- in United States

- with readers working within the Law Firm industries

- within Transport topic(s)

Stock Market Commentary

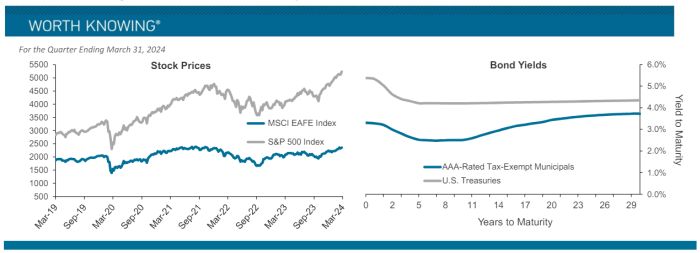

Following a strong end to 2023, U.S. stocks continued their climb through the first quarter of 2024. In the first 50 trading days of the year, the S&P 500 Index had 17 all-time closing highs—the most for the start of a year since 1998. Though the positive performance broadened out some from artificial intelligence–related hype, it was still led by a handful of large companies, with Nvidia, Microsoft, Meta, and Amazon each contributing over 0.5% to the index's positive 10.6% return for the quarter. The communications, energy, and technology sectors were up the most, while interest rate–sensitive sectors such as utilities and real estate struggled as investors believed rates may need to remain higher for longer to combat a recent uptick in inflation.

International markets were positive as well. The MSCI EAFE Index, which tracks the performance of equity markets in developed countries outside of the United States and Canada, returned 5.9% for the quarter. Japan's major stock market index, the Nikkei 225, reached a new high for the first time in nearly 35 years, despite that country's economy almost falling into a recession.

The MSCI Emerging Markets Index eked out a 2.4% gain, as Chinese stocks saw a modest rally. So far, the Chinese government has not employed strong stimulus to help their faltering economy, and the valuation discount between Chinese stocks and their global peers remains near record levels.

Bond Market Commentary

After robust returns in the last quarter of 2023, fixed-income markets were relatively flat in the first quarter of 2024. The Bloomberg US Aggregate Bond Index was down 0.78%, while high-yield bonds were up 1.47%.

Inflation remained the primary concern for many central banks. Switzerland unexpectedly cut its key interest rate in March, becoming the first advanced economy to make such a move. EU, UK and Canada held rates steady in the first quarter of 2024. All three countries indicated they would lower their key interest rates as early as the second quarter. Not all countries desired lower inflation, however. Japan, which had inflation well below its 2% target for years, embraced higher inflation after years of deflation. In March, Japan increased its key rate to at least zero, ending its negative interest rate policy after eight years.

In the U.S., the Federal Reserve maintained its current fed funds rate, although Fed Chair Jerome Powell also reaffirmed projections for cuts later this year. A high fed funds rate means attractive yields, especially for short-term bond investors. The return for 3-month U.S. Treasury Bonds remained at the highest level in the past 23 years, yielding 5.36% at the end of the first quarter.

Economic Commentary

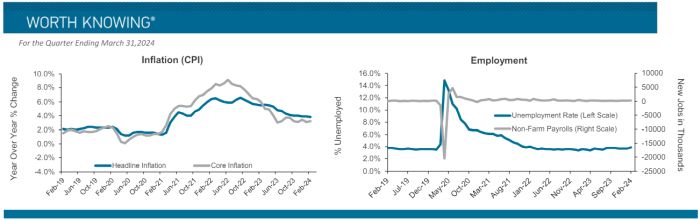

Economic growth in the U.S. remained robust during the first quarter of 2024 even as the Federal Reserve kept a watchful eye for signs of a slowdown in the face of restrictive monetary policy.

Historically, high interest rates eventually lead to lower inflation through lower growth and higher unemployment. During this economic cycle, however, inflation appears to be falling toward the target levels without the correlating economic slowdown. While it may not be time to declare a victory lap for the Fed's "soft landing" just yet, it does appear as if the central bank's policy goals are within reach with minimal economic harm realized thus far.

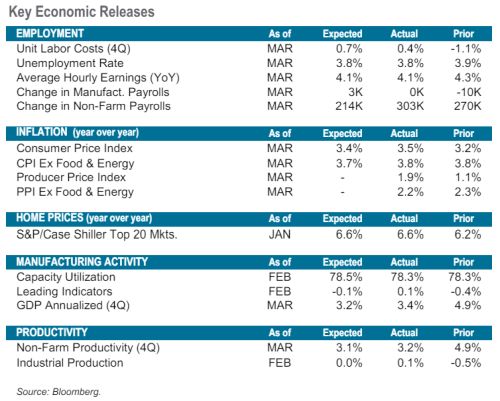

Consumer sentiment is rising, new home sales are steady, existing home sales are picking up, and unemployment, while rising at the margin, is still at a low 3.8%. The Consumer Price Index rose slightly to 3.5% in March from 3.2% in Febuary, primarily due to increased gasoline prices and airfares, but the Fed indicated no ongoing concern about these increases when giving comments to Congress in early March.

As Fed Chair Powell testified on Capitol Hill, "We believe that our policy rate is likely at its peak for this tightening cycle." We agree, but we see the possibility for rates to remain "higher for longer" this cycle while still anticipating a rate cut before year end.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]