2.3. Tax on Services (ISS)

ISS is the municipal tax on services levied on the import and the rendering of services listed in Federal Supplementary Law 116/03.

Said law has fixed the ISS maximum rate at 5% and the minimum rate at 2% (some municipalities adopts lower rates, against the law) and ruled the ISS exemption on exports, defining exports as the rendering of services to non-residents as long as the results of such services are not produced in Brazil.

Such definition has raised serious concerns, as there is no clear criteria to identify what should be understood by "results produced in Brazil". Taxpayers are the service providers. However, in the case of imports of services, the importer is responsible for the calculation and collection of the tax due by the foreign party. The ISS taxable basis is the service price and tax rates vary from municipality to municipality by type of service.

As a general rule, the tax must be paid to the municipality where the establishment performing the service is located. However, there are some exceptions to this rule depending on the type of service. For instance, in case of performance of civil construction, hydraulics or electrical engineering services, the ISS is due to the municipality where the service is provided.

Supplementary Law 116/03 allows the municipalities to determine that the engaging party is liable for the withholding and payment of the ISS in certain cases.

2.4. Contribution for the Social Integration Program (PIS) and Contribution for S ocial Security Funding (COFINS)

PIS and COFINS are federal social security contributions levied on:

(A) revenues earned by legal entities, with few exceptions (e.g. dividends and revenues derived from exports of goods or services are not taxed, in the last case as long as the export revenues are cashed in Brazil) and

(B) imports of goods and services. In such cases, taxable basis are, respectively: (i) customs value of the goods plus ICMS and the same contributions (PIS and COFINS must be included in their own taxable basis) and (ii) amounts paid or credited for imports of services, plus WHT, ISS and the same contributions (PIS and COFINS included in their own taxable basis). The Federal Revenue Service has described how PIS and COFINS shall be calculated in this case.

PIS and COFINS are mainly calculated according to the non-cumulative or cumulative systems, which may coexist on a case by case basis. Exemptions and specific rules apply to certain businesses and certain income on a case-by-case basis.

PIS and COFINS are highly regulated taxes and represent a significant share of the overall Brazilian tax collection. Disputes and controversies are frequent in this field, especially regarding the right to tax credits.

2.4.1. Non-cumulative System

PIS and COFINS are levied on gross revenues of legal entities at rates of 1.65% and 7.6% respectively. Nowadays, financial revenues are subject to a zero percent rate, except for a few cases.

The taxpayer is entitled to tax credits provided by law to offset PIS and COFINS debts, generally corresponding to the rate of each contribution (1.65% and 7.6%), among which we highlight the following:

A) contribution paid on (i) domestic purchases or imports of goods for resale or manufacturing inputs and (ii) services hired by the taxpayer to provide services to its customers and/or for producing goods for sale or renting;

(B) expenses with electric energy, rent of buildings, rent or lease of machines and equipments used for the activities of the taxpayer and transportation costs relating to sales; and

(C) depreciation expenses relating to fixed assets imported or purchased in the domestic market and used in the manufacturing process, for renting or for the rendering of services (alternatively, such credit can be calculated at 1/48 per month of the cost of acquisition of the relevant fixed asset – general rule – or at 1/24 per month of the same cost in certain cases).

As the law restricts tax credits, the PIS and COFINS tax burden is significant.

Generally, legal entities that calculate their corporate taxes (IRPJ and CSLL) based on the actual profit system are subject to PIS and COFINS based on the non-cumulative system. However, the cumulative system is mandatory in some cases, irrespectively of the method chosen for the calculation of the IRPJ and CSLL.

If a company has activities/revenues subject to the cumulative and non-cumulative systems, PIS and COFINS tax credits must be proportioned to the revenues subject to the non-cumulative system.

2.4.2. Cumulative System

In the cumulative system, operational revenues earned by legal entities are taxed at the rates of 0.65% (PIS) and 3% (COFINS). The taxpayer has no tax credits for the contributions paid on imports or relating to domestic purchases and expenses incurred.

Based on paragraph 1 of article 3 of Law 9718/98, non-operational revenues, including financial revenues, should be included on PIS and Cofins taxable basis in the cumulative system. Such provision was revoked by Law 11 941 , issued on May, 2009. This happened in line with decisions rendered by the Federal Supreme Court, which determined that the referred provision was unconstitutional. However, for the period before May, 2009, the right to exclude non-operational revenues from PIS and Cofins taxable basis depends on a judicial decision on the matter for each legal entity.

Generally, legal entities that calculate their corporate taxes (IRPJ and CSLL) based on the deemed profit system are subject to PIS and COFINS according to the cumulative system (in some cases, the cumulative system is mandatory, irrespectively of the method chosen for the calculation of the IRPJ and CSLL – e.g. civil construction until the end of 2010).

2.4.3. Specific PIS and COFINS Rules

Specific rules apply per type of revenue or activity, such as:

(A) financial institutions;

(B) pharmaceutical, automotive, beverage, and tobacco industries;

(C) fuel industry; and

(D) hygiene and cosmetics products.

Among such specific rules, we highlight:

(A) tax centralization rules, by means of which PIS/COFINS are charged only once, from a chosen person of the relevant market chain; and

(B) tax substitution rules, by means of which a person appointed by the law must be liable to calculate and collect PIS/COFINS due by other persons, on past or future transactions (in the latter case based on estimate prices).

Such tax centralization and tax substitution rules are frequent in sectors with high informality levels. A tax substitution system applies, for instance, to tobacco industries, in which case importers and manufacturers will be liable for the taxes due at the retail level.

2.4.4. PIS-Import and COFINS-Import

According to Law 10865, since 2004 PIS and Cofins are due on imports of goods and services generally at the rates of 1.65% and 7.6%, respectively. Regarding these transactions, the taxpayer subject to the non-cumulative system is usually entitled to tax credits.

2.4.5. PIS and COFINS Withholdings

Among other cases, PIS and COFINS withholdings are required:

(A) on payments for certain professional services rendered by legal entities to other legal entities, at rates of 0.65% and 3% respectively, as prepayments of the beneficiary's contributions, regardless of whether such beneficiary is taxed based on the cumulative or non-cumulative system; and

(B) on payments made by the federal administration to Brazilian legal entities for goods supplied or services rendered, at rates of 0.65% and 3% respectively, regardless of whether such beneficiary is taxed based on the cumulative or noncumulative system (state and municipal administration may comply with this withholding obligation as agreed with the federal administration).

2.5. Economic Intervention Contribution (CIDE) on Payments of Royalties, Technical Services and Administrative Assistance

CIDE is a Federal contribution levied at a 10% rate on the amounts paid, credited, transferred, delivered or otherwise made available to non-residents for technology transfer or technology license agreements, patents and trademarks licenses, technical assistance, technical and administrative services9 and any agreement involving royalty payments.

In case of service fees, WHT and ISS shall be included in the CIDE taxable basis. A CIDE tax credit is granted for payments of royalties for patents and trademark licenses 10 which may be offset against the amounts to be paid as CIDE in subsequent remittances of the same nature.

2.6. Tax on Financial Transactions (IOF)

IOF is levied on credit, exchange and insurance transactions, as well as on securities at variable rates. Credit transactions are subject to the IOF at a 0.0041 % daily rate and to a 0.38% surcharge. Foreign currency exchange transactions are subject to a general 0.38% rate. Insurance transactions are generally subject to the IOF at rates varying from 0% to 7.38%. Securities transactions are subject to the IOF at rates that vary according to the type of investment and investment period. Generally, floating income investments and fixed income investments for 30 days or more are subject to a zero percent rate.

2.7. Property Taxes

2.7.1. Urban Property Tax (IPTU)

IPTU is a municipal tax levied annually on the ownership or possession of any real estate located in urban areas. The taxable basis corresponds to the fair market value of the property at a rate that may vary according to the Municipality and the use and price of the real estate.

In the city of São Paulo, IPTU rates range from 1% to 1.5% with discounts or additions granted based on the market value (calculated as provided by the Municipal law) and use of the relevant property.

2.7.2. Tax on Vehicles' Ownership (IPVA )

IPVA is a state tax levied annually on the ownership of vehicles (car, trucks, buses, tractors, boats, yachts and aircraft11 ). The taxable basis corresponds to the fair market value, determined every year by the State Treasury Secretariat, that takes into consideration the brand, model and age of the vehicle. The applicable rate may vary according to each State. In São Paulo, for instance, the tax rate varies from 1.5% to 4%.

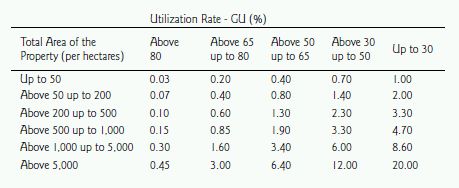

2.7.3. Tax on Rural Properties (ITR)

ITR is a federal tax levied annually on the ownership or possession of rural property (real estate located outside the urban zones of the cities). The Federal Union may enter into conventions with Municipalities to delegate to such Municipalities the duty to inspect and collect the ITR.

The taxable basis is the value of the taxable area, which shall be calculated in accordance to specific rules. Tax rates vary depending on the total area of the property and level of use of the areas that can be exploited for agricultural purposes, according to the table of rates below.

Constitutional Amendment 42/03 has confirmed ITR progressive rates and granted an ITR tax exemption to small sized rural property exploited by its owner, who does not have any other real estate. Note that ITR has been an important tool to discourage unproductive rural properties.

2.8. Tax on Real Estate and Related Rights Transfer (ITBI)

ITBI is a municipal tax levied on inter vivos and remunerated transfers of ownership or in rem rights over a real estate. The taxable basis corresponds to the fair market value of the property at a rate that may vary according to the Municipality. In the city of São Paulo, the general rate is 2%.

This tax is not levied on the contribution of a real estate and/or in rem rights in exchange for capital of a legal entity or on ownership transfers resulting from corporate reorganizations, such as mergers, spin-off or liquidation, except if, in any such cases, the acquirer's core activity is trading or leasing real estate as provided by the law.

2.9. Donation and Inheritance Tax (ITCMD)

ITCMD is a state tax levied on donations or inheritances. The taxable basis corresponds to the fair market value or value of the relevant donation or inheritance. Applicable rates vary from State to State, subject to a maximum 8% rate. In São Paulo, ITCMD is charged at 4%.

3. Customs Duties and Export Taxes

3.1. Customs Duty (II)

II is a federal tax levied on imports of goods and charged for the clearance of such goods from customs.

Generally, II taxable basis is the CIF value, with due regard to the 1994 General Agreement on Trade and Tariffs (GATT) customs valuation rules. The Agreement describes six methods, which may be successively applied in order to ensure that II is paid on market prices.

Applicable rates vary per imported item - according to the relevant tax classification under the Mercosur Common External Tariffs Table ("TEC-SH"), organized based on the Mercosur Nomenclature (which is based, in turn, on the Brussels Nomenclature) - and may range from 0% to 35%. II is not a VAT.

Please note that IPI, PIS/COFINS and ICMS are also levied on imports of goods, as described above.

3.1.1. Special Customs Regimes Available

Brazilian law allows the admission of imported goods into the Brazilian territory without the immediate payment of taxes, under special import regimes, as long as certain requirements are met. The most common regimes are as follows.

(A) Temporary Admittance of Foreign Goods

Under this regime, some goods are admitted into Brazil for specific purposes and for a certain term, with total or partial suspension of the relevant federal taxes levied on imports. The total tax suspension is usually applicable in the case of goods imported for sport competitions, artistic and cultural exhibitions, scientific and trade fairs. If the imported goods are nationalized, the corresponding taxes will be levied as if the tax suspension had never taken place.

The partial tax suspension applies to goods imported for economic purposes, such as the rendering of services or the manufacturing of other goods (e.g., import of equipment and machines under operational lease agreements). When such goods are admitted into the national territory, relevant taxes are charged proportionally to their respective useful life and term of stay in the country.

If such imported goods are nationalized, relevant taxes are due according to the remaining time of their useful life. Among other requirements, for the partial tax suspension, a guarantee must be provided.

The total/partial tax suspension applies to Custom Duties, IPI and PIS/COFINS on imports, and an ICMS exemption or a taxable basis reduction may apply, as provided by the law of each state, as authorized by the Agreement 58/99.

(B) Drawback It is applicable to the import of goods used for manufacturing products to be exported or that had already been exported.

The regime allows (i) the suspension of taxes due on imports provided that the taxpayer uses the imported products to manufacture products to be exported within a specified term (generally one year, but it may be extended for the same term); or (ii) the exemption of the federal taxes due on imports for replacement of stocks of imported goods subject to taxes and used in the manufacturing of products that had already been exported. If such exports are not carried out (or if exported amounts are lower than the amounts that should be exported) the taxes suspended must be paid with penalties and interest.

In case of suspension of federal taxes (Custom Duties, IPI and PIS/COFINS on imports), an ICMS exemption may be granted, as provided by the law. In case of exemption of federal taxes, the drawback will not be applicable to the ICMS.

This special regime (drawback suspension) can be combined with drawback "green – yellow" (drawback "verde – amarelo"), in which the taxpayer can buy inputs in the domestic market to manufacture products to be exported. This tax benefit does not apply to ICMS.

(C) Bonded Warehouse

Under this regime the goods are admitted into consignment in Brazil for a period of one year (which may be extended for two more years from the time of the custom clearance) and the payment of import taxes is suspended as long as the goods are stored at certain customs areas.

The beneficiary of the regime shall be liable for the stored goods and for all measures required for the nationalization of such goods, as the case may be (the goods belong to the consignor as long as stored at the bonded warehouse).

This regime applies to Custom Duties, IPI, ICMS and PIS/ COFINS on imports.

(D) Industrial Warehouse (RECOF)

According to this regime the industrial establishment remains under customs control and the taxes are suspended provided that the beneficiary exports a minimum amount of goods manufactured with imported raw-materials. This regime applies only to manufacturing of products related to aviation, vehicle, telecommunication, information and high technology electronics fields.

If the minimum amount is not exported after a certain period of time, taxes will be charged as in an ordinary import, increased by penalty and interest and the beneficiary's right to the RECOF benefits may be cancelled.

To be entitled to this regime the company must, among others: (i) have a net worth equal or greater than BRL 25 million (approximately USD 14 million); (ii) undertake to export goods manufactured with imported inputs equivalent to 50% of the total imported goods and not less than USD 10 or 20 million per year, depending of the manufacturer's activity; (iii) use, in one year, at least 80% of the imported inputs on the manufacturing process; and (iv) have a computerized stock control system accessible by Federal Revenue Service Agents. This regime is applicable to Custom Duties, IPI and PIS/ COFINS on imports.

3.2. Export Tax (IE)

Export tax is a federal tax levied on exports of national or nationalized products, imposed when the products leave the Brazilian territory. Generally speaking, the taxable basis is the export price of the product. The rate may vary according to the tax classification number of the product, but, currently, the rate is zero for virtually all products, except for (i) leather, fur and dead animal skin, which are subject to the tax rate of 9%; and (ii) cigarettes and guns destined to Latin America, subject to tax rate of 150%.

4. Payroll Taxes / Welfare Contributions

4.1. Social Security Contributions

The Brazilian Social Security System is basically funded by contributions of both companies and employees. These contributions are levied on the employee's overall salary. The companies' contributions vary from 26.3% to 31 ,8% (aggregate rates), according to the company's activities, the company's Accident Prevention Factor (FAP) which is calculated, among other factors, based on the company's accident occurrence index, and include, among other contributions, the contribution to fund Social Service and Training Programs (such as SESI, SENAI, SESC and SENAC).

The employees' contribution must be withheld by the employer at rates varying from 8% to 11%, as provided by law, limited to a maximum monthly contribution of BRL 375.82 (approximately USD 209). As for third service providers (individuals), the companies must: (a) contribute with 20% of their overall compensation and (b) withhold 11% of said compensation, on behalf of such professionals (in this latter case the limit of BRL 375.82 also applies).

4.2. Severance Indemnity Fund (FGTS)

The employer must make monthly deposits in accounts opened for each employee with a governmental financial institution. Such funds can only be withdrawn by the employee in certain circumstances. Currently, the total FGTS cost corresponds to 8% of the employee's overall compensation.

In case of dismissal without cause, the employer is also subject to pay a penalty corresponding to 50% of the total FGTS deposits it has made in the employee's account (40% deposited in said bank account and 10% paid to the Federal Government).

5. TAX INCENTIVES

5.1. Free Trade Zones

5.1.1. Manaus Free Trade Zone ("ZFM") ZFM incentives are granted by the Brazilian Constitution until 2023 and comprise federal, state and municipal tax benefits, such as:

Federal taxes incentives:

II: up to 88% tax reduction on several inputs used in the manufacturing process at ZFM according to a Basic Producing Process defined by law;

IPI: exemption on imports of certain inputs to be manufactured or consumed at the ZFM, on shipment of products made in Brazil to ZFM for consumption in the region and on shipment of products manufactured in ZFM to other regions within the national territory, including ZFM;

IRPJ: tax reduction for applications filed with the ZFM until December 31, 2013; PIS and COFINS: 0% on imports from ZFM of (i) inputs to be manufactured at the ZFM and (ii) fixed assets listed in Decree;

PIS and COFINS: 0% on revenues arising from sales by legal entities based outside ZFM of goods to be consumed or manufactured inside ZFM and on revenues arising from sales of raw-materials, intermediate products and packaging materials by legal entities based inside ZFM to ZFM companies;

PIS and COFINS: reduced rates on sales of products manufactured by ZFM (provided that certain characteristics of the purchaser are met).

State taxes incentives:

ICMS: exemption on the shipment of national products from other Brazilian States to ZFM companies;

ICMS: tax refund for companies established in ZFM on the shipment of goods to other States, varying from 55% to 100% of the tax accrued.

5.1.2. Other Free Trade Zones There are other free trade zones in Brazil, to which similar benefits apply. Similar IPI benefits are also granted to taxpayers based in the West Amazon region (States of Acre, Rondônia, Roraima and Amazonas).

5.2. Regional Development Incentives

Companies in the North, Northeast and in certain States in the Middle West (Mato Grosso) and Southeast (certain areas of Espírito Santo and Minas Gerais) can benefit from federal, state and municipal incentives.

The most important one relates to the IRPJ, which is expected to expire in 2013. In general terms, a 75% IRPJ reduction can be granted for a period of up to 10 years to activities considered of priority (as defined by Presidential Decrees) for the development of those regions. The benefit shall be approved by the Federal Revenue Service based on a prior technical analysis of the Amazon and Northeast Development Superintendence (SUDAM/SUDENE).

Special rules ("lucro da exploração") apply for the calculation of the incentive. The tax waiver must be registered as a profit reserve and can only be used to offset losses or increase the company's capital (cannot be distributed to its partners).

5.3. Technological Innovation Incentives

Applicable to legal entities that carry out researches of new products, new manufacturing processes and improvements in quality, productivity and competitiveness of existing products and manufacturing processes.

IRPJ and CSLL benefits:

Deduction of expenses with technological innovation R&D and payments of certain royalties;

Exclusion of certain percentages of amounts paid as technological R&D, patented technological development or registered cultivars;

Full depreciation in the year of acquisition of new assets used in the technological R&D;

Accelerated amortization of amounts paid to purchase intangibles linked to the technology innovations R&D;

Other benefits:

10% credit of the tax withheld on payments or credits to non-residents of royalties, scientific or technical assistance and technical service fees. Valid until December 31, 2013 upon compliance of certain requirements;

0% rate for payments or credits to non-residents for the registration and maintenance of trademarks, patents, and cultivars abroad;

50% reduction of the IPI levied on the purchase of assets destined for technological R&D; Government subvention of up to

60% of the value of the remuneration of researchers holding masters or PHD degrees.

5.4. Other Incentives

6. PUBLIC DIGITAL BOOKKEEPING SYSTEM (SPED)

Since 2000, the Federal Union, States and Municipalities have worked to link their electronic systems and to share a common electronic platform, where information related to books and documents that comprise the commercial and tax bookkeeping of legal entities shall be received, validated and stored. This common data base must be available for consultation by the Federal, State and Municipal tax administrations and other governmental agencies.

The SPED was officially launched by Decree 6022/07, later supplemented by the Normative Instruction of the Federal Revenue Service 787/07 and its amendments.

The SPED should simplify the paper work and tax returns, as some of the most important information about taxpayers shall be available on-line. Once SPED is fully implemented, Brazilian tax authorities will have access to detailed information about the taxpayers' economic activities. The Federal Revenue Service – which manages, governs and supervises the SPED – is frequently working on the improvement of the digital system and issuing new rules for its regulation.

As part of the SPED, all legal entities that pay corporate taxes based on the actual profit system must keep their accounting records in digital format and submit such files to the Federal Revenue Service since 2009.

The implementation of e-tax books also started in 2009, for the legal entities expressly listed by State law. Moreover, commercial invoices started to be issued electronically, per economic activity, gradually.

It is worth mentioning that, at present, some of the most important tax returns, such as the legal entities' income tax return, are already filed electronically. In some cities, such as São Paulo, service invoices are also issued electronically.

We point out that taxpayers cannot oppose their commercial secrecy against Brazilian tax authorities, as a general rule. The banking secrecy has also been relaxed by Supplementary Law 105/01. In light of such framework, taxpayers must be alert to the need of receiving adequate protection as regards their secrecy rights.

Footnotes

1 Estimated exchange rate: BRL 1.80 per each USD 1.00.

2 Usually applicable to small-size companies with total revenues of less than BRL 48 million (approximately USD 26.7 million) in the previous year, that are not subject to restrictions otherwise imposed by law (e.g., financial institutions, companies earning profits/income from abroad etc.). The taxable basis (deemed profit) is calculated on a quarterly basis upon the applicability of certain percentages on the company's gross sales revenue which may vary per activity performed by the company. The general percentages are 8% (for IRPJ) and 12% (for CSLL). In case of services the percentage is 32% for both taxes. Other revenues may be subject to other specific percentages or may be fully added to the taxable basis.

3 For a long time used at the sole discretion of the tax authorities. Recently the companies have been authorized to use this income tax system in some specific cases, such as when their accounting records are not reliable for the calculation of the taxes due. It is similar to the "Deemed Profit System" (also calculated on a quarterly basis), but the percentages applicable on the companies' revenues are 20% higher for IRPJ purposes.

4 The profit sharing or bonus paid to employees is taxable for the respective beneficiaries.

5 An experts' report can be used to support different rates.

6 See definitions on Section 1.1.2.3.

7 Under the "Deemed Profit" and the "Arbitrated Profit" such taxes must be calculated on a quarterly basis.

8 The taxable basis is calculated by applying certain percentages on the gross sales revenues (similar to the Deemed Profit System – see footnote 2 above). The general percentages are 8% (for IRPJ) and 12% (for CSLL). In case of services the percentage is 32% for both taxes. Other revenues shall be fully added to the taxable basis.

9 Even if they do not involve technology transfer (as of January 1, 2002). In the case of computer programs, the tax shall only be levied in case of transfer of technology (as of January 1, 2006).

10 For taxable events as of January 1, 2009 up to December 31, 2013 the tax credit is of 30%.

11 Although Brazilian Superior Court has decided that IPVA is not due on the ownership of aircraft and boats, but only on land vehicles ownership, some States are still charging this tax on these vehicles and the taxpayers should discuss the matter in Courts.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.