CBN Bank recapitalisation

Highlights

- We anticipate that the move by the CBN will enhance the stability and capacity of the banking industry as well as attract greater investments to the sector.

- The new capital requirement as defined by the CBN has triggered a call to action by ALL banks who are impacted to different degrees.

- Data suggests a significant capital shortfall of N4.2 trillion across all license categories, with available options for banks including capital raise (as much as between 35% - 90% of the new minimum capital); mergers and/or acquisitions; and the downgrade of license authorisations.

- We recommend a proactive monitoring of market dynamics to identify and address any systemic risks or disruptions that may arise during the recapitalisation phase to preserve the stability of the financial system.

Event

The Central Bank of Nigeria (CBN) recently announced an increase in capital requirements for banks operating in Nigeria across the different license categories. An integral part of the announcement is the definition of minimum capital to include only paid-up capital and share premium, thereby excluding the industry's significant retained earnings reserves as well as other forms of capital.

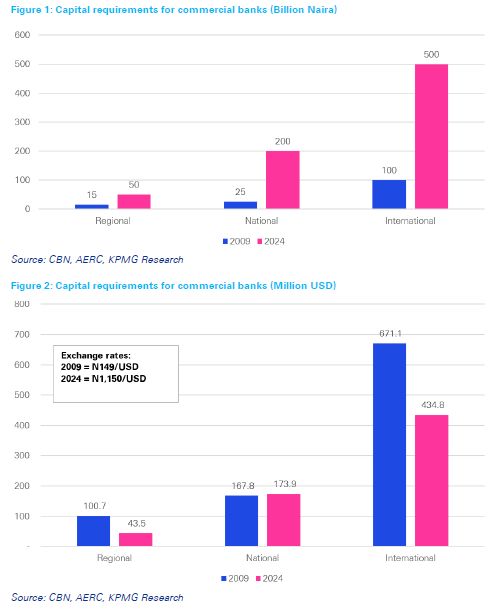

CBN Capital Requirements by License Category

|

Banks |

Coverage/Scope |

Capital requirements (N'Billion) |

|

Commercial |

International National Regional |

500 200 50 |

|

Merchant |

National |

50 |

|

Non-interest |

National Regional |

50 10 |

The increase in capital requirement by the CBN is aimed at strengthening the resilience of the banking industry to withstand challenges arising from global and domestic headwinds. The higher capital requirement will enhance financial system stability as banks become better positioned to absorb financial shocks or unexpected losses. In addition, the upward adjustment will help boost investor confidence in the banking system as investors tend to perceive well-capitalised banking systems as being 'too big to fall'.

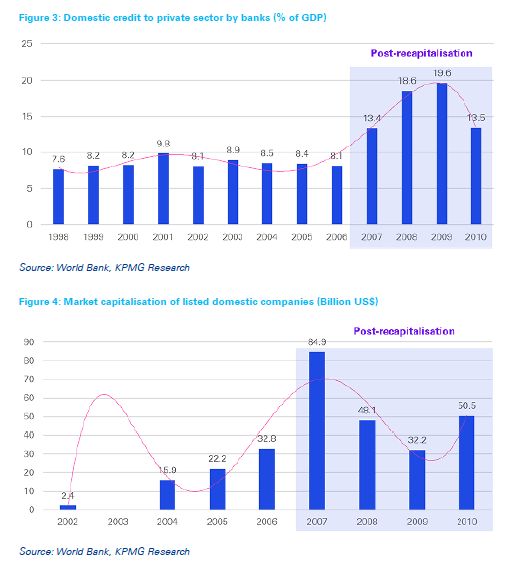

The last banking sector reform introduced by the CBN in 2004 led to a significant 1,150% increase in the minimum capital requirement for banks, from N2 billion to N25 billion.

The reform was marked by extensive M&As, leading to a notable reduction in the number of deposit money banks in the country from 89 to 25.

Consequently, banks were better positioned for financial intermediation to support economic growth and development. Bank credits to private sector as a ratio of GDP rose to as high as 19.6% in 2009 when banks were allowed to operate as regional, national and international banks while market capitalisation increased to about $85bn in the immediate periods following the last bank recapitalisation in 2004.

With the current reform agenda, the stringent definition of minimum capital which has left significant reserves unavailable for capitalisation, is driving a widespread impact on the banking industry with changes to the competitive landscape expected as a fallout. The capital shortfall for banks ranges between 35% to 90% of the new minimum capital requirement, with an estimated total capital shortfall of about N4.2 trillion across the entire industry.

Several options are available to banks in their effort to raise additional capital, a route we anticipate to be the first line of action for most banks in achieving the new capital requirement, and these include public offerings, rights issues, private placements, etc. However, consideration for potentially value accreting mergers and acquisitions as an alternative option may prove invaluable for players who adopt a broad-based approach to the reform.

In conclusion, we welcome the recapitalisation of banks with optimism as it is necessary to enhance the resilience of the banking system and support the growth agenda of the economy through greater financial intermediation. However, we recommend a proactive monitoring of market dynamics to identify and address any systemic risks or disruptions that may arise during the recapitalisation phase to preserve the stability of the financial system.

The opinion expressed in this article is solely personal and does not represent the views of any organization or association to which the authors belong.

We operate a free-to-view policy, asking only that you register in order to read all of our content. Please login or register to view the rest of this article.