Introduction:

Recent statements from the Prime Minister announced forthcoming changes to company size classifications, promising to streamline reporting obligations for businesses nationwide. These adjustments, stated to take effect later this year, aim to simplify both non-financial and financial reporting processes for Small and Medium Enterprises (SMEs), aligning with evolving post-Brexit regulatory freedoms.

Key Developments:

As of March 18, 2024, the government revealed plans for significant deregulatory measures, including a noteworthy 50% increase in the thresholds dictating company sizes. This adjustment is poised to redefine the classification of a substantial number of businesses, potentially granting relief to around 132,000 entities by alleviating certain non-financial reporting burdens.

Proposed Changes:

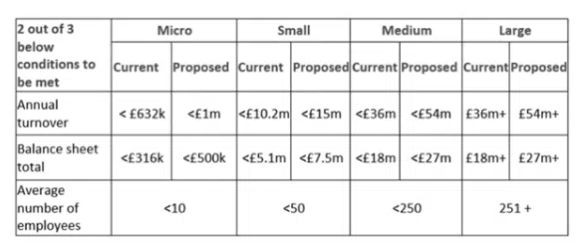

The proposed modifications to company size thresholds, stated for implementation for financial years starting October 1, 2024, are summarised in the table below:

Additionally, governmental initiatives will:

- Streamline reporting obligations by eliminating redundant or outdated requirements from the Directors' Report and the Directors' Remuneration Report and Policy.

- Facilitate the transition to digital annual reports for companies.

- Address technical intricacies in the audit regulatory framework stemming from the integration of EU law into UK legislation.

Future Considerations:

Looking forward, the government plans to further engage in consultations regarding additional measures, with a particular focus on medium-sized companies. These discussions may encompass exemptions from producing strategic reports and potential adjustments to the employee size threshold, possibly raising it from 250 to 500 employees.

Conclusion:

The forthcoming adjustments to company size classifications underscore the UK government's proactive stance in fostering a regulatory environment conducive to business growth post-Brexit. By simplifying reporting requirements and alleviating administrative burdens, these measures aim to bolster the resilience and prosperity of SMEs while ensuring regulatory compliance. As businesses brace for these impending changes, staying informed about updates and guidance will be paramount for navigating the evolving regulatory landscape effectively.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

We operate a free-to-view policy, asking only that you register in order to read all of our content. Please login or register to view the rest of this article.