The combined gross domestic product (GDP) of the 10 member states of the Association of Southeast Asian Nations (ASEAN) stands at $2.8 trillion—equivalent to ranking fifth in the world's largest economies1. Although the impacts of the COVID-19 pandemic on the region are highly uncertain at the time of writing, the pre-COVID-19 expectation was for GDP to grow at a projected average rate of 5.5 percent per annum across the ASEAN region. This is certainly an attractive opportunity for foreign investment. Once we emerge from the COVID-19 pandemic, the key to ensuring the renewed growth trend in ASEAN is energy, both in terms of providing ASEAN members with the power needed to drive their growing economies and in creating opportunities for foreign direct investment.

In our new series, “Energy in ASEAN: the essentials,” we will provide an insight into the key components of the energy market in the ASEAN member nations, with a particular focus on oil and gas, conventional power and renewable energy. We will provide an overview of the regulatory landscape in the energy sector, as well as highlighting some of the key legal issues that prospective investors should take into consideration.

All Part of a Master Plan

In the first of our articles, we consider the renewable energy industry in Vietnam, one of Asia's fastest-growing economies. Despite seeing its projected GDP growth falling from 6.82 percent to 4.8 percent in light of the fallout of the COVID-19 pandemic, Vietnam has established itself as a global manufacturing hub and is benefitting from the fallout of the U.S.-China trade war. The continued growth of Vietnam's economy has been matched by an ever-increasing demand for energy, with electricity consumption projected to expand at an annual rate of 10–12 percent through 2030. However, it remains to be seen whether this will be impacted by the inevitable aftereffects of the ongoing COVID-19 pandemic.

The primary legislation governing the power sector in Vietnam is the Electricity Law of 2004 (as amended)3. The Electricity Law requires that national power development master plans be established for 10-year periods. On July 21, 2011, the Vietnamese government released the National Power Development Plan for the 2011–2020 period with the Vision to 20304 (the “Original Master Plan”). The goal of the Original Master Plan was to set out a strategy to secure Vietnam's energy needs, while improving interconnectivity in rural areas and increasing the nation's reliance on renewable sources of energy. The Original Master Plan indicated that investment totaling $150 billion, in both new generation and grid development, was required in order to keep pace with Vietnam's rising level of electricity consumption.

In March 2016, the Revised Power Development Master Plan VII5 (the “Revised Master Plan”) was released. The Revised Master Plan provided for, among other things:

- Reliance on renewable energy (excluding large and medium scale hydropower) to be 10 percent of total generation by 2030 (up from seven percent under the Original Master Plan).

- A reduction in coal-fired generation.

Solar is seen as key to the proposed increase in renewable generation capacity, with Vietnam aiming to install 12GW by 2030.

Achieving the Targets

The Vietnamese government, in a bid to promote the goals set out in the Original Master Plan, issued a decision in November 20156 which approved Vietnam's renewable energy development strategy up until 2030 (the “Renewable Decision”) and also provides guidance on the strategy through 2050. The Renewable Decision provided that investors in renewable projects would be entitled to those incentives already prescribed for in existing legislation (i.e., the Law on Investment7) such as:

- Import duty relief – An exemption from import duty in respect of goods imported in order to construct or form fixed assets as part of a renewable energy project, as well as materials, components and semi-finished products (that cannot be manufactured domestically), to be utilized in respect of the foregoing.

- Corporate income tax – New investment projects for renewable energy production will be subject to a reduced corporate income rate of 10 percent for the first 15 years of the project (compared with the lowest rate of 20 percent applied to companies not qualifying for relief)8.

- Land-related incentives – Investors in

renewable energy projects may be entitled to the following

land-related incentives9:

- Exemption from land use fees for a period of 11 years.

- Exemption from land use fees for a period of 15 years where the project is located in a region facing “extreme socio-economic difficulties.”

- During the capital construction period of a project (being the period of construction of a new building, or plant, for up to three years from the effective date of the land lease contract), investors are entitled to exemption from land rents and water surface rents.

The incentives detailed above were designed to stimulate growth in Vietnam's renewable energy sector. However, investor uptake in the wake of the Renewable Decision was relatively muted, prompting further action by the Vietnamese government in 2017, specifically targeting the solar market, which in turn initiated a period of rapid development.

Part A: The Solar Story

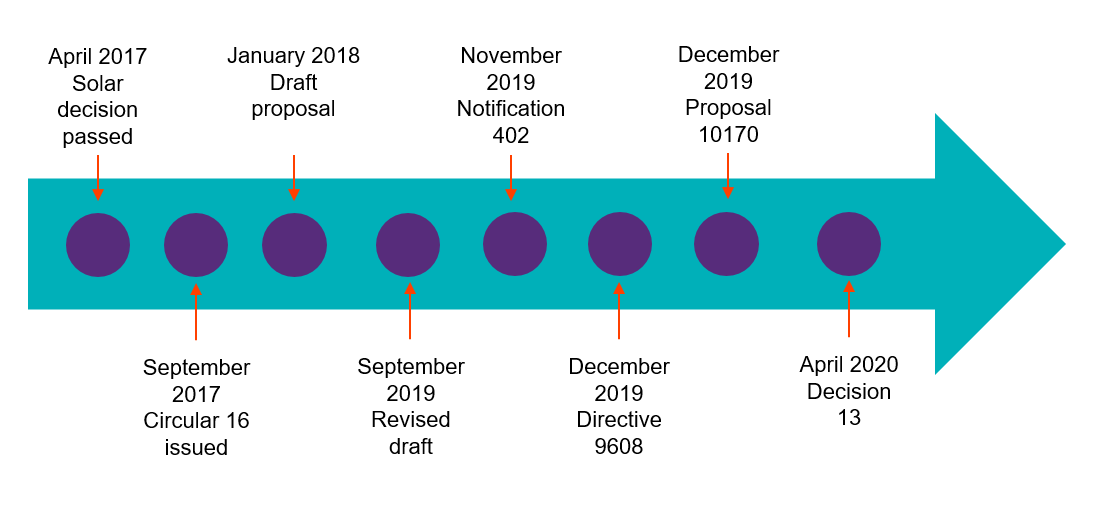

Since 2017, a significant number of decisions, proposals and circulars (as illustrated by the timeline below), were issued by both the Vietnamese government and the Ministry of Industry and Trade (MOIT) in an attempt to create a clear regulatory framework to attract investment into the solar sector. As we shall see, there are signs that this arduous process may be close to conclusion, but certain issues have yet to be resolved.

The Solar Decision

In April 2017, the Vietnamese government issued a decision that had the effect of prioritizing solar over other energy sources in the context of the Revised Master Plan10 (the “Solar Decision”). It is in the solar sector where Vietnam has experienced the most impressive growth in renewable energy capacity. In 2018, solar accounted for only 134MW of renewable capacity, equivalent to three percent of Vietnam's total renewable capacity (excluding large and medium scale hydropower). Recent data published by state-owned utility company Electricity Vietnam (EVN) indicates that Vietnamese solar generation in the first quarter of 2020 surged by 28 times to 2.3 billion KWh compared with the same period in 2019. EVN also highlighted that as many as 91 solar farms, with a total capacity of 4,550 MW, began operation in 2019, bringing the aggregate capacity of solar plants to 25,000 MW11. In doing so, Vietnam appears to have smashed its 2020 solar target of 4,000 MW, provided for in the Revised Master Plan, and has now overtaken Thailand as the largest solar market in Southeast Asia12.

The rapid expansion of the solar sector can largely be attributed to the implementation of the Solar Decision which sets out, amongst other things, the feed in tariff (the “Solar FIT”) applicable to solar projects (both grid-connected and roof-top based). The Solar FIT mandated:

- A power price for grid-connected solar projects of VND 2,086/kWh (excluding value-added tax (VAT)), (equivalent to $9.35/kWh).

- An exchange rate set at VND 22,316 to $1.00 (as announced by the State Bank of Vietnam on April 10, 2017).

The Solar FIT exclusively applied to grid-connected projects with solar cell efficiency of more than 16 percent or solar module efficiency of more than 15 percent

Adjustment to the Solar FIT and the Model Solar PPA

While the Solar FIT is the same for both grid-connected and rooftop projects, the adjustment mechanism for each is different. Adjustment of the grid-connected Solar FIT is dealt with under the model power purchase agreement (the “Model Solar PPA”), published by Circular No. 16/2017/TT-BCT in September 2017 (“Circular 16”). Adjustment of the Solar FIT for rooftop projects, however, is dealt with by way of annual review by the MOIT (based on the last exchange rate of the preceding calendar year), with the adjusted Solar FIT applying for the following year.

In addition to publishing the Model Solar PPA, Circular 16 reaffirmed the applicability of the Solar FIT to grid-connected and rooftop projects as originally stated in the Solar Decision. A further key aspect of Circular 16 was the requirement for solar power projects to be included in the approved provincial and national solar power development plans prior to execution. It is, therefore, critical for prospective developers to ensure that their projects are included on said plans prior to entering into firm development commitments.

As regards the terms of the Model Solar PPA itself, there are a number of commercial and legal issues arising from it that give investors cause for concern. These concerns relate primarily to bankability, but we will discuss these in in detail in an upcoming article in this series.

The Draft Proposal and Revised Draft

Returning to the Solar Decision, in addition to establishing the Solar FIT, it reaffirmed that the incentives provided for under the Renewable Decision would apply in respect of solar energy projects. The Solar Decision came into force on June 1, 2017, and expired on June 30, 2019. During that period (particularly throughout 2019), the sector underwent rapid growth as developers sought to take advantage of the Solar FIT. The expiry of the Solar FIT, however, created a degree of uncertainty for prospective investors that the MOIT sought to address by issuing a draft proposal to the Vietnamese government in January 2018 for new Solar FIT mechanisms that would apply from July 1, 2019, to June 30, 2021 (the “Draft Proposal”).

Under the initial Draft Proposal (which underwent several iterations over the course of 2019), the MOIT proposed varying levels of Solar FITs, based on geographic region and technologies, with prices ranging from VND 2,159/kWh ($6.67/kWh) to VND 2,486/ kWh ($10.87/kWh). It is understood that the rationale for the geographical split in the FIT was to promote solar power development in those regions of Vietnam that had not seen significant investment in the sector (the majority of solar projects in Vietnam have been developed in the southern or central highland provinces). Consultation between the Vietnamese government and various stakeholders led to the Draft Proposal being revised and resubmitted by the MOIT in September 2019 (the “Revised Draft”).

Notification 402

In November 2019, the Vietnamese government released Notification No. 402/TB-VPCP (“Notification 402”), which proposed a number of amendments to the Revised Draft and introduced a new proposal from the MOIT to move to an auction-based system that would replace the Solar FIT. Notification 402 suggested that certain projects would still be entitled to the benefit of the existing Solar FIT, such as those ground-based projects that had already executed PPAs and would achieve a commercial operation date (COD) during 2020.

Directive 9608 and Proposal 10170

In December 2019, the Vietnamese government issued Directive No. 9608/BCT-DL (“Directive 9608”), which instructed the provincial People's Committees and EVN, to suspend all proposals for grid-connected solar projects pending clarification on the new remuneration mechanism. On December 31, 2019, the MOIT issued Proposal No. 10170/TTr-BCT (“Proposal 10170”), which incorporated the government's proposals set out in Notification 402, as well as setting out the following in respect of the Solar FITs:

- A new Solar FIT for grid-connected floating solar projects of VND 1,758/kWh ($7.69/kWh).

- A new Solar FIT for grid-connected, land based, solar projects of VND 1,620/kWh ($7.09/kWh).

Proposal 10170 also set out the criteria for solar projects looking to qualify for the new Solar FITs. Specifically, qualifying projects had to be those meeting one of the following criteria:

- In respect of which PPAs had been executed prior to November 22, 2019.

- Which had “commenced construction” prior to November 22, 2019.

- Which will achieve their COD between July 1, 2019, and December 31, 2020.

We note that to qualify as having “commenced construction,” solar projects had to have obtained/executed each of the following:

- The project's technical design, as appraised by the relevant authority.

- Construction permit (to the extent applicable).

- Construction contract with the relevant contractor(s).

Proposal 10170 went further in setting out a list of solar farms deemed eligible for the proposed new Solar FIT, noting that this list is exclusive of solar farms located in Ninh Thuan Province (please see below). Proposal 10170 also addressed a number of other key issues relating to solar projects, namely:

- Solar rooftop FIT: It proposed a reduction in the FIT for rooftop solar, from VND 2,156/kWh ($9.35/kWh) to VND 1,916/kWh ($8.38/per kWh).

- Special policy in relation to Ninh Thuan Province: It continued to recognize the Vietnamese government's special policy with regard to the development of solar power projects located in Ninh Thuan Province. Essentially, certain listed projects in this province would be entitled to receive the existing Solar FIT (i.e., VND 2,086/kWh (equivalent to $9.35/kWh)), provided they achieve COD prior to January 1, 2021. However, those projects would only be entitled to receive the existing Solar FIT between COD and January 1, 2021. Thereafter, the projects would move to one of the new proposed Solar FITs set out above. In addition, the right to receive the existing Solar FIT will only apply until such time as 2,000 MW of total accumulated capacity is installed in Ninh Thuan Province.

- Proposals for the implementation of pilot solar auctions: In the event that a solar project does not qualify for either the new or existing Solar FIT, the MOIT proposed that the market undergoes transmission to an open, competitive and transparent auction mechanism. Under Proposal 10170, the Electricity and Renewable Energy Agency was requested to expedite the development of the solar auction mechanism. In addition, MOIT requested that EVN selected one potential project location for launching a pilot solar auction in accordance with relevant legislation, with the pilot auction to be launched during the course of 2020.

The Way Forward – Decision No. 13/2020/QD-TTG

Following hot on the heels of Proposal 10170, the Vietnamese government appears to have finally reached a conclusion regarding future development of Vietnam's solar sector with the issuance of Decision No. 13/2020/QD-TTg (“Decision 13”) on April 6, 2020. Decision 13, which will come into effect on May 22, 2020, is broadly consistent with the proposals set out in Proposal 10170, with its key aspects summarized as follows:

- Extension of the Solar FIT: It provides for an extension of the Solar FIT for those projects that failed to achieve COD by June 30, 2019 (albeit reflecting the proposed reduction in the Solar FIT as proposed by Proposal 10170), with the exception of those projects located in Ninh Thuan Province (see below). Decision 13 states that, in addition to the qualification criteria set out in Proposal 10170, projects seeking to obtain the benefit of the Solar FIT must have solar cell efficiency of greater than 16 percent, or module efficiency greater than 15 percent. Projects not satisfying the conditions will have their purchase price for electricity determined by a “competitive mechanism.” Although no further clarification has been provided on this point, we understand that it refers to the pilot auction mechanism (see above).

- Criteria for rooftop Solar FIT qualification:

It classifies rooftop solar power projects as follows:

- Projects selling all, or part, of their electricity production to EVN.

- Projects selling all, or part, of their electricity production to other purchasers not directly connected to the EVN grid.

This is an interesting development as, previously, rooftop projects were restricted to selling their electricity solely to EVN. With the implementation of Decision 13, small-scale rooftop developers now have the flexibility to sell to other purchasers not directly connected to the grid and should, in theory, have the right to do so on negotiated contractual terms rather than the terms of the Model Solar PPA.

In order to qualify for the new rooftop Solar FIT (again, as proposed in Proposal 10170), projects must satisfy the following criteria:

- Have been directly connected to the EVN grid.

- Have sold electricity to EVN.

- Have achieved COD, and had verified meter readings, in the period between July 1, 2019 and December 31, 2020.

In the event that a project does not satisfy the conditions set out above, then the purchase price for the electricity shall be as agreed between the parties. Such sale arrangements do not appear to require use of the Model Solar PPA, but we anticipate further clarification from the Vietnamese government in this regard. Note that the existing maximum capacity of 1 MW and voltage of 35kV will continue to apply in respect of projects looking to obtain the benefit of the rooftop Solar FIT.

Ninh Thuan Province Policy: Decision 13 continues the “special policy” relating to Ninh Thuan province. Consequently, the existing Solar FIT of $9.35/kWh will continue to apply to projects in Ninh Thuan that achieve COD prior to January 1, 2021 (as provided for in Proposal 10170) provided that:

- Total installed capacity in the province does not exceed 2,000 MW.

- Such projects have been included in the national/provincial power development plans.

Projects located in Ninh Thuan that fail to achieve COD prior to January 1, 2021, will receive an FIT to be determined by a “competitive mechanism” and, again, we understand that this relates to the auction mechanism described above.

Other Points to Note:

- Sellers and purchasers: Previously, the Solar Decision mandated that EVN be the sole off-taker of electricity generated by solar power projects. However, Decision 13 appears to offer a new approach that contemplates sale to parties not forming part of the EVN group. This should, in theory, break the monopoly held by EVN and help to further develop Vietnam's electricity market.

- Model Solar PPA: Decision 13 reaffirms that, for sales to EVN, project investors must execute a PPA with EVN based on the Model Solar PPA, for a fixed term of 20 years from the COD and with the ability to extend subject to the agreement of the parties. For projects in which the purchaser is not an EVN group company, the parties are, apparently (and as highlighted above), permitted to freely negotiate the price, terms and conditions of the supply and purchase of electricity. However, we expect the government to issue further guidance in this regard.

Conclusion: The release of Decision 13 is a welcome development in Vietnam's solar power sector and, to a certain extent, helps to alleviate a number of developer concerns (primarily regarding the extension of the Solar FIT). However, we anticipate that further clarification will be required in order to address a number of matters, particularly the prospective pilot auction mechanism. The limited term of Decision 13 (until December 31, 2020) indicates that the Vietnamese government foresees the competitive bidding model as the future for the solar market.

Part B: Wind on the Rise?

With over 3,000 km of coastline and a monsoonal climate, Vietnam is considered a prime candidate for wind energy development. The Revised Master Plan envisages 800 MW of wind-generated capacity being installed by 2020, 2 GW by 2025 and increasing to 6 GW by 2030. In 2019, the Vietnamese government approved the preparation of a feasibility study for a proposed offshore wind farm project in an area off the cape of Kê Gà, in Binh Thuan province, South Vietnam. In the event that the project completes, it would be, at the time of writing, the world's largest offshore wind farm with a capacity of 3,400 MW. U.K. renewable developer Enterprize Energy is leading the project, along with Vietnamese partners Petroleum Equipment Assembly & Metal Structure and Việt Nam-Russia Oil and Gas Joint Venture (known as “Vietsovpetro”), which has been engaged to undertake design, construction and installation of the offshore infrastructure, as well as connection to the transmission grid.

The feed-in tariff applicable to wind energy projects in Vietnam (the “Wind FIT”) was initially implemented by Decision No. 37/2011/QD-TTG (“Decision 37”). On September 10, 2018, the government issued Decision No. 39/2018/QD-TTG (“Decision 39”), which provided for an increase in the Wind FIT and separate Wind FITs in respect of onshore and offshore wind projects as follows:

- Onshore - VND 1,928 /kWh ($8.5/kWh).

- Offshore - VND 2,223 /kWh ($9.8/kWh).

The Wind FITs set out in Decision 39 apply to all on- and offshore wind projects achieving a COD prior to November 1, 2021. It is unclear whether the Vietnamese government intends to introduce new Wind FITs post-November 2021 or move to an auction-based mechanism as now appears likely for solar. This creates a degree of uncertainty for wind projects, such as Kê Gà, which is not expected to achieve COD until 202713.

However, there are signs that this lack of clarity may be about to change. Earlier this month, the MOIT submitted a proposal to the Vietnamese government to extend the existing Wind FITs to the end of 2023 from the original expiry date in November 2021. Despite not having seen the proposal, we understand that the MOIT has proposed moving to an auction-based mechanism.

The Model Wind PPA

The first standardized power purchase agreement for wind power projects in Vietnam (“Model Wind PPA”) was issued with Circular No. 32/2012/TT-BCT (“Circular 32”) in 2012, which sets out the regulations relating to the development of wind power projects in Vietnam. A key aspect of Circular 32 was the requirement for the General Directorate of Energy to establish a list of wind power projects to be permitted for development over the next five years and submit the same to the MOIT for approval. It is, therefore, critical for prospective developers to ensure that their projects are shortlisted prior to entering into firm development commitments. The terms of the Model Wind PPA caused concern among international developers, as well as the local business community. One issue of key concern is the bankability of the PPA from a project-finance perspective. The Vietnamese government recently attempted to address certain of these concerns by issuing Circular No. 02/2019/TT-BCT (“Circular 2”), which amended the Model Wind PPA, as well as specifying the procedure for the negotiation and execution of PPAs for wind power projects in Vietnam. We will consider the Model Wind PPA alongside our analysis of the Model Solar PPA in an upcoming article in this series.

Part C: Looking Ahead

Historically, hydropower has been the key source of renewable energy in Vietnam. In the International Hydropower Association's 2019 report, Vietnamese hydropower capacity (including large-scale) was estimated at 16.68GW (believed to have increased to almost 18GW at the time of writing), making it the fourth largest in the Asia-Pacific behind China, Japan and India. However, concerns regarding the impact of large-scale hydropower on the environment and local communities (for example, the 2018 Xe Pian-Xe Namnoy hydropower dam collapse in Laos, where at least 40 people died and thousands were made homeless) are leading some countries to focus on other, less intrusive sources of renewable energy. Indeed, it is worth noting that the Revised Master Plan does not focus on the development of large-scale hydropower as a renewable source of energy to be prioritized for development, but does promote an increase in capacity to 21.6GW in 2020 and approximately 27.8GW by 2030, through small, multipurpose projects.

The anchor hydropower project in Vietnam is the 2.4GW Son La plant, located on the Da River approximately 340km northwest of Hanoi. The plant was completed in 2012 and is capable of generating up to 10 billion kWh per year, making it the largest hydropower plant in Southeast Asia.

Vietnam, it appears, is not alone in moving away from large-scale hydropower to small scale, as evidenced by a 2017 study undertaken by the United Nations and the Singapore-based Development Bank of Singapore14. The report identifies that the ASEAN region held some of the best-untapped hydropower potential in the world and that small (e.g., 6-7MW) hydropower projects could be developed with relatively low capital investment (approximately $30 million) and taking only around two years to complete. However, micro-hydropower projects (e.g., capacity less than 1MW) are likely to support only small rural communities and, as such, are considered less bankable15.

Counting on Coal?

Notwithstanding the goals set by the Revised Master Plan and undoubted advances made in the field of renewables, Vietnam remains heavily reliant on coal-fired power generation. While the Revised Master Plan sets a clear objective to reduce Vietnam's dependence on coal-fired generation, the reality is that, in 2020, 49.3 percent of the country's capacity will still be generated from coal-fired power stations. By 2030, coal's share of generating capacity is forecast to increase to 53.2 percent16, with a number of new coal-fired power plants earmarked for development.

As highlighted above, Vietnam has been undergoing a period of rapid growth that (notwithstanding the immediate impact of the COVID-19 pandemic on demand) is expected to continue over the course of the next decade. When power consumption hit a record 36,000 MW in May 2019, close to the then-maximum capacity, the government requested that consumers reduce air-conditioning usage in order to help avoid blackouts17. Vietnam will need to develop additional capacity quickly and cost effectively in order to ensure that economic development is not derailed in the long term. The likelihood is that much of the required new capacity will be derived from coal, and the Revised Master Plan contemplates this.

However, it remains to be seen whether government policy will continue to support new coal-fired generation when the eighth power master plan (“Master Plan VIII”) is released. In an interview with the Vietnam News Agency in September 2019, Nguyễn Mạnh Cường, an official from the Institute of Energy's Department of Electrical System Development under MOIT, commented that while the Revised Master Plan relied “heavily on traditional power sources such as hydropower, thermal power, and gas turbines”, Master Plan VIII will be the “the electricity plan of the renewable energy era.”18 With details of Master Plan VIII not yet published, prospective investors are likely to be paying close attention to whether the government intends to reduce reliance on coal and introduce further incentives for the development of renewables.

Conclusion

Over the past two years, Vietnam has demonstrated significant progress in promoting renewable energy but it remains to be seen whether the nation is capable of fulfilling the goals set out in the Revised Master Plan by the June 2020 deadline. In addition, as far as Master Plan VIII is concerned, it also remains to be seen whether renewables can take center stage in Vietnam's power market over the course of the next decade.

Continued reliance on coal and investor concerns in relation to bankability regarding the Model Wind and Solar PPAs are key inhibitors to the development of the renewable sector in Vietnam. These issues need to be addressed in order for the country to move forward and attract the level of investment required to develop enough renewable capacity to meet its increasing demand for energy.

Nevertheless, we see significant potential in the Vietnamese renewables market, and the nation certainly appears to be demonstrating its commitment to the sector by the significant advances made, particularly in respect of solar, over the course of 2019. We expect the solar development story to continue, perhaps at a somewhat reduced pace, following clarification of the new remuneration mechanism, along with a drive from existing projects to achieve their respective CODs prior to the end of 2020 in order to take advantage of the apparent extension of the Solar FIT. Focus on the wind sector is expected to increase, but this is likely to be dependent on the government softening its stance in respect of amendments to the Model Wind PPA.

Footnotes

1 U.S. – ASEAN Business Council, Inc., “Growth Projections,” July 22, 2019.

2 The World Bank – The World Bank in Vietnam, October 18, 2019.

3 Law No. 28/2004/QH11 on Electricity, December 3, 2004, as amended.

4 Decision No. 1209/QD-TTg.

5 Decision No. 428/QD-TTg.

6 Decision No. 2068/QD-TTg.

7 Law No. 67/2014/QH13.

8 PwC, Vietnam, “Corporate – Tax Credits and Incentives.”

9 Decree No. 46/2014/ND-CP, Regulations on collection of land rent and water surface rent.

10 Decision 11/2017/QD-TTg.

11 VnExpress, “Solar power generation surges 28 times”, 14 April 2020.

12 Ibid.

13 Eco Business, “Gusty growth: Vietnam's remarkable wind energy story,” November 19, 2019.

14 DBS and UN Environment Enquiry, “Green Finance Opportunities in ASEAN,” November 2017.

15 Ibid.

16 Decision No. 428/QD-TTg.

17 Reuters, “In Vietnam's booming energy sector coal reigns, but renewables play catch-up,” May 24, 2019.

18 Viet Nam News, “Power Development Master Plan 8 focuses on renewable energy,” September 28, 2019.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.