Gardiner Roberts LLP are most popular:

- within Insurance, Law Department Performance and Privacy topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- in North America

- with readers working within the Accounting & Consultancy, Technology and Law Firm industries

INDIVIDUAL TAX RATES

- New annual reporting requirements for trusts after 2020

- No individual tax rate changes

- At‐risk rules for tiered

partnerships

- For a limited partner that is itself a partnership, its share of losses from the bottom partnership that can be allocated to its own members will be restricted by that limited partner's at‐risk amount in the bottom partnership

CORPORATE TAX RATES

Private Company Tax Planning

- The Federal Small Business Rate

- Reduced from 10.5% to 10% for 2018 and to 9% for 2019

- Given no change in the Ontario corporate tax rates, the combined small business rate for 2018 will be 13.5% and for 2019 it will be 12.5%

- Limiting Access to the Small Business

Rate

- Response to widespread criticism of proposed taxation of passive investment income

- Significant reversal from previous proposals to impose heavy tax burdens on CCPC's with passive income

Private Company Tax Planning/ Passive Investment Income

- Propose to phase out the lower rate on a straight‐line basis for associated CCPC's with between $10 million and $15 million of taxable capital employed in Canada

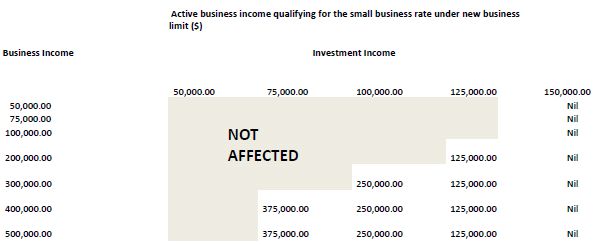

- If a CCPC and its associated corporations earn more than $50,000 of passive investment income the amount of income eligible for the Small Business Rate would be gradually reduced

- The Small Business Deduction would be reduced by $5.00 for every $1.00 of investment income above the $50,000 threshold

- As a result, the Business Limit would be reduced to zero at $150,000 of investment income

Private Company Tax Planning/ Refundability of Tax on Investment Income

- Propose new refundable tax account: "eligible RDTOH" which tracks refundable taxes paid under Part IV on eligible portfolio dividends (i.e. from non‐connected corporations), and Part IV tax payable because of dividends received from connected corporations that received a dividend refund on paying a dividend from its eligible RDTOH

- Any taxable dividend (whether eligible or non‐eligible dividend) entitles the corporation to a refund from its eligible RDTOH account

Private Company Tax Planning/ Refundability of Tax on Investment Income

- Propose second new refundable tax account: "non‐eligible RDTOH", includes the current RDTOH account which tracks refundable taxes paid under Part I on investment income, as well as under Part IV on noneligible portfolio dividends (i.e. dividends that are paid by nonconnected corporations as non‐eligible dividends)

- Refunds from this account will be obtained only on payment of noneligible dividends

- An ordering rule provides that payment of a non‐eligible dividend will generate a refund from its non‐eligible RDTOH account before the corporation obtains a refund from its eligible RDTOH account

Private Company Tax Planning/Income Sprinkling

- Plan to proceed with revised proposals dated December 13, 2017, effective January 1, 2018 to impose tax on split income ("TOSI Rules") at top rates

- Parliamentary Budget Officer, Jean‐Denis Frechette, estimates that these tax changes will result in a windfall for government revenues: $356 million for 2018‐2019, versus Finance's estimate of $190 million, and $429 million by 2022‐2023 versus $220 million per Finance

- Presumption is that TOSI Rules apply to an individual who earns income from a private business that is a dividend, interest, partnership or trust allocation or capital gain, unless an exception applies

- "Excluded Amount" includes income and gains from inherited property provided the individual has not then attained 24 years of age; income derived by an individual who has then attained 17 years of age if from an "unrelated business"; for individual between 17 and 24 there is a "safe harbour" return based on a prescribed rate of return on an arm's length property investment by the individual; for individual who then has attained 24, income or gains from an "excluded share" which is a share of a corporation carrying on a non‐service business and in which the individual holds at least 10% of the shares, or attains a reasonable return on capital invested

- "Excluded Business" means a business in which the individual is actively engaged on a regular, continuous and substantial basis

International Tax Measures

- Proposal to deem the activities of a foreign affiliate to be a separate business resulting in Foreign Accrual Property Income, where the income from such activities accrues to the benefit of a specific taxpayer under a tracking arrangement, whether the foreign entity employs more than five employees or provides that each taxpayer can make use of a separate cell of such entity

- Sharing Information

- Amend CBCA to disclose beneficial ownership and eliminate bearer shares

- Tax information will now be open to be shared with Canadian police officers, and foreign countries that are mutual assistance partners, investigating serious crimes, such as terrorism, organized crime, money laundering

HST

- Propose new rule for general partners of an investment limited partnership, so that management and administrative services performed by a GP will be considered a taxable supply to the limited partnership, based on the FMV of such services

- An investment limited partnership

means an LP, the primary purpose of which is to invest funds in

property consisting primarily of financial instruments

- e.g. a fund promoted to invest in securities or interests in other LPs

- excludes an LP that primarily invests in real property

Marijuana Tax

- Propose new federal excise duty under the Excise Act, 2001 to be imposed on federally‐licensed producers at the higher of (a) a flat rate applied to a quantity of cannabis contained in the final product, and (b) a percentage of the dutiable amount of the product sold by the producer

- Generally, the dutiable amount is the quantity of cannabis contained in the final producer's selling price that does not include cannabis duties

- All cannabis products will have to have an excise stamp before they can removed from the premises of a cannabis licensee and enter the market for a retail sale

- Also, cannabis products that might otherwise be exempt from HST as being agricultural or basic groceries will become subject to HST

- Revenue sharing: 25/75, federal/provincial

Ontario Budget

- For individuals, the budget proposes to eliminate the surtax on personal income tax, resulting in some restructuring of tax rates but no change at the top rate: still 53.53%

- For corporations, Ontario will

generally parallel the Federal changes:

- Small business rate going down from 4.5% to 3.5%, resulting in combined rate of 13.5% in 2018 and 12.5% in 2019

- Adopt the phase out of the small business deduction

- Adopt income sprinkling rules – TOSI

- Agree on cannabis taxation and revenue sharing

- Ontario is linking its cap‐and‐trade carbon market to that of Québec and California

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.