Tyler McGaughey, a partner in Winston's Washington office, and the former Deputy Assistant Secretary (DAS) for Investment Security at the U.S. Department of the Treasury, offers his thoughts on the key takeaways from CFIUS's recently published annual report for 2020, a year that was heavily impacted by the COVID-19 pandemic, and the first year that its new regulations were effective.

A few weeks ago, CFIUS published its annual report for calendar year 2020. The report can be found here. CFIUS's annual reports are a major event for dealmakers and other CFIUS watchers because they represent one of the only times that CFIUS publicly reveals information about its operations, which by law are highly confidential. Moreover, this year's report is the first since CFIUS published its new regulations, which became effective on February 13, 2020, and offers dealmakers their first glimpse of how CFIUS is handling some of its new authorities.

The key takeaways from this year's annual report are provided below. However, the most important takeaway is that CFIUS continued to perform its mission despite the hardships created by the COVID-19 pandemic. When the pandemic hit, it could have severely disrupted CFIUS's operations. Every CFIUS case involves classified information, and case officers can only review that type of information at secure government facilities—telework is not really an option. But despite the pandemic, the Committee did not halt its operations. Rather, it made a few adjustments to its processes and procedures and then continued to operate as usual so that business transactions could be cleared as quickly as possible. Indeed, as the annual report reflects, the overall number of transactions reviewed or assessed by the Committee increased substantially in 2020, and despite the case processing challenges posed by the COVID-19 pandemic, the Committee did not miss any of its statutory deadlines.

Other takeaways from the report include:

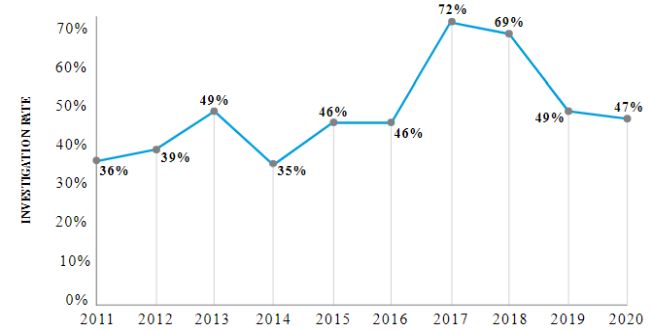

- The investigation rate for Notices continues to hover

around 50%. CFIUS analyzes transactions in two stages.

First, CFIUS has 45 days to conduct a "review." Second,

if necessary, CFIUS has another 45 days to conduct an

"investigation." Historically, the percentage of

transactions that have gone to investigation has hovered between

35% and 49%. In 2017 and 2018, the investigation rate spiked,

reaching 72% and 69%, respectively. In 2019, the investigation rate

dropped to 49%, a drop that was likely due, in part, to a provision

in the Foreign Investment Risk Review Modernization Act of 2018

(FIRRMA) that gave CFIUS an extra 15 days to conduct reviews. The

drop was also due, in part, to a renewed emphasis by the U.S.

Department of the Treasury, the chair of CFIUS, on clearing

transactions during the review period. In 2020, the investigation

rate dropped even further, to 47%.

Given that the investigation rate has stayed south of 50% for the last two years, dealmakers can safely assume that the spike in the investigation rate in 2017 and 2018 is over, and that the investigation rate is returning to historical levels. Accordingly, for any given transaction, dealmakers should expect to have about a 50/50 chance of clearing in review or going to investigation.

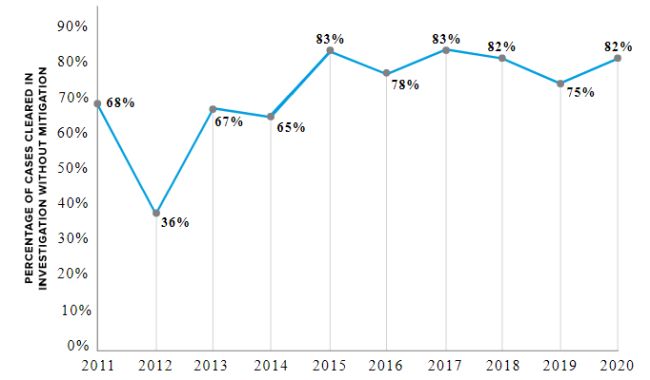

- CFIUS continues to clear a significant number of

transactions in investigation without mitigation. In 2020,

a total of 88 transactions proceeded to investigation, but only 16

transactions required mitigation, meaning that 72 transactions

(82%) were cleared in investigation without mitigation. The high

percentage of cases clearing in investigation without mitigation is

not a recent development. Rather, the percentage has been high for

several years.

The percentage of cases that clear in investigation without mitigation is a key indicator of how efficiently the Committee is reviewing transactions. If the Committee cannot identify a national security risk arising from a transaction, it should be able to clear the transaction during the 45-day review period, leaving the investigation period for more difficult cases that require mitigation or prohibition. This is particularly true after FIRRMA gave the Committee an extra 15 days to complete its reviews. In some cases there may be extenuating circumstances where it makes sense for the Committee to confirm that there is no national security risk by taking a transaction to investigation and performing additional due diligence. But those situations should be rare. As the graph reflects, CFIUS has room to improve in this area. For parties going through the CFIUS process, the takeaway is that even if a transaction goes to investigation, it does not mean that the transaction will likely be blocked or mitigated. Rather, the odds are still good—in fact, they are really good—that the transaction will clear without any mitigation at all.

- The Committee is requiring fewer withdraw/refiles and

forcing fewer abandonments. Parties withdraw a transaction

for two main reasons. In some cases, the transaction parties are

negotiating mitigation with the Committee, and the Committee

requests that the parties voluntarily withdraw and refile their

transaction (referred to as a "withdraw/refile"), which

restarts the clock and gives the parties more time to negotiate a

mitigation agreement. The parties are not obligated to withdraw

their transaction, but if they do not, the Committee may refer the

transaction to the President with a recommendation to block. Given

the alternative, transaction parties almost always voluntarily

withdraw and refile the transaction.

In other cases, the parties withdraw their transaction because CFIUS notifies the parties that mitigation will not work and that it intends to refer the matter to the President for a block. Because it is highly unlikely that the President will reject the Committee's recommendation, most parties choose to simply walk away from the deal rather than suffer the public embarrassment of a presidential block.

Historically, the total number of withdrawals has hovered between 8% and 16%. In 2017 and 2018, however, the number of withdrawals spiked, reaching 31% and 29%, respectively. During the 2017–2018 time period, the Committee was frequently requiring transaction parties to withdraw and refile their transactions, extending the CFIUS review process beyond 90 days. The Committee was also threatening to send a large number of transactions to the President, which drove up the number of transactions that were voluntarily abandoned for national security reasons. In 2019 the number of withdrawals dropped to 13%, and last year the number of withdrawals stayed about the same, rising slightly to 16%.

2013[1] 2014[2] 2015 2016 2017 2018 2019 2020 Total Number of Notices 97 147 143 172 237 229 231 187 Withdraw/Refiles - - 9 15 44 42 18 21 Forced Abandonments

(for national security)- - 3 3 24 18 8 7 Other[3] - - 1 9 6 6 4 1 Total Number of Withdrawals 8 12 13 27 74 66 30 29 Percentage of Total Withdrawals 8% 8% 9% 16% 31% 29% 13% 16%

For transaction parties, there are two main takeaways. First, when analyzing the likelihood that the Committee will block a transaction, dealmakers should not only look at the publicly available information on presidential blocks but should also consider the publicly available statistics on how many transactions are forced to be abandoned by the Committee each year. The statistics indicate that the Committee is forcing fewer abandonments than in 2017 and 2018, but it is still forcing some. In 2020, the Committee forced seven transactions to be abandoned— about one transaction every two months.

Second, although the number of withdraw/refiles has decreased in recent years, the Committee is still requiring transaction parties to withdraw and refile a nontrivial number of transactions each year—last year there were 21 withdraw/refiles. Thus, if dealmakers anticipate that their transaction will require mitigation, they should plan for the CFIUS review process to take longer than 90 days.

- The Committee is working hard to make the new

declarations process a success. Last year was the first

year the new declarations regulations were effective. Under the

declarations regulations, CFIUS can resolve a declaration in three

ways: (1) clear the transaction; (2) request a filing; or (3)

refuse to complete the action, which means that the Committee does

nothing—it does not clear the transaction, but it also does

not request a filing (i.e., the Committee gives the transaction a

so-called "shoulder shrug").

In 2020, transaction parties filed a total of 126 declarations. Of that total, the Committee cleared 81 transactions (64%). The Committee requested that the parties file a notice for 28 transactions (22%), and the Committee gave a "shoulder shrug" to 16 transactions (13%). One transaction was withdrawn for business reasons (1%).

The fact that the Committee was able to clear 64% of declarations the first year that the new declarations regulations were effective is impressive in its own right—it will naturally take some time for agencies to adjust to signing "safe harbor" letters based on less information and less time to conduct due diligence. But to achieve a high clearance rate during a pandemic year is a particularly significant achievement and a reflection of the hard work and dedication of Treasury's new declarations team, which administers the declarations process.

For dealmakers and other CFIUS watchers, the main takeaway is that CFIUS is obviously working hard to clear declarations during the 30-day assessment period. Dealmakers should be cautious about overreacting to the statistics, however. Most of the foreign acquirers who filed declarations were likely companies who (1) are from countries that are allies and partners of the United States and (2) submit frequent CFIUS filings and are therefore well known to the Committee. Indeed, the annual report supports this conclusion. There is a table in the annual report showing that the countries that filed the most declarations in 2020 were Canada, Japan, the United Kingdom, Germany, and Sweden.

Even though the statistics are promising, the annual report does not change our general advice regarding declarations. Declarations are best if the foreign acquirer recently submitted a CFIUS filing and was cleared in review, the transaction is straightforward (e.g., 100% acquisitions), and the U.S. business has few touchpoints with U.S. government agencies or the military. If a transaction does not have at least some of these characteristics, filing a declaration will likely just add 30 days to the CFIUS review process.

- The Committee is now publishing statistics on the

non-notified process. This year's annual report is the

first time that CFIUS has published statistics on the non-notified

process. The report states that "[t]here were 117 transactions

identified through the non-notified/non-declared process in 2020

that were put forward to the Committee for consideration," and

that "[f]rom the transactions identified, 17 transactions

resulted in a filing."

These statistics provide evidence for what most dealmakers and CFIUS watchers already know: the non-notified team is growing in size and taking a far more active role in scrutinizing non-notified transactions.

The statistics also highlight that CFIUS's non-notified team conducts due diligence on many transactions for which it does not request a filing. That is because CFIUS has the statutory authority to conduct due diligence on non-notified transactions that "may" fall within the Committee's jurisdiction. In many cases, the non-notified team needs to conduct due diligence to confirm whether CFIUS has jurisdiction over a transaction and, if so, whether the transaction presents a national security risk.

For dealmakers there are two main takeaways. First, if a transaction involves strategic competitors or raises significant national security issues, it will be increasingly difficult to keep the transaction off the Committee's radar. Indeed, the non-notified team conducted due diligence on over 100 transactions in 2020, notwithstanding the pandemic. That number will likely rise going forward. Second, if the Committee contacts transaction parties about an old transaction, it does not necessarily mean that the Committee will request a filing. That being said, the yield for last year—17 transactions (approximately 14%)—seems low. We expect that number to continue to rise in the future, particularly as Treasury's non-notified team hires more case officers and continues to get better integrated with Treasury's Office of General Counsel (OGC) and Treasury's Office of Reviews and Investigations (R&I).

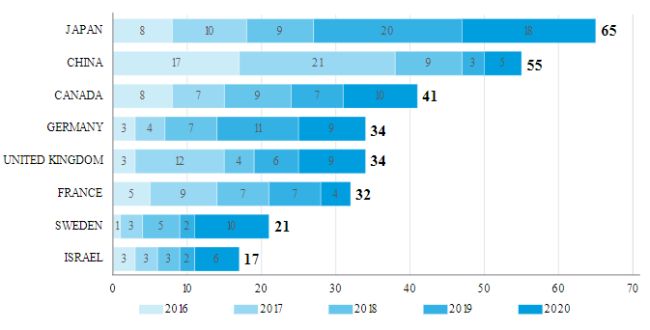

- Japanese, Canadian, and European companies are the most

active investors in U.S. critical technology, whereas Chinese

companies are making fewer investments. CFIUS reports

annual statistics on originating countries for covered transactions

involving acquisitions of U.S. critical technology companies. The

annual report indicates that in 2020 the top originating countries

were:

Home Country Number of Transactions Involving

U.S. Critical Technology CompaniesJapan 18 Sweden 10 Canada 10 Germany 9 United Kingdom 9 Israel 6 China 5 France 4

The list is dominated by Japan, Canada, and several European countries. Although China still appears on the list, over the past five years, the number of CFIUS filings involving Chinese acquisitions of U.S. critical technology companies has declined rapidly, falling from 21 filings in 2017 to three filings in 2019. Last year, Chinese investors submitted CFIUS filings for only five transactions involving U.S. critical technology companies.

As the graph above reflects, in the current geopolitical climate, it is challenging for Chinese companies to negotiate the CFIUS review process successfully, especially in cases where a Chinese company wants to acquire a U.S. critical technology company. Accordingly, we are seeing a drop in filings from Chinese acquirers. Conversely, over the last two years, there has been a significant rise in the number of CFIUS filings from Japan, and this year there was a rapid rise in filings from Sweden.

Footnotes

1 The 2013 Annual Report only provides statistics on the total number of notices and withdrawals.

2 The 2014 Annual Report only provides statistics on the total number of notices and withdrawals.

3 Parties also withdraw and abandon their transactions because they failed to satisfy the CFIUS process requirements or because of commercial reasons.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.