- within Real Estate and Construction and Family and Matrimonial topic(s)

- in United Kingdom

- with readers working within the Aerospace & Defence industries

For U.S. tax purposes, gain or loss upon a sale or exchange of property is generally sourced based on the tax home of the seller. For a foreign person investing in a partnership conducting a U.S. trade or business ("specified partnership"), it is important to keep in mind that when at some later date she sells or otherwise disposes of the investment, and no matter where she resides, she will be subject to tax on gain deemed to be effectively connected with a U.S. trade or business.

Code §864(c)(4), added by the Tax Cuts and Jobs Act of 2017 ("T.C.J.A."), and repealing the holding of the Grecian Magnesite case,1 recharacterizes a sale of a partnership interest as a sale of partnership assets, resulting in gain to the selling foreign partner. Under Code §1446(f), withholding tax of 10% applies to the seller's amount realized.

I.R.S. Regulations adopted in 2020 address sales and comparable transactions by non-U.S. persons of direct and indirect interests in a U.S. partnership. Final regulations under Code §1446(f) (T.D. 9926) provide the mechanical rules for withholding by transferees (acquirers) and follow up on previously released guidance under Code §864(c)(8) (T.D. 9919) which contained substantive rules. In short, the acquirer or transferee of the partnership interest is required to deduct and withhold 10% of the gross purchase price. Foreign partners in partnerships with U.S. fixed offices and U.S. trades or businesses will want to master these rules and exceptions.

BACKGROUND

The statutory enactment of Code §§864(c)(8) and 1446(f) could be viewed as the final word by the I.R.S. in a long-standing, heated back-and-forth conversation.

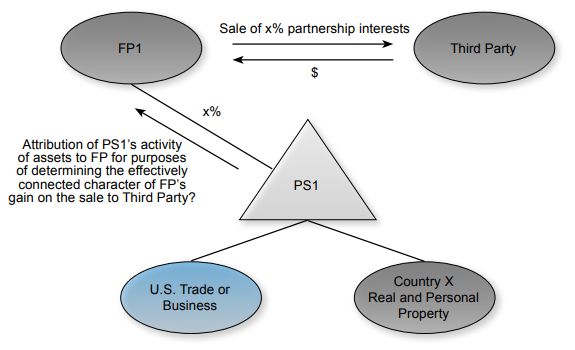

In Rev. Rul. 91-32, 1991-1 C.B. 107, a foreign partner ("FP1") in partnership PS1, sold its interests for cash, as depicted below.

Rev. Rul. 91-32 (Situation 1)

Concluding that for treaty purposes a portion of the resulting gain

relating to FP1's partnership interests should be treated as

E.C.I. attributable to a U.S. permanent establishment

("P.E."),2 the I.R.S. could not rely on Code

§864(c)(8) (which did not exist) so it analogized based on

rules like Code §875(1).3

This was followed by an important Tax Notes article six years later, criticizing the ruling and arguing that it should be set aside;4 a 2017 Tax Court case, Grecian Magnesite refusing to follow the ruling as "cursory in the extreme" (affirmed by the D.C. Circuit Court of Appeals); and the 2017 legislative enactment repealing Grecian Magnesite and providing a statutory basis for the I.R.S. position.

Effectively Connected Income

A foreign person engaged in a trade or business in the United States is taxed on income effectively connected with that conduct of the trade or business ("E.C.I."). Partners are treated as engaged in the conduct of a business if the partnership is so engaged.5 A U.S. trade or business exists for each year that a foreign person engages in "considerable, continuous, and regular" activity in the U.S.6 Tests are applied to determine whether income, gain or loss is effectively connected with assets used in that trade or business ("asset use test"), or activities of the business were a material income-producing factor ("business activities test"). Code §865(e) treats gain on the sale of personal property attributable to a U.S. office as U.S. source unless a foreign office materially participated in the sale (the "U.S. office rule").

The new regime does not change these rules, nor create a new rule of income recognition; rather it simply recharacterizes the sale of partnership interests as a disposition of assets. The recharacterization requires facts-and-circumstances rules like the above to be applied to a fictional sale. The Regulations explain how.

FINAL REGULATIONS

T.D. 9919 - Substantive Rules under §864(c)(8)

Final regulations under Treas. Reg. §1.864(c)(8)-1 determine the disposing partner's effectively connected gain or loss or "aggregate deemed sale E.C.I." ("A.D.S.E.C.").

The Regulations address how the deemed sale is to be analyzed for the business activities test or U.S. office rule, where no actual sale takes place and include special rules for inventory,7 intangibles, and other property. Modified sourcing rules apply. The partner's distributive share of A.D.S.E.C. may vary based on the partners' agreement. Special rules apply to publicly traded partnerships. This article focuses on non-publicly traded partnerships.

It is important to note that if a partnership distribution results in gain recognition, these new rules may be implicated.

T.D. 9926 - Withholding of 10% Tax under §1446(f)

The Regulations under T.D. 9926 address the numerous practical matters relating to a sale of partnership interests, including required notifications (see end of this article). If the transferor is a U.S. person and provides Form W-9, then 10% withholding is inapplicable. Otherwise, the transferee must withhold 10% of the amount realized and submit the same to the I.R.S. unless an exception or adjustment applies.

Exceptions include the following cases:

- The transferor certifies non-foreign status.

- The transferor certifies that no gain, including ordinary income from deemed sales of "hot assets", will be realized by reason of the transfer.

- The transferor certifies that gain will not be recognized because the transaction is a nonrecognition exchange, or that the provisions of a tax treaty apply.

- The transferor certifies that during a prescribed look-back period the transferor was a partner throughout such period, and that the transferor's distributive share of gross E.C.I. was less than $1 million and less than 10% of the transferor's total distributive share of gross income (and that other technical requirements are satisfied).

- The partnership certifies that effectively connected gain is less than 10% of the total net gain inherent in its assets.

- The partnership certifies that based on partnership allocations, the transferor would be allocated E.C.I. equal to less than 10% of the total amount allocable.

- The partnership certifies it was never engaged in a U.S. trade or business.

To view the full article, please click here.

Footnotes

1. Grecian Magnesite Mining, Indus. & Shipping Co. v. Commr., 149 T.C. 63 (2017), aff'd, 926 F.3d 819 (D.C. Cir. 2019).

2. The P.E. question is addressed in Situation 3.

3. Code §875(1) provides that "a nonresident alien individual or foreign corporation shall be considered as being engaged in a trade or business within the United States if the partnership of which such individual or corporation is a member is so engaged." Also see Donroy, Ltd. v. U.S., 301 F.2d 200 (9th Cir. 1962).

4. Kimberly Blanchard, "IRS Rev. Rul. 91-32: Extrastatutory Attribution of Partnership Activities to Partners," Tax Notes, Sept. 14, 1997.

5. Code §875.

6. For example, see Pinchot v. Commr., 113 F.2d 718 (2d Cir. 1940).

7. Historical sales data is used to determine the transferor's A.D.S.E.C.

Originally Published 27 May 2021

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.