The Hon. Minister of Finance Prof. Edward Scicluna, presented his 2014 Budget speech on 4 November 2013. This publication highlights the key fiscal measures and latest economic statistics on the Maltese economy.

General overview

In his introduction to the 2014 Budget speech, the Hon. Minister of Finance Prof. Edward Scicluna declared that the basis of the 2014 Budget reflects the Government's promise to change the economic direction of the country towards one of sustainable development that will benefit all.

In order to achieve this goal, the Government laid out the first phase of its economic plan which was based on the following six priorities:

- That all expenses were to be incurred in accordance with the Government's overriding policy of expenses not being greater than what the country can afford;

- That the country's energy generation costs should be reduced;

- That the country's economic potential be increased, such that it may translate into an improved standard of living for all Maltese which is not less than that enjoyed by other Europeans. This Budget will as a result be focusing on the need to incentivise those currently not working to start doing so, in line with the principle of 'Making Work Pay';

- That waste and excessive red tape, which are costing the Government money and are stifling those who wish to contribute to economic growth and work, are reduced;

- That the country's economic activities are diversified and spread, not only geographically, but over all gainful areas of manufacture and services, so as not to be reliant on a few industries; and

- That all social services are placed on solid and sustainable foundations.

Economy and employment

The Maltese economy is expected to grow by 1.2% during 2013, with a projected growth of 1.7% in 2014. According to recent Eurostat statistics, the 6.4% Maltese unemployment rate ranks amongst the lowest within the EU, reflecting an economic growth of 3.6% in Q2 2013. Inflation rate up to September 2013 has reduced to 0.6% compared to 2.9% in September 2012.

Government finances

The total estimated Government revenue for 2013 is expected to reach €3,050 million (2012 - €2,716 million) while total expenditure is expected to be €3,230 million (2012 - €3,058 million). The 2014 projections indicate a total Government revenue of €3,273 million whilst the total expenses are expected to reach €3,409 million. The deficit to GDP ratio is estimated at 2.7% for 2013 and is projected to reduce to 2.1% during 2014.

Personal income tax

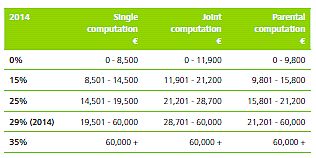

The plan to reduce overall income tax levels is being continued through an increase in the tax-free bracket to €9,800 in respect of parental rates and a reduction of the 32% tax bracket to 29% in 2014.

Dividends received will be taxable at the progressive tax rates applicable prior to the introduction of the 32% tax rate.

The qualifying age for children in tertiary education maintained by individuals benefitting from the parental computation is to be increased from 21 to 23 and the qualifying tertiary educational institutions are to be extended to other institutions such as MCAST and ITS.

Cost of Living Adjustment

The Cost of Living Adjustment for 2014 will be €3.49 per week. As a result, the minimum wage will increase from €162.19 to €165.68 per week. The necessary amendments to the tax law will be made to ensure that persons earning the minimum wage will not be subject to income tax.

As from 2014, the tax exemption will be extended to pensioners whose only income consists of a pension that does not exceed the equivalent of the minimum wage.

Water and electricity

The electoral pledge to reduce residential water and electricity tariffs will be implemented in March 2014. The price of electricity is to be reduced by an average of 25%, whilst the price of water is to be reduced by an average of 5%. Such a measure is to save families more than €25 million.

Water and electricity tariffs for businesses will be reduced in 2015.

Excise duty and other taxes

Measures have been announced for the revision of motor vehicle registration and licence fees, as well as excise duty on tobacco, fuel, cement and alcoholic beverages, and tax rates applicable to bunkering of fuels.

These measures are expected to generate an estimated increase in Government revenue of €21.4 million.

Transport

Refunds of car registration taxes

€3.5 million is being allocated in the 2014 Budget towards the granting of registration tax refunds to those who registered a vehicle for personal use between May 2004 and December 2008. The refunds will be effected over a seven year period.

Decrease in vehicle registration tax

A yet unquantified decrease in the registration tax of certain vehicles imported from outside the European Union, and which are not older than eight years and which have CO2 emissions not greater than 150g/km, is to be implemented.

The tax on the registration of motor cycles having an engine capacity of 250cc or more is to reduce by 25%.

Employment incentives

Income tax on part time employment

- The income ceiling on which the preferential tax rate of 15% is applied is to be extended from €7,000 to €10,000 in the case of part time employees, and from €7,000 to €12,000 in the case of part time self employed persons.

- Part time self employed business owners are to be allowed to employ up to two part time employees without losing their entitlement to the 15% preferential tax rate.

- Part time self employed pensioners will be eligible to apply the preferential tax rate of 15% on their income as long as such income would not exceed the minimum income on which they would pay the lowest rate of social security contributions.

- Footballers are to be taxed at a preferential rate of 7.5% on their part time income derived from the sport.

Incentives for working women over 40

As from next year, married women over 40 years of age who return to work after an absence of five years or more, and whose income will not exceed the minimum wage, will not be required to include their salary in the joint tax computation with their husbands'. This benefit should apply for a maximum period of five years and should translate in an annual tax saving of approximately €800.

Incentives for the employment of apprentices

This year's Budget sees the introduction of an incentive to employers to offer apprenticeships or work placements. A tax deduction of €600 for each work placement and of €1,200 for each apprenticeship offered is to be given to employers.

Benefits for single parents

Measures will be introduced to encourage single parents to enhance their employment prospects. Single parents in receipt of social benefits that opt to enrol for intensive vocational courses or full-time education will be granted a credit ranging from €200 to €1,000.

Incentives for the employment of middle aged persons

The Government plans to introduce incentives that will assist in the training and subsequent employment of unemployed persons aged between 45 and 65 through a reduction in income tax in the first two years of such person's employment. Furthermore, employers of such persons will be assisted by means of a reduction in tax equal to 50% of the training cost, capped at €400.

Incentives for those wishing to work

In line with this Government's 'Work Pays' philosophy, an incentive is being introduced so as to assist persons currently unemployed, in the transition towards a place into the work force. This incentive will mean that persons may still enjoy 65% of their unemployment benefits during their first year of employment, 45% during their second year, and 25% during their third year. Additionally, the employer will receive 25% of these benefits each year for three years.

Tax deduction for the use of child care centres

The current maximum tax deduction on fees paid for children attending child care centres will increase from €1,300 to €2,000.

Withholding tax on rent

In a drive to regularise the rental market, the Government is to introduce the option to landlords of residential property to be taxed at 15% on the gross rental income of such property. The Government has warned of greater enforcement in this sector and has declared a zero tolerance towards tax evasion. Any undeclared rental income will be subject to a final tax of 35% on the gross rental income, in addition to fines and penalties which would be imposed.

Investment Registration Scheme

An Investment Registration Scheme will be re-introduced. This will provide the opportunity for persons who have undeclared funds, stocks or investments, locally or overseas, to regularise their position through the scheme. Further details on this scheme should be announced shortly.

Fight against tax evasion

In the context of the fight against tax evasion, the Minister of Finance announced the introduction of a system to encourage persons who buy construction related services, to substantiate the estimated value of works carried out through presentation of receipts, failing which such persons may be liable to pay the VAT due thereon. No further details have been provided as to how this system will operate.

Online system for the reporting of abuse

A new online system will be introduced for reporting of illegal cases where foreigners working or operating in Malta do not adhere to fiscal or employment statutory obligations thus gaining unfair competitive advantage.

Duty on documents

Duty on sales by auction

Duty is currently payable at the rate of 2.6% on sales by auction of movables exceeding a value of €230. This duty is now being removed.

Capping of interest on causa mortis transmissions

Interest payable by heirs on late payment of duty arising upon causa mortis transmissions has now been capped such that the interest cannot exceed the amount of duty itself.

Duty exemption on first time property buyers

A reduced rate of duty of 3.5% is currently payable on the first €150,000 of the value of an immovable property intended to be used as, or to construct thereon, a person's sole, ordinary residence.

In order to incentivise first time buyers, the law will be amended such that during 2014, no duty will be payable on the first €150,000 of the value of an immovable property purchased by persons who never owned any immovable property, directly or indirectly, prior to 1 January 2014.

Government appointed architects

In the context of determining the duty payable on immovable property transfers, the tax authorities will start accepting valuations prepared by private architects. The necessary safeguards will however be introduced to curb any abuse.

Duty on property transmissions to persons with disability

The duty payable on bona fide transmissions causa mortis of immovable property will be removed where the transferee is a person with a disability. Currently, an exemption applies only where the property being transmitted consists of the deceased and the heir's ordinary residence.

Simplification in VAT rules

Under the current provisions in the VAT law, when a VAT registered person does not pay the VAT due on time, any subsequent payments are first allocated against interest and penalties, and then against the VAT due, starting from the older balances. This appropriation system results in current VAT balances remaining outstanding with further interest continuing to accumulate on such balances.

The VAT law will be changed such that, as from January 2014, when a VAT return is filed on time and the relative VAT is paid, such payment will be allocated against the VAT due on that VAT return, with the older balances, interest and penalties remaining outstanding.

Other similar changes to the VAT law will be made to ensure that payments are not allocated to VAT which is still being disputed by the VAT registered person.

Another provision in the VAT law that is being removed is that through which a VAT return is deemed not to have been filed if it is not accompanied by the full payment of VAT declared to be payable therein.

The prescribed rate of interest on late payment of VAT, which is currently set at 9% per year, will be reduced and will be a flexible one, as may be determined by the Minister from time to time.

Offences against income tax law

Under current tax law, the Court is obliged, for a second offence against the provisions of the Income Tax laws, where this happens within five years from when the person has been warned by the Court following a first offence, to sentence the person to three days imprisonment in addition to any other punishment.

Amendments to the tax laws will be introduced to allow the Court discretion as to whether to sentence the person to prison or to impose a fine (multa) of €2,000.

MicroInvest Scheme

The MicroInvest Scheme will be reintroduced. Small enterprises and self-employed individuals will be allowed a 45% tax credit on eligible capital expenditure which increases to 65% if the small enterprise or self-employed individual carries out the activity in Gozo.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.