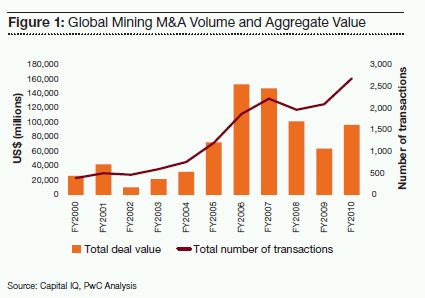

1. Number of transactions at all time high. Aggregate dollar values post impressive annual gains, but "mega deals" remain elusive.

The numbers are in—2010 results prove that the first decade of the millennium belongs to the mining sector! We tracked 2,693 global mining M&A deals worth $113 billion in 2010, bringing the decade total to over 11,000 transactions worth close to $785 billion. Indeed, the cumulative annual growth rate (CAGR) for mining M&A volumes in the decade ended 2010 was 21%. No other global industry sector has experienced comparable growth rates or volumes.

A closer look at the data:

- With 2,693 announced deals, volumes posted a 28% gain over 2009 and a 21% gain over the previous market peak (2007).

- The total value of announced deals in 2010 was 77% higher than the prior year although aggregate dollar values remained 26% lower than the 2006 peak. Values did not rebound as precipitously as volumes due to an absence of mega deals announcements (transactions over $10 billion), which skew average deal values upward and contribute disproportionately to dollar values.

- With the exception of the withdrawn $40 billion takeover offer of Potash Corporation of Saskatchewan by BHP Billiton, 2010 did not see any mining sector deal announcements breach the $10 billion mark. The largest announced deal was Newcrest Mining's $8.7 billion acquisition of Lihir Gold. Consider that 2006-2008 saw numerous $10 billion+ transactions including, among many, Vale/Inco ($20 billion) and Teck/Fording ($12 billion).

- An absence of $10 billion+ deals in 2010 was not due to lack of motivated buyers. Quite the contrary. In a mining environment generally characterized by high demand, tight supply and expensive exploration and development costs, most senior executives expressed a desire to secure takeover targets to boost reserves, increase production rates and improve access to capital. Why then did we not see a high volume of mega deal activity in 2010? Global miners have been so active that in 2010 there were simply fewer good targets with market capitalizations of >$5 billion in play.

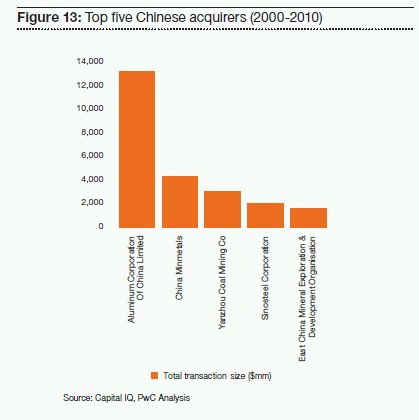

- As set out in the accompanying graph, we observed five companies that have each announced more than $20 billion in acquisitions since 2000. Together, this group contributed close to a quarter of buy-side dollar volumes between 2000-2010. The corollary of this decade-long deal binge is a limited universe of large takeover targets. Indeed, consider that a recent study by the Raw Materials Group revealed that 85% of total global industrial mine production is now controlled by only 150 companies, with the degree of fragmentation varying by commodity.

2. Buyers extend geographic reach to acquire five key resources.

While nearly all mining sub-sectors were busy from a deal perspective through 2010, five key resources dominated M&A. Mines with a primary resource of gold, copper, coal, fertilizer minerals or iron ore represented 88% of aggregate dollar values in 2010. In our top 20 deals of 2010, all but two targets (Mantra Resources, Anglo American Zinc) fell into one of these five sub-sectors. In many instances demand for key resource projects was so voracious that miners penetrated regions with higher political risk profiles.

A closer look by major resource

Gold

- Entities with a primary interest in gold were the most sought after targets in 2010, representing 44% and 31% of volume and value respectively. Six of our top 20 deals in 2010, worth close to $22 billion, were in the gold sector, including the largest and third largest deals of the year—Newcrest's acquisition of Lihir Gold ($8.7 billion) and Kinross Gold's acquisition of Redback Mining ($6.8 billion). The strategic rationale behind both these deals was reserve growth. In both instances, some measure of geographic diversification was also achieved, Lihir (Papua New Guinea and Cote d'Ivoire) and Redback (Mauritania and Ghana).

- While blockbuster gold deals typically garnered the most attention, the majority of gold targets were small-medium size entities with exploration or development stage projects. For this reason, gold targets had an average value of only $54 million, although values ranged from less than $1 million to almost $9 billion. We observed a wide variety of buyers, including two Kazakhstani producers and numerous Chinese intermediates, actively buying such projects. The majority of gold mine acquirers exhibited little risk aversion, securing assets in such frontier regions as Mongolia, Sudan and the Democratic Republic of Congo, or in new and untested geographies, such as the Canadian high Arctic. The traditional gold geographies of Latin America, North America and Australia also remained popular, although new projects in these regions were few.

- Gold sector M&A was, by and large, underpinned by expectations for further gold price strengthening amidst a backdrop of low interest rates, a depreciating US$ and infl ation. This macro backdrop resulted in an upsurge in gold demand from central banks and investors.

-

- Since the latter half of 2009, global central banks collectively transitioned to become net buyers of gold. As set out in the accompanying graph, China, Russia and India were the most active central bank acquirers in 2010. Most agree that central bank actions were motivated by a desire to diversify FX reserves away from US$ holdings.

- Statistics from the World Gold Council revealed that demand for gold by ETFs and similar investment vehicles was up 414% in mid 2010 over the prior year. This increase was partially fuelled by the emergence in 2010 of ETFs that hold physical gold.

Coal

- While coal targets represented only 5% of acquisitions (by volume), measured by total transaction value, coal targets represented 19% of the market. Indeed, six of our top 20 deals of 2010, worth over $14 billion, involved a coal target.

- Although we did observe continued acquisitions of Canadian and US based targets (Western Coal, Cumberland Resources), acquirers also extended their geographic reach into Mozambique, Russia, Poland, Colombia and China. Indeed, the largest announced coal deal in 2010 was Rio Tinto's pending acquisition of Riversdale Mining for $3.8 billion. Although headquartered in Australia, Riversdale's most attractive assets are its hard coking-coal projects in Mozambique which, according to analysts, will not come into production until 2013 but have the potential to supply 5-10% of the global market for the key steel-making material. At the time of print, the outcome of this bid, which is confused by strategic shareholdings held by Indian and Brazilian investors, is uncertain. Another interesting coal deal in 2010 was the $3 billion acquisition of two of Indonesia's largest coal producers by a holding company founded by British financier Nathanial Rothschild to raise cash for acqusitions.

- While large deals were the most talked about coal transactions through 2010, we did observe a number of tuck under buys of small coal reserve deposits by a diverse range of buyers seeking to build scale or vertically integrate supply chains. Examples of the latter rationale included buyers JFE Shoji Trade Corporation, a Japanese steelmaker and PGE Polska Grupa Energetyczna S.A., a Polish energy electrical energy company, both of whom acquired small coal properties in order to secure critical supplies for steelmaking and energy.

- In Australia we saw a complex situation surrounding takeover bids for Macarthur Coal by Peabody and New Hope fizzle out to nothing, reportedly due primarily to concerns with the resources tax, while a low profile yet successful deal by Banpu of Thailand for Centennial Coal was the largest completed deal. We also saw Indian buyers, notably Adani, making significant deals.

- Like all resource M&A in 2010, many coal deals were motivated by a need to build production capacity to meet soaring demand for coal from non-OECD nations. As set out in the accompanying graph, the United Nations Statistics Division expects coal consumption from these nations will expand by 85% through to 2035.

Fertilizer mineral mining

- Interesting and new to our annual top five target resource categories is the fertilizer mineral category, which displaced silver in our annual top five. This category covers takeover activity in the phosphate, potash and borate minerals segment of the mining market.

- Although representing less than 1% of transaction volumes, fertilizer mineral targets represented a whopping 15% of target dollar values (and likely the majority of mining headlines in 2010!). Notwithstanding the failed takeover of Potash Corporation by BHP Billiton, Brazil's Vale was one of the biggest stories of the year for the sub-sector. The South American giant acquired $4.7 billion of various fertilizer assets from Bunge in 2010 on the heels of $850 million worth of potash mine buys in Argentina and Canada in 2009. And, in what was the third largest chemical and fertilizer deal of 2010, Vale sold minority stakes in its Bayovar phosphate project in Peru for $660 million to Mosaic (35% and an offtake agreement for $385 million) and Mitsui & Co Ltd (25% for $275 million). The alliance of Vale, Mosaic and Mitsui in the latter transaction provided Vale with access to technical expertise, guaranteed product off-take and enhanced product distribution capabilities. The deal was part of the South American giants strategy to diversify its operations. The largest fertilizer deal of the year was the mega-merger of Russia's Uralkali and rival potash producer Silvinit—the $8.4 billion cash and share deal was the second largest mining deal of the year.

- Outside the major deals noted, there were a small number of <$100 million acquisitions of small potash or phosphate projects, mineral claims or quarries. Phosphate targets were largely concentrated in China and the US while various countries in South America as well as Russia and Canada were the most popular acquisition regions on the potash front due to the high concentration of the respective minerals in each of these geographies. In addition to market leaders such as Vale, a number of venture-stage miners were active acquirors of the properties.

- The emergence of fertilizer as an operational focus for miners is largely due to global concerns about food scarcity. In its most recent forecast, the Food and Agricultural Organization of the United Nations postulated that demand for food in the first half of this century will double. At the same time, crops may increasingly be used for bioenergy and other industrial purposes. Both of these forces are already resulting in tight supplies and putting upward price pressure on agricultural chemicals and fertilizers, a highly profitable state of affairs for miners of these commodities.

Copper

- M&A deals involving a target with a primary copper resource represented 19% of transaction volumes and 13% of aggregate dollar values in 2010. Our top 20 deals of 2010 profile two copper deals. The first was a traditional "merger of equals" deal between Canada's Quadra mining and FNX mining. The $1.5 billion deal provided the combined entity with a portfolio of high quality assets in the politically stable regions of Canada, the US and Chile, as well as the critical mass and financial fl exibility to pursue further M&A and exploration. The second largest copper deal of 2010 bore little resemblance to the first. Canadian-Australian listed copper miner Equinox Minerals agreed to acquire a smaller Australian peer Citadel Resource Group. The newly combined entity has a portfolio of unique high-quality assets in Zambia, and in Saudi Arabia, where Citadel had been progressing the Jabal Sayid copper-gold project.

- Similar to gold sector deal dynamics, measured by number of transactions, the majority of copper activity involved the acquisition of exploration or development stage projects. We observed intermediates and juniors, in addition to seniors, actively buying projects in the traditional copper geographies of Canada, Australia, South Africa, Chile and Peru. However, with few good projects in play and supply extremely tight, many buyers sought out projects in new and higher risk regions, namely Zambia, Saudi Arabia, Mongolia and the Philippines.

- Copper M&A was, by and large, motivated by a desire to access reserves that could fulfill strong copper demand from Asia, ahead of expected price strengthening. Indeed, those able to secure projects were well rewarded. The price of copper rallied 30% through 2010, while LME inventories were drawn down by 25%. As well, with few new copper projects coming online in 2010, supply made little headway catching up with demand—at year end, the supply/demand shortfall was 14,385 thousand metric tonnes.

Iron ore

- Targets with a primary interest in iron ore made up 9% of target volumes and 10% of aggregate value. Our top 20 deals of the year list includes three iron ore takeovers, worth $5.6 billion, the largest of which was Vale's $2.5 billion buy from BSG Resources of a collection of iron ore deposits in Guinea, including assets previously confiscated by the West African nation. Vale agreed to pay $500 million up front for a 51% interest in the projects, with the remainder to be paid as the projects meet milestones.

- The major deal driver in the iron ore subsector this year, in addition to securing reserves ahead of strong expected demand from China, was steelmakers' desire to vertically integrate supply chains in order to secure raw materials supply, an issue which our sister publication, "Metals Deals, Forging Ahead" discusses in detail in the broader context of the steel market and its unique dynamics.

3. Canada and Australia governments look inward. Canadian and Australian corporates look outward.

2010 will undoubtedly go down as the year in which the most talked about mining issue was a matter of philosophy—who should benefit from resources imbedded in national soil— citizens or shareholders?

The BHP Billiton/Potash Deal and Australia's MRRT tax were largely behind these conversations:

- BHP Billiton's hostile bid for Canada's potash giant

was shut down by Investment Canada for not meeting a "net

benefit" test for the country. The rejection was only the

second since the Investment Canada Act came into force in 1985 and

stunned global dealmakers. Perhaps more surprising than the actual

rejection of BHP's bid by Investment Canada, however, was

Canada's pre-emptive position on a potential Asian bidder (a

bidder which, for the record, had yet to even materialize). The

Conference Board of Canada released an official review of the

proposed transaction to the Government of Saskatchewan and

expressly stated

"The acquisition risk associated with a Chinese consortium bid, however, is more serious. As we discuss, a Chinese bid mingles state strategy with commercial strategy. Under this scenario, the Province cannot count on market discipline to manage its supply-side risk. Potash is critical to China's food needs and therefore there may be a tendency for the state to "subsidize" food through cheap inputs like potash."

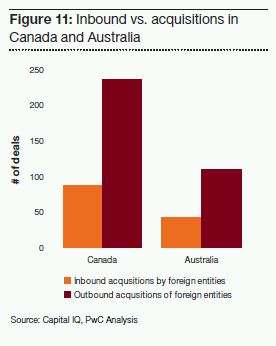

- On the other side of the world, a historically equally mining friendly nation took an equally tough stance on the mining sector. On July 2nd, 2010, the Australian Government announced the Mineral Resource Rent Tax ("MRRT"), a profits-based tax which is intended to apply to iron ore and coal and is projected to come into effect on July 1, 2012. The proposed new tax applies over and above any corporate tax paid, at a rate of 30% (reduced to 22.5% with an 'expertise' credit applied). In essence, this rate is applied to the value of the minerals as close to the point of extraction as possible, less all costs incurred up to that point. Its aim is to tax the value of the natural resource rather than any value added by the miner. Chief among the Australian Federal Government's rationale for the proposed tax was a concern that Australians were not benefiting enough from the revenue being generated by its vast natural resources. (It should be noted that the MRRT was a significantly watered down tax from the initially suggested Resource Super Profit Tax announced earlier in 2010). Some further details regarding the MRRT are available at http://www.pwc.com.au/assurance/ifrs/assets/DiggingIFRS-28Jan11.pdf . While the Australian government has made it clear foreign investment is still welcome, for sophisticated foreign investors choosing a jurisdiction to invest capital, the concept of a specialist tax regime imposing more costs, is clearly a deterrent. Indeed, of 2,693 transactions in 2010, only 43 involved a non-Australian acquiring an Australian entity (by contrast, Canada saw 87 acquisitions by non-Canadian entities).

- It is interesting that while national interests in Canada and Australia raised concerns about foreign resource ownership, corporations in Canada and Australia were busy buying foreign assets (as has been the privilege of these resource rich nations for the better part of this century). In fact, in somewhat of a "hollowing in", Canadian owned entities completed 236 acquisitions of foreign targets worth $8 billion while Australian owned entities completed 109 acquisitions of foreign targets worth $9.7 billion.

4. High profile bidding wars see some buyers left out or having to boost purchase price.

Protectionist sentiment was not the only thing preventing mining deals from getting done. 2010 was indeed a seller's market. A number of acquirers failed in their acquisition attempts, or were prompted by shareholders and/or boards to retreat and return with better terms.

- Among such instances were:

-

- In September 2010, Vale put forth a bid to acquire

Paranapanema, Brazil's sole copper smelter, for approximately

R$1.13 billion. In response to shareholder criticism, Vale

subsequently raised its offer to R$2.4 billion, but the bid failed

again, with less than 50% shareholder approval. Vale did not

counter and was unable to secure Paranapanema, a target it has been

trying to acquire since early 2008. Paranapanema CEO Luiz Antonio

Ferraz stated that the company

"should remain independent," and that "it has a life of its own."

- Also in September 2010, Goldcorp trumped Eldorado Gold's

C$3.4 billion hostile bid offer for Andean Resources Ltd., owner of

the Cerro Negro gold project in Argentina, by putting forth a C$3.6

billion offer. Eldorado did not attempt to counter Goldcorp's

offer, with Eldorado CEO Paul Wright stating quite controversially

that he did not want to get into a valuedestroying auction:

"The gold industry, as a whole, has an appalling track record of value destruction and Eldorado has no intention of following in these unfortunate footsteps."

- In February 2010, Newcrest Mining Limited approached Lihir Gold Limited with an A$9 billion offer to combine the two companies to create the world's fourth largest gold company. This proposal was rejected by shareholders due to their concerns that it undervalued Lihir's portfolio of assets. In May 2010, a final bid was made that was accepted by the board of directors, and ultimately the shareholders of Lihir Gold. Prior to the final offer being made, speculation ran rampant that other bidder's were seriously looking at acquiring Lihir. The final offer was at a 40.8% premium to Lihir Gold's share price immediately prior to the first offer in February, and ultimately valued Lihir Gold at A$9.5 billion.

- In September 2010, Vale put forth a bid to acquire

Paranapanema, Brazil's sole copper smelter, for approximately

R$1.13 billion. In response to shareholder criticism, Vale

subsequently raised its offer to R$2.4 billion, but the bid failed

again, with less than 50% shareholder approval. Vale did not

counter and was unable to secure Paranapanema, a target it has been

trying to acquire since early 2008. Paranapanema CEO Luiz Antonio

Ferraz stated that the company

5. China's role in global M&A overstated. Australia, Canada and Developed Europe dominate global buy-side activity.

It should come as no surprise 2010 saw continued buy-side activity involving Chinese entities. During 2010, we observed 161 acquisition announcements involving a Chinese entity worth close to $12 billion. Year end results bring the decade ended 2010 deal tally to 400 deals worth close to $48 billion. Front of mind for us, however, is not the volume/value trend. The results speak for themselves and are indisputably notable considering that Chinese buyers were negligible players in mining M&A only five years ago. Rather, we wanted to know what M&A in the decade ended 2010 told us about how China is faring overall with its "go-out" strategy—the nation's ambitious plan, announced in 2001, to boost its investments overseas.

- Much western rhetoric has been devoted to the suggestion that China, through its state owned enterprises, is amassing de facto control of the world's mining sector. Global mining M&A data, however, would suggest otherwise. Unlike the energy or financial services sectors, where we have seen Chinese buyers making numerous $5 billion+ acquisitions into world leading corporations, few Chinese buyers have successfully secured controlling stakes in world leading mining companies. Rio Tinto and Xstrata alone completed more acquisitions (in value terms) in the 2000-2010 period than all Chinese buyers cumulatively.

-

- The largest equity deal to date involving a Chinese entity has been the joint $14 billion acquisition by Aluminum Corporation of China (Chinalco) and Alcoa of a 9% stake in Rio Tinto (and subsequent rights purchases to avoid dilution). No other Chinese entity has even breached the $3 billion price point. Although Chinalco's failed second bite at Rio Tinto would have easily done this and also created much debate in 2009!

- As set out in the accompanying map on page 20, we tracked the project locations of Chinese targets in the 2000-2010 period. During this time, 61% of projects acquired were in China, while an additional 16% were in an adjoining Asian geography or in an emerging market region (South America, Africa, Latin America). Only 22% of transactions involved a target with a project on "western" soil.

- As well, consider that in 2010 only 6% of buyers in global mining M&A deals (by volume) were Chinese, the highest proportion to date, but still dwarfed by acquirers from North America (51.8%) and Australia (16.2%). The largest Chinese-led deal of the year was East China Mineral's announced acquisition of Brazil's Itaminas Iron Ore Mine for $1.2 billion (including the assumption of $400 million in debt). While smaller than the Rio Tinto acquisition, this deal was arguably more notable because East China acquired a 100% equity stake in the entity, giving the state-owned enterprise complete control of the operations and management.

What then, have Chinese dealmakers been doing?

- In the west, Chinese entities have largely been opportunistic partners, seeking to secure supply by being long-term creditors, often passive. The most notable case in point being the $1.5 billion investment by China Investment Corporation (CIC), in Teck Resources. (In 2009 CIC took a 17.2% in Class B Teck shares, carrying only a 6.7% voting interest, in exchange for a $1.5 billion cash infusion).

-

- The most notable strategic partnership of 2010 was Rio Tinto and Chalco's joint venture to develop and operate the Simandou Iron Ore project. The project, 95% owned by Rio Tinto, is located in the south eastern part of Guinea in West Africa and is currently undergoing the final stages of exploration and feasibility studies. When completed, this world-class mining operation is expected to be one of the largest integrated iron ore mine and infrastructure projects ever developed in Africa. Under the terms of the agreement, Chalco will provide $1.35 billion on an earn-in basis which will give them an effective 44.65% stake in the project while reducing Rio Tinto's stake to 50.35%. The Guinean Government holds an option to buy up to a 20% stake in the project but the incoming government is looking to define a new mining policy where Guinea would own a 33% interest in the country's mines. Key aspects of the legal status of this project are still to be clarified; accordingly this transaction has been excluded from M&A statistics.

- In the emerging world, especially in frontier markets, China is actively acquiring small to medium size projects, often also providing funding for local infrastructure as part of deal consideration (China has been especially active in rail construction or port-to-harbour developments near acquired projects in Africa). Our data suggests that just over 80% of China led deals are the latter type.

- The reality is that, for most key metals and minerals, with the exception of rare earths, China's current supply of resources largely depends on Western owned entities. As we discuss further in our 2011 outlook, however, we expect this dynamic will change, albeit very slowly.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.