Geopolitical tensions have been elevated between the US and China, creating waves of disruption across industrial supply chains. Following the US ban on Chinese telecom equipment in 2019 and the subsequent nearshoring of semiconductors in 2022, the biopharma supply chain is now at the center of a storm as the BIOSECURE Act makes its way through Congress.

The bipartisan bill seeks to reduce American dependence on Chinese biopharma manufacturing and limit the transmission of citizens' genomic data to a foreign adversary.1 The latest draft provisions would restrict US government agencies from contracting with any organization that collaborates with Chinese 'biotechnology companies of concern.' Given the industry's broad involvement in federal contracts, the pending restrictions could have wide-reaching impacts across the sector.

The bill passed the House on September 9th with broad support and will likely be considered as part of a larger legislative package through the Senate this year.2 The exact scope and impact of the bill continue to evolve, including the types of contracts affected and whether limits on collaboration apply to all projects or only those with federal funding. Still, the stakes are high. In a recent survey by leading industry trade group Biotechnology Innovation Organization (BIO), ~80 percent of US biopharma companies reported a relationship with a Chinese contract development and manufacturing organization (CDMO), revealing the industry's reliance on China for developmentscale and commercial manufacturing.3

In this paper, we discuss the actions companies have been taking in response to the bill, the impact it will have on different stakeholders, and strategic moves companies and investors should take to turn disruption into advantage.

CONTEXT FOR THE BILL'S EMERGENCE

In recent years, biopharma companies have increased their reliance on Chinese providers to manufacture their drugs. WuXi AppTec and WuXi Biologics, two companies named in the bill, have partnerships to manufacture key branded drugs such as Imbruvica (J&J, Abbvie), Jemperli (GSK) and Trikafta (Vertex), and by one estimate, have been involved in developing 25 percent of all drugs used in the US.4

As reliance on Chinese manufacturers has grown, Congress has taken notice. BGI Group's (formerly BGI-Shenzen) acquisition of California-based Complete Genomics in 2013 initially sparked fears that health data of Americans could be accessed by the Chinese military.5 Amid growing concerns about intellectual property theft and the need for resilience in a critical sector, the BIOSECURE Act has garnered rare bipartisan support. (Chinese CDMOs focused on small-molecule drugs versus biologics have avoided being targeted by the bill.)

The industry is now responding with concerns of its own. In a recent survey by industry observer and publisher BioCentury, 90 percent of pharmaceutical executives said they anticipate product pipeline slowdowns if the legislation were to be enacted, with 64 percent expecting a "substantial" slowdown.6 Provisions added in May would grandfather existing contracts until 2032 and limit the scope to only those funded by federal agencies. However, moves are already underway.

SHIFTING CURRENTS IN BIOPHARMA MANUFACTURING

A June survey by LEK Consulting signaled a measured, cautious industry reaction to the emerging legislation. The survey noted that only two percent of companies globally have begun unwinding relationships with companies named in the bill and that just 13 percent would only consider non-Chinese CDMO partners.7

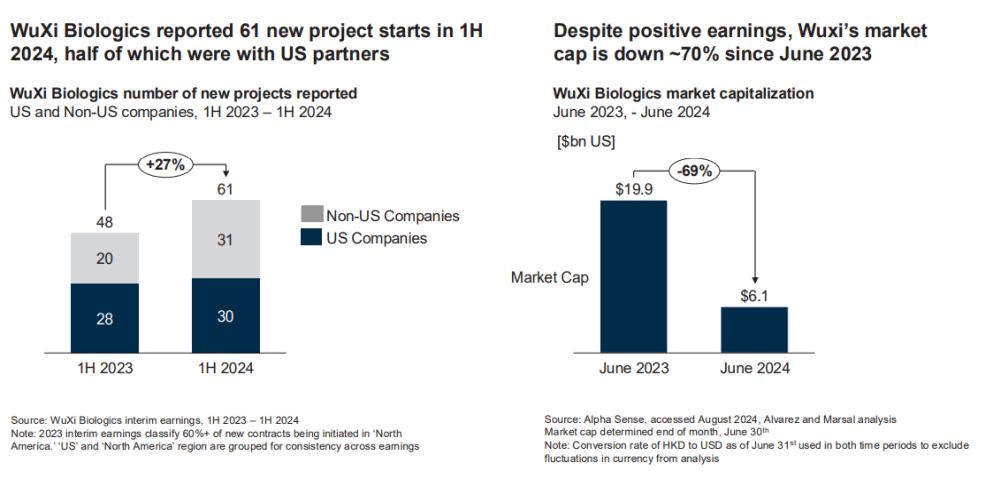

In late August, WuXi Biologics (2269.HK) released its interim results for 1H 2024, citing growth in new project starts despite the geopolitical headwinds of the BIOSECURE Act. In particular, the update indicates that ~30 new projects were initiated with US companies in the first half of the year.8 Despite the apparent momentum, investors have lowered expectations for the company's prospects: WuXi Biologics' market capitalization has declined 70% since June of last year.

Boosting Bio: How Pharma Is Scaling Manufacturing

Companies have been investing heavily in their biomanufacturing capacity, some in direct response to the BIOSECURE Act and others as part of broader industry tailwinds. Examples include:

- India-based CDMOs such as Enzene and Aragen are making significant investments to boost their Biologics manufacturing capacity and capabilities.9.10

- Swiss CDMO Siegfried purchases Curia's early-phase manufacturing site in Wisconsin, and competitor Lonza acquires large-scale biologics manufacturing site in California from Roche for $1.2 billion in cash11.12

- Private equity firms KKR, Cinven, CVC, Antin, and Permira, submit bids on Spanish pharma Rovi's contract development and manufacturing business line, valued at $3.5 billion13

- Research tools and services company Agilent Technologies announces acquisition of Canadian based specialty CDMO Biovectra for $925 million14

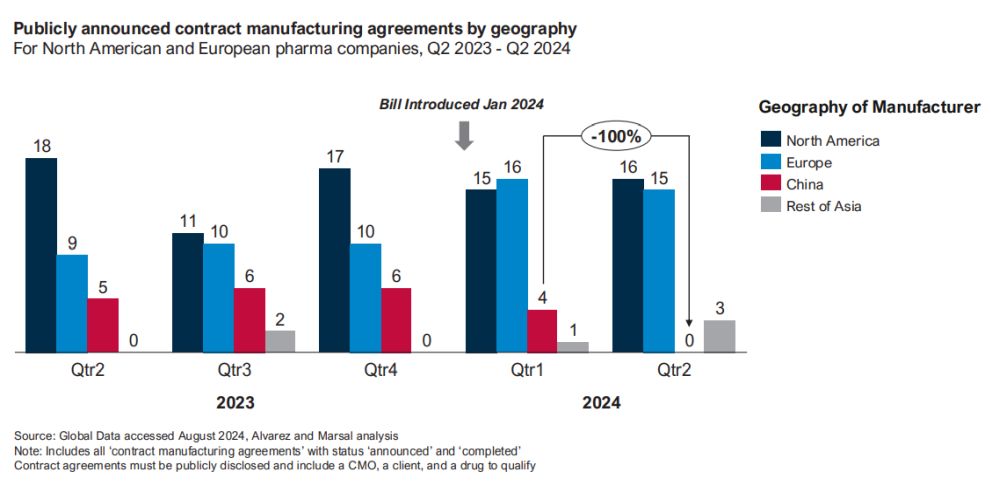

Across the industry, there are signals that the act is already impacting company decision-making. We examined the number of publicly announced contract manufacturing agreements between Chinese partners and biopharma companies in North America and Europe. In Q2 2024, the number of announced agreements declined materially.

New contracts announced with Chinese manufacturing partners have declined materially since introduction of BIOSECURE Act

Our analysis shows that:

- In China, the number of new contract manufacturing agreements announced with North American and European biopharma companies declined from ~5 agreements per quarter in the prior 12 months to zero in Q2 2024.

- In Europe, the number of new contract manufacturing agreements announced increased after the bill was introduced in January 2024.

- In the rest of Asia, the number of new manufacturing agreements announced saw an uptick in Q2 2023, the highest in the past five quarters.

How should the decline in manufacturing contracts announced be interpreted, and why the apparent discrepancy with new projects reported at WuXi? One explanation could be that multiple projects are conducted under umbrella contracts spanning a portfolio of drugs. Another could be that new projects are tied to contracts that were previously announced. Alternatively, fewer companies could be choosing to publicly announce their contracts with CDMO partners in China. Regardless, the currents in biopharma manufacturing appear to be shifting.

STAKEHOLDER IMPACTS ACROSS THE BIOPHARMA LANDSCAPE

While threatening supply chain partnerships in China, the BIOSECURE Act presents the industry with both imperatives and opportunities. Stakeholders will feel the impact in different ways.

US-based biopharma companies will need to transition existing manufacturing relationships and invest time and resources to integrate new value chain partners. The BIO survey indicates that 85 percent of biopharma companies believe changing vendors for preclinical and clinical work would take between six months to six years, highlighting the complexity in decoupling with existing vendors.15 Additionally, companies operating in China must prepare for a potentially harsher business environment, as the risk of regulatory retaliation is high.

Non-Chinese CDMOs are presented with an opportunity to capture business volumes previously serviced by Chinese companies. Meeting this demand will require increased investment in biologics manufacturing capacity through targeted acquisitions or construction of new Active Pharmaceutical Ingredient (API) facilities, paired with the hiring and training of a skilled labor force.

Private equity and strategic investors can seize this moment to pursue new acquisitions of CDMOs and expand capacity through integration with existing CDMO platforms. They may also find the potential to acquire divested USbased operations from Chinese companies.

FINDING OPPORTUNITIES AMID DISRUPTION

The companies that find success through the BIOSECURE Act, by taking advantage of opportunities and mitigating risks and costs, will be those acting today. Here are four moves that companies should pursue to capitalize on disruption.

Refresh partnership strategies across the value chain

- Conduct risk assessments of current suppliers and their likelihood to be named as a company of concern in the future, considering both contract manufacturing and clinical research agreements

- Develop partner management programs to ensure available capacity, considering the competition for space at alternative manufacturers

- Establish agreements with multiple biopharma manufacturing partners, incorporating geographic diversity, to create surge and redundancy options

Pressure test roadmap for scaling and sustaining volume to avoid drug shortages without sacrificing on margin

- Evaluate return on investment for capacity expansion, including decisions on whether to build, buy, or partner, considering demand forecasts, complexity of manufacturing, and geographic reach

- Consider on-shoring vs other-shoring production and identify strategic "landing spots"

- Contract manufacturers with excess capacity should leverage their positioning to both partner with biopharma companies and pursue contracts diverted from Chinese companies

- Manage the cost of support functions through fit-for-purpose design and digital enablers

Include tax in planning to build tax and trade efficiency into the new operating model and capitalize on available incentives

- Implement strategic tax and trade structures as the business goes through geographic shifts in the value chain (e.g., R&D, procurement, or production moving to new locations)

- Manage tax costs while shifting activities to other countries (e.g., exit tax, withholding taxes)

- Optimize duty and indirect tax costs by setting up production sites in Free Trade and Special Economic Zones

- Assess Rules of Origin to successfully shift production to non-China locations for US customs purposes

- Explore potential state and local incentives such as project-cost assistance through tax increment financing, sales and use tax exemptions, property tax and payroll incentives, tax credits or cash grants

Target new deals to strengthen position in advanced manufacturing

- Ramp up target screening in CDMO space as risk of trade tariffs paired with domestic incentives provide favorable investment tailwinds

- Evaluate opportunities to carve out manufacturing capabilities from larger manufacturers with excess capacity

- Prepare for divestures of US and European operations by Chinese companies

Precedent in the Telecom Sector?

In 2019, out of national security concerns over surveillance and cybersecurity, Congress added Section 889 of the National Defense Authorization Act barring government agencies and any companies being paid through contracts with the federal government from using communications equipment or components from 21 named Chinese companies, including Huawei, ZTE, and Hikvision. As a result, US telecom providers had to replace existing equipment suppliers and manufacturers across the industry.16

- Smaller, rural telecom providers felt the most pain, as they relied heavily on sourcing cheap Chinese telecom equipment.17

- Non-Chinese telecom equipment suppliers benefited, as suppliers such as Nokia (Finland) and Ericsson (Sweden) increased share of equipment sales.18

- US companies operating in China faced a harsher business environment, as China retaliated by limiting use of U.S.-made processors (Intel, AMD) and operating system software (Windows) in government computerss.19

RECHARTING THE MAP

The BIOSECURE Act is causing waves of disruption across the biopharma supply chain. While the scope and depth of impact remain unclear, we observe the industry is already making moves to de-risk their suppliers. As we look ahead, biopharma companies working with Chinese partners should be prepared for greater government scrutiny not just in biomanufacturing but in clinical partnerships as well.20 Those who plan for resilience today are positioning themselves for the shifting current and the ongoing disruption it brings.

Footnotes

1. Text - H.R.8333 - 118th Congress (2023-2024): BIOSECURE Act - Library of Congress

2. House passes bill that targets China biotechs - STAT

3. BIO survey reveals dependence on Chinese biomanufacturing - BIO

4. U.S. Scrutiny of Chinese Company Could Disrupt Supply Chain for Key Drugs - The New York Times

5. Chinese Firm is Cleared to Buy American DNA Sequencing Company - The New York Times

6. Anti-China bills portend massive blow to biotech - BioCentury

7. Impact of the US BIOSECURE Act on Biopharmas, Contract Services and Investors - LEK

8. WuXi Biologics Inte.rim earnings 1H 2024

9 Enzene opens continuous biologics manufacturing facility - Business Standard

10. Aragen setting up a $ 30 million bio-manufacturing site in India - Aragen Life Sciences

11. CDMO Siegfried expands US footprint with acquisition of Wisconsin facility - FiercePharma

12. Lonza Signs Agreement to Acquire Large-Scale Biologics Site in Vacaville (US) from Roche

13. Spain's Rovi receives offers for potential sale of €2B-plus CDMO group - FiercePharma

14. Agilent Technologies lays out $925M to acquire Canadian specialty CDMO Biovectra - FiercePharma

15. Millions could be harmed by sudden decoupling of Chinese CDMOs - FiercePharma

16. U.S. Moves to Ban Huawei From Government Contracts - The New York Times

17. Huawei business ban leaves rural wireless companies with few alternatives - The Washington Post

19. China blocks use of Intel and AMD chips in government computers - Financial Times

20. Lawmakers spotlight clinical studies in China - FiercePharma

Originally published 30 September 2024

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]