- within Employment and HR topic(s)

- with readers working within the Retail & Leisure industries

- within International Law, Media, Telecoms, IT, Entertainment and Corporate/Commercial Law topic(s)

- with Finance and Tax Executives

Pension in the oil and gas (upstream) sector is a bubble that may burst, if nothing is done to address the issue of escalating liabilities. The only question is: when? Given the high remuneration level and salary escalation rate of about 20%1per annum, the growing gap between pension liabilities and funding, presents an immediate concern. It is becoming clear that the continuous upward trend in pension costs is not sustainable. The issue, therefore, is how and when this matter will be addressed.

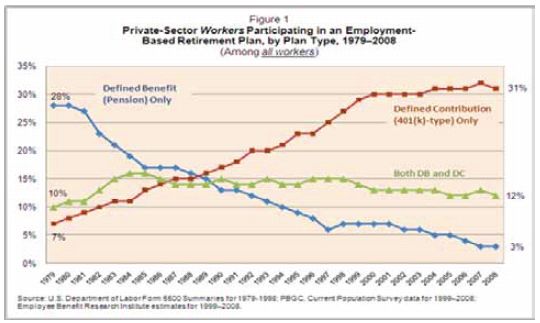

Pension in the International Oil Companies is predominantly defined benefits (DB) in nature, a type of scheme that is fast losing popularity around the globe, due to the high cost of funding, as shown below2.

In a DB plan, the amount of pension to be paid in retirement is defined in advance, usually with reference to the employee's salary at exit and qualifying years of service. The risk that contributions and returns on invested funds may not meet future pension obligations rests entirely on the employer, who must worry about funding any deficit. After the enactment of the Pension Reform Act of 2004 (PRA), most of the companies chose to manage their DB schemes as closed PFAs, given the size of the accumulated fund.

The other type of pension plan, common in other sectors in Nigeria, is Defined Contributions (DC). In this scheme, it is the rate of contribution that is defined and the employer's obligation ends with making the required contribution. Investment risk is, therefore, entirely borne by the employee, who is not sure if the accumulated fund would be sufficient to provide a fair level of income in retirement. 90%, if not more, of pension plans in Nigeria are DC plans. This scheme poses no issues except the safety of contributions and investment risk for the employee.

It is, therefore, important to understand the key aspects of DB plans that drive up pension liabilities. These include life expectancy, salary escalation rate, investment returns, attrition rate, staff population growth rate etc. Of all these, salary escalation is perhaps the strongest of the drivers. It is also one over which the employer has the most control. Salary escalation is an issue because the increases awarded fully impact pensionable salary items, which ultimately drive up pension benefits. On average, annual salary escalation is about 20% of Annual Basic Salary. To appreciate the strength of this variable, it is instructive to note that an increase of 1% in pensionable salary can have a significant multiplier effect on pension obligations. Based on our experience and knowledge of the market, pension liability accelerates more rapidly than changes in pensionable salary.

Given the unionised nature of the Industry, whereby employee unions wield a strong influence on the smooth running of company operations, the question is how much control do the companies have on salary increases?

The key to managing this issue, without causing unnecessary disagreement with the unions, therefore, lies in awarding increases in such a way that pension cost is managed.

Companies need to explore the possibility of channelling increases to those pay items that do not form part of pensionable salary. This way, the employee takes home a higher salary every year and the company is able to manage its pension costs. For this to succeed, companies need to engage with their employees and union members to secure their buy-in.

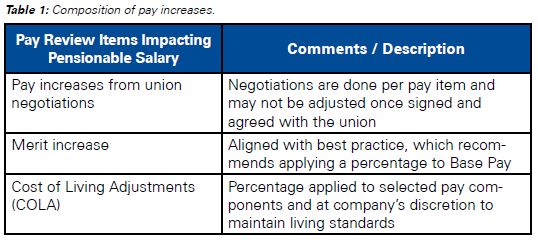

Given the type of increases granted, as shown in Table 1 below, the only window for executing this strategy is via cost of living adjustment (COLA) as a separate pay item.

In changing the way COLA is delivered, the questions to answer are: by how much is pension liability expected to slow down, what is the impact on the employee's total package and external competitiveness, and how and what should the new pay item to replace COLA be?

Another approach is to deliver all pay reviews with reference to the same Annual Basic Salary before the increases, rather than as compounded increases on one another.

Alternatively, a company can consider an overhaul of the scheme, whereby it defines new pension scheme rules and the amount of pension payable. Also, the company can freeze the scheme to new entrants, grandfathering existing members.

Perhaps, the second most critical driver of pension cost is life expectancy. Globally, the average person is living longer than before. The average life expectancy of a retiree (post-retirement) in the oil majors is about 15 years. This gives an indication of how long the scheme member will live to recieve pension benefits. If this is combined with the normal retirement age of 60 years, the total life expectancy can be as high as 75 years, as against 51.9 years3 , for an average Nigerian.

One way the developed and other countries have managed this is to increase retirement age. With a higher retirement age, the scheme has more time to invest funds before beginning to pay out pensions. Overall, increasing retirement age leads to a potential drop in future pension liability. The question is can a Nigerian company increase retirement age, without the required legislative amendments?

The other factors that are important to note are investment returns, attrition rate, staff strength etc. Return on Investment is a function of the investment vehicles allowed by the Pension Commission (PENCOM). Most of the funds are invested in government and private- sector bonds, with an average return of between 12% – 15% (based on typical actuarial assumptions for valuing the schemes). With the general bearish trend in the stock market over the past year, overall returns on fund assets may remain moderate over time. Attrition rate can be as low as 1%. The implication is that almost all employees will work till retirement. Given the salary escalation rate and life expectancy in retirement, the overall implication, when combined with long years of service, is higher pension cost for companies.

There is no doubt that managing pension cost has become a very big issue in the industry. Doing nothing does not wish the problem away. Companies need to act fast to address this issue. They need to evaluate the impact of continued increases in pensionable salary on pension costs and begin to engage employees on managing the growing liabilities. They may also want to explore the possibility of transforming the existing scheme into a defined contribution scheme as it has been done in many countries. This exercise may be extended to gratuity schemes since they are also DB schemes.

Footnotes

1 A typical composition of increases is 5% COLA, 5% Merit and 10% Union Negotiation

2 We expect the trend to remain the same as at today

3 Source: UNDP's Global Human Development Report, 2011

The opinion expressed in this article is solely personal and does not represent the views of any organization or association to which the authors belong.