeting on October 27, 2009.

About BLGThe content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.