- within Compliance topic(s)

ABSTRACT

On 22 September 2022; the third Tuesday of September the Dutch Budget Day Plan for 2022 was introduced by the government. This Budget Day Plan also consists out of the Tax plan 2022. In this plan new legislations and amendments have been added with regard to Direct taxed like the Corporate Income Tax Act and the Dividend Withholding Tax act. These amendments and legislations concern new CIT rates, ATAD2 legislation, mismatches in transfer pricing, CFC measures and loss offset rules.

Key words: CFC, Reversed Hybrid Mismatch, Carry Forward, Dutch Tax Plan 2022, Arm's Length Principle

INTRODUCTION

During the Dutch Budget Day 2022, on the third Tuesday of September, the Dutch parliament presented its Tax Plan 2022. Because the Netherlands currently has a caretaker government, there have not been many new or major decisions and changes with regard to taxes. This year there are mainly small(er) changes, which will improve the tax system. In particular, improvements are being made to the existing taxes in the areas of housing, work, green initiatives and business start-ups. This makes the Tax Plan 2022 package a lot smaller in policy terms than previous years, which is appropriate for the caretaker status of this government.

The tax plan does contain some interesting amendments that can have an effect-on-effect companies. These are predominantly amendments made in the Dutch Corporate Income Tax Act ("CITA").

In this article I will briefly discuss the following subjects: (i) CITA tax rates, (ii) the new reversed hybrid mismatch measure, (iii) the mismatches in price adjustments, (iv) the restrictions of advance tax deductions for Corporate Income Tax purposes (Sofina), (v) the order of loss offset in the case of CFC measure and finally (vi) the new loss offset rules in the CITA, followed by a conclusion.

CORPORATE INCOME TAX RATES 2022

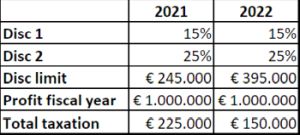

The below table shows current applicable CITA rates and the CITA rates becoming applicable in 2022.

Currently the tax rates in 2021 are a 15% tax rate on profit up to an amount of €245.000 . After that amount tax rate on profit is 25%. In 2022 the disc limit of disc 1 will increase; meaning that up to an amount of €395.000 profit will be charged with 15% and after that amount if will get charged with 25%. This is a beneficial development for companies that are subject under the CITA as it will effectively slightly lower their corporate income tax burden. For instance when a BV has a profit of €1 million at year end, then it is effectively taxed €225.000. Whereas if the same BV would make that profit in 2022 will effectively be taxed €150.000.

REVERSED HYBRID MISMATCH

Starting per January 1, 2022, the legislation regarding reversed hybrid mismatch situations shall be implemented in the CITA1, DWTA2 and the WHTA3. Hybrid mismatch regulation stems from the Anti-Tax Avoidance 2 (ATAD2) EU legislation. A Hybrid mismatch concerns situations in which different jurisdictions classify an entity differently, where one jurisdiction classifies a company as transparent while another considers the same company as non-transparent with different fiscal treatment as result. Hybrid mismatches allow companies to deduct a payment (e.g. interest) from their taxes in one country without it being taxed in another, or deduct one payment in multiple countries. The reverse-hybrid measure aims to tackle the hybrid mismatch at the source by making the hybrid entity subject to tax4. Effectively, a reverse hybrid entity will become subject to Dutch corporate income tax only to the extent that the profit is attributable to related participants that qualify the entity as non-transparent. The general rule is that a deduction in one country may not lead to an exemption in another country.

A common situation in which a reverse hybrid mismatch can occur is the infamous CV/ BV structure and it's tax implications in the Dutch CITA. In these structures a Dutch CV is often held by US companies. The CV in turn holds the shares in a BV. For US legislation the CV is non-transparent and for Dutch legislation the CV is transparent and therefore not subjected to the CITA. To elaborate:

- When BV would distribute a benefit to CV, from a Dutch perspective the BV would distribute these benefits to the US shareholders of CV and attributes these benefits to the US shareholders.

- But from an US scop,e BV is distributing these benefits to CV. And therefore the US attributes these benefits to CV and not to the US shareholders.

- CV is not established in the U.S. and therefore is not subject to the tax there.

- If BV makes a payment to CV, the above leads to the fact that - by applying the current hybrid mismatch measures in the CITA- that the payment made by BV is excluded from deduction because it is a so-called deduction without inclusion in the tax base of the receiver (CV).

With the new reversed hybrid mismatch regulation the CV as the receiver will get applied the reversed hybrid mismatch tax measure in which the Netherlands classifies the CV to be non-transparent and therefore independently liable to tax. As a result, CV's profits are integrally taxed in the Netherlands. However, to the extent that the CV's profits accrue to participants that are resident in a State that the CV considers transparent, a deduction will be granted for this when determining the CV's profit.

MISMATCHES IN PRICE ADJUSTMENTS

In addition, separate from the Tax Plan 2022, another bill has been sent to the House of Representatives to address mismatches to be implemented from January 1, 2022. Within a group of companies (transactions between related entities), business dealings with each other must be just as professional as independent parties would do under comparable circumstances (also known as the business principle (In Dutch: "het zakelijkheidsbeginsel")5. This is required on the basis of the arm's length principle. But because countries apply that principle differently or not at all, differences ('mismatches') may arise in international situations, resulting either in part of the profits of a group not being taxed anywhere, being taxed lower or a situation of double non-taxation". In such a situation, the measures in the proposal limit the downward adjustment of the profit taxable in the Netherlands at the taxpayer's expense. This measure is intended to neutralize transfer pricing differences and to avoid situations in which double non-taxation may occur.

For example if a BV does not pay an interest to a related entity - in this situation the related entity is A Co that is established in EU country 1 ("EU1") - in regard to a loan with 0% interest, but BV does have the right to deduct an at Arm's length interest rate of 5%. And in EU1 there is not a corresponding adjustment of 5% interest income at the level of A Co for taxation purposes, then BV will be denied the right to deduct the 5% (unpaid) interest in its CIT to neutralize the tax benefit that arises in such a situation for BV.

RESTRICTIONS OF ADVANCE TAX DEDUCTIONS FOR CORPORATE INCOME TAX PURPOSES (SOFINA)

It has been proposed to limit the possibilities for taxpayers to offset dividend tax and tax on games of chance (advance levy) against corporate income tax as of January 1, 2022, after the Sofina case6.

Under the main rule of the proposed measure, the set-off of withholding taxes will be limited to the amount of corporate income tax payable before the set-off of withholding taxes has been taken into account . This applies to all entities subject to CIT.

Under current Dutch legislation, both portfolio shareholders resident in the Netherlands and portfolio shareholders resident abroad pay dividend tax on profit distributions by Dutch-based entities. Portfolio shareholders resident in the Netherlands who are liable for CIT (taxpayers) can always offset the dividend withholding tax against CIT, so that on balance they only pay CIT on the portfolio dividend. If they are loss-making or otherwise do not owe CIT, the taxpayers get a full refund of the dividend tax levied. Foreign loss-making portfolio shareholders (foreign entities), on the other hand, do not have this option. This legislation neutralizes the fiscal benefit that portfolio shareholders resident in the Netherlands currently have compared to the foreign portfolio shareholders. In other words, the Dutch portfolio will lose these benefits.

In short, under the proposed measures, the crediting of withholding taxes will only be limited with respect to taxpayers who:

- Are not in a position where CIT is due because those taxpayers are loss-making or entitled to statutory deductions or double taxation relief; or

- Are in a position to pay CIT, but the amount they have to pay is lower than the amount of withholding taxes levied; and

- Pay gambling tax because a game of chance has been won as part of the company's activities; or

- Hold an equity interest of less than 5% in an entity established in the Netherlands that is liable to withhold dividend tax. Also if the dividend withholding tax exemption is not applied to an interest of 5% or more of the taxpayer in an entity established in the Netherlands which is liable to withhold dividend tax is liable to withhold dividend tax, there may be dividend tax levied of which the set-off is limited in time.

THE ORDER OF LOSS OFFSET IN THE CASE OF CFC MEASURE

CFC legislation (CFC stands for Controlled Foreign Company) is tax legislation aimed at preventing Dutch taxpayers from having their income deposited in letterbox companies abroad, particularly in tax havens. It is anti-abuse legislation, particularly in the area of corporate income tax. CFC legislation taxes this income on the shareholder, even if no dividend has been paid.

The current Dutch CFC legislation is laid down in art. 13a of the VPB 1969 Act. Pursuant to art. 13a VPB 1969, a taxpayer is, under certain circumstances, required to annually value its interest in a subsidiary at fair value (revaluation obligation). As a result, the result of the subsidiary will be subject to corporate income tax of the parent company before any profit distributions have taken place or any disposal benefit has been realized, and both the rate and deferral benefit associated with the use of a CFC will be lost. From January 1, 2022, a new measure is implemented7. This new measure establishes a mandatory foreign profit tax credit sequence for a CFC entity. Until now, you could choose what part of the tax was settled in one year and what part you wanted to defer to future years. The measure starting January 1, 2022, dictates in what order foreign profits taxes can be offset, if the parent company has more than one CFC. The measure entails a mandatory order to set off the foreign taxes by first setting off the lowest amount, followed by the increasing amounts. If the amounts to be set off are identical, both amounts should be considered for a proportionate amount.

NEW CITA LOSS OFFSET RULES IN THE CITA

Starting from January 1, 20228, new los offset rules apply in the CITA for companies. There will be a broadening that means that losses can be carried forward indefinitely. In addition, a restriction will be introduced whereby losses are only fully deductible up to an amount of € 1 million. To the extent that a loss exceeds the amount of € 1 million, only 50% of the loss is deductible. The backward loss relief is limited to the previous year. The limitation for losses above an amount of € 1 million also applies to the backward loss relief. The amendments apply to losses from financial years commencing on or after January 1, 2013, to the extent that these losses are set off against taxable profits from financial years commencing on or after January 1, 2022.

CONCLUSION

Even though at first glance it may not seem as though there are very big changes to the Dutch tax system this year. The changes with respect to Dutch direct taxes are significant and do carry substantial changes with it. The reversed hybrid now fully dismantles the benefits that were once present with structures like the CV/BV structure. The measure to combat mismatches in regard to price adjustments will force international groups to reconsider their 0% loans that they have with their Dutch entities. The new measures due to the Sofina Case will impact Dutch residents that once has a fiscal benefit. And the new rules for the carry forward loss will require a significant tax asset management by a group's treasury department. We can imagine that these new measures and amendments are a lot to take in. Therefore we are glad to be of assistance.

Footnotes

1. Dutch Corporate Income Tax Act

2. Dutch Dividend Withholding tax Act

3. Dutch Withholding Tax Act

4. Rijksoverheid. (2021, 22 september). Memorie van toelichting wetsvoorstel Wet implementatie belastingplichtmaatregel uit de tweede EU-richtlijn antibelastingontwijking.

5. Ministerie van Algemene Zaken. (2021, 22 september). Wetsvoorstel Wet tegengaan mismatches bij toepassing zakelijkheidsbeginsel. Kamerstuk | Rijksoverheid.nl. https://www.rijksoverheid.nl/documenten/kamerstukken/2021/09/21/wetsvoorstel-wet-tegengaan-mismatches-bij-toepassing-zakelijkheidsbeginsel

6. Ministerie van Algemene Zaken. (2021, september 20). Memorie van toelichting Belastingplan 2022. Kamerstuk, Chapter 13, page 19 | Rijksoverheid.nl. https://www.rijksoverheid.nl/documenten/kamerstukken/2021/09/21/memorie-van-toelichting-belastingplan-2022

7. Staatssecretaris van Financiën. (2021, september 20). Wijziging van enkele belastingwetten en enige andere wetten (Overige fiscale maatregelen 2022) Memorie van toelichting. Kamerstuk, Chapter 8, page 20 | Rijksoverheid.nl.

8. Rozendal, A. (2021, 4 October). Verliesverrekening in de Vennootschapsbelasting. Navigator.nl. https://www.navigator.nl/thema/1090/verliesverrekening-in-de-vennootschapsbelasting#:%7E:text=Vanaf%201%20januari%202022%20worden,1%20miljoen%20volledig%20verrekenbaar%20zijn.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]