Key Points:

- On Wednesday, March 6, 2024, the SEC in a 3-2 vote adopted "The Enhancement and Standardization of Climate-Related Disclosures for Investors" (Final Rule). The Final Rule will require public companies to disclose certain climate-related information in their registration statements and annual reports. The Final Rule is intended to enhance and standardize certain climate-related disclosures in order to address stakeholder demands for more consistent, comparable and reliable information about the financial effects of climate-related risks and how companies manage such risks.

- The Final Rule reflects the Biden administration's whole of government approach to the U.S. government's response to climate change, leveraging, in this instance, the SEC's rulemaking authority to improve transparency significantly around climate risks and claims.

- This Alert summarizes the Final Rule, identifies criticisms and potential legal challenges and offers recommendations on how to prepare for the new disclosure requirements.

Summary

Modeled in part upon the Task Force on Climate-Related Financial Disclosures (TCFD)1 disclosure framework, bound by materiality as a general threshold for the requirements, the Final Rule requires disclosure of the following topics.

- Governance: Describe the board's and management's oversight and governance of material climate-related risks.

- Strategy: Disclose the material impact or reasonably likely material impact of identified climate-related risks on strategy, results of operations or financial condition.

- Risk Management: Describe the processes for identifying, assessing and managing material climate-related risks, and any integration into overall risk management.

- Targets and Goals: Disclose any material climate-related targets or goals and their material impact or reasonably likely material impact, including (1) the scope of activities included in the targets and the time horizon for achieving such targets, (2) how such targets or goals are intended to be met and (3) any progress made toward the targets or goals, with annual updates.

- GHG Emissions Metrics: To the extent determined to be material, large accelerated filers and accelerated filers will be required to separately disclose direct greenhouse gases (GHG) emissions (Scope 1) and/or indirect GHG emissions from purchased electricity and other forms of energy (Scope 2), expressed both by disaggregated constituent GHG emissions and in the aggregate. Notably, the U.S. Securities and Exchange Commission (SEC) elected to omit from the Final Rule a requirement that a company also disclose indirect emissions from upstream and downstream activities in such company's value chain (i.e., Scope 3 emissions information). Omission of the Scope 3 disclosure requirement represents a departure from the disclosure rule, as proposed, as well as a deviation from climate disclosure rules adopted by European regulators and the suite of climate disclosure legislation enacted by the state of California.

- Attestation of Scope 1 and Scope 2 Emissions Disclosure: Provide, if required to provide GHG emissions disclosures, an attestation report from a qualified outside service provider covering, at a minimum, the disclosure of Scope 1 and Scope 2 GHG emissions and certain related disclosures about the service provider.

- Carbon Offsets: Disclose information about the use of any carbon offsets or renewable energy certificates (RECs) used as a material component of a company's plan in achieving its climate-related targets or goals.

- Financial Statement Metrics: Provide climate-related financial statement metrics and related disclosure in a note to the company's audited financial statements.

Climate-related disclosures under the Final Rule, both narrative and quantitative in form, are to be tagged in Inline XBRL and will be filed rather than furnished. A more fulsome description of the Final Rule is set forth below.

The Final Rule will go into effect 60 days after publication in the Federal Register, and compliance will be phased in as described below.

Comments

In its adopting release, the SEC acknowledged the "extensive public comments" it received in relation to the proposed rule, noting that the agency received "over 4,500 unique comment letters...and over 18,000 form letters." Such comments were received from a broadly-based set of stakeholders, including "academics, accounting and audit firms, individuals, industry groups, investor groups, law firms, non-governmental organizations, pension funds, professional climate advisors, professional investment advisers and investment management companies, registrants, standard-setters, state government officials, and U.S. Senators and Members of the House of Representatives." The SEC also pointed out that each of its Investor Advisory Committee and Small Business Capital Formation Advisory Committee recommended modifications to the disclosure rules, as proposed, and that the Final Rule reflects modifications that "better effectuate our goals in requiring these additional disclosures while limiting the final rules' burdens on registrants."

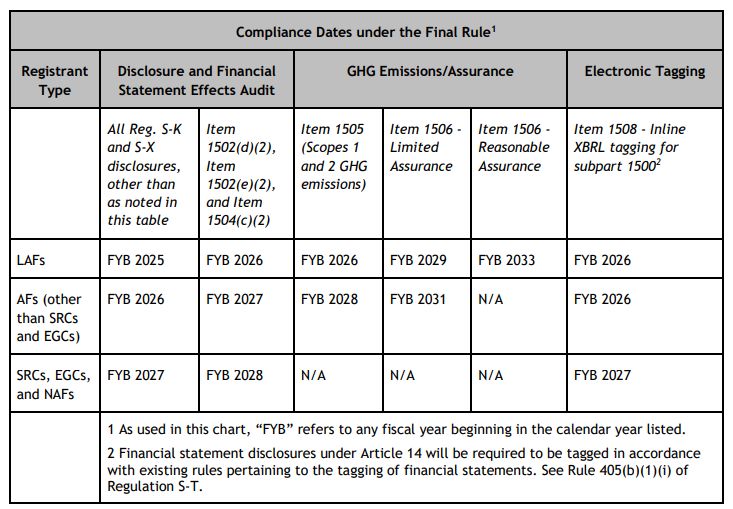

Compliance

The following table sets forth compliance deadlines:

LAF—Large Accelerated Filer

AF—Accelerated Filer

NAF—Non-Accelerated Filer

SRC—Smaller Reporting Company

EGC—Emerging Growth Company

To view the full article, click here.

Footnote

1. The SEC in the adopting release refers to recent rulemaking initiatives by foreign and state regulatory authorities in relation to the disclosure of climate related risks, including announcements by several countries of their intention to adopt laws or regulations implementing climate reporting standards developed by the International Sustainability Standards Board (which we wrote about here) and climate-related disclosures requirements enacted by the state of California (which we wrote about here). We note that California's climate-disclosure rules are currently subject to challenge in federal court

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.