If your company is a profitable U.S.-based business engaged in sales of products or services to non-U.S. persons, it may be eligible for a tax incentive that can equate to up to 2% or more of the gross export sales. The incentive is known as the domestic international sales corporation, or "DISC." This newsletter explains how it might benefit your company.

Who can qualify

Any profitable U.S. company that –

- sells or leases products for use outside the U.S. where the exported products have no more than 50% foreign content by value; or

- performs engineering or architectural services for projects located (or proposed for location) outside the U.S.

may be eligible to use a DISC to avoid federal income tax on a portion of its income from the export sales. The incentive works for any type of company, whether a C corporation or a pass-through entity such as an S corporation, limited liability company, or partnership.

How it works

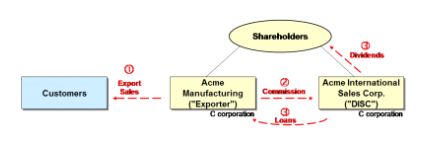

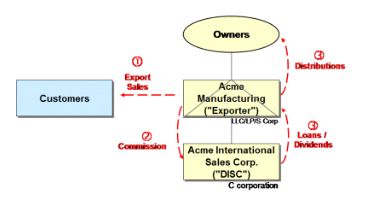

A U.S. company with qualifying export sales ("Exporter") or its shareholders form a U.S. corporation and elect DISC status for the corporation. Once the DISC is formed, Exporter enters into an agreement with the DISC to pay a commission to the DISC on all export sales. The commission is generally the greater of 4% of the qualified export receipts or 50% of the taxable income from the qualified export receipts. The commission can be calculated separately for each sale to maximize the commission to the DISC.

As export sales are made, Exporter pays commissions to the DISC and deducts the payment. The DISC pays no tax on the commission income. The DISC generally loans the commissions it receives back to Exporter, or purchases export receivables from Exporter. The DISC's shareholders pay an interest charge at a very low rate (0.24% for 2015) on the DISC's undistributed income. When the DISC distributes its income to its shareholders as a dividend, it is qualified dividend income eligible for a maximum federal tax rate of 23.8% for individuals; considerably less than the maximum rate of 43.4% on ordinary income.

Note that even though the DISC may be earning significant income from commissions, loans and export receivables factoring transactions, it has no employees and no physical assets.

Typical DISC arrangements for a C corporation and for a pass-through entity are illustrated below.

Figure 1 – C Corporation Structure

Figure 2 – Pass-Through Entity Structure

Benefits

If Exporter is a C corporation (Figure 1), using a DISC completely eliminates corporate income tax on Exporter's income paid as DISC commissions. Assuming a 4% commission and a 34% corporate tax rate, the benefit equates to a pre-tax equivalent cost savings of 2.06% of gross export sales (4% x 34% ÷ (1 – 34%)). The benefits can be greater for high-margin (>8%) products that can use the 50% of taxable income method for computing the DISC commission.

If Exporter is a pass-through entity (Figure 2), using a DISC converts Exporter's operating income paid as DISC commissions from ordinary income (43.4% maximum tax rate) to qualified dividend income (23.8% maximum tax rate), and the ability to defer recognizing that income until the DISC distributes it, with only a nominal interest charge for the deferral. Assuming a 4% commission and maximum tax rates, the benefit equates to a pre-tax equivalent cost savings of 1.39% of gross export sales (4% x (43.4% – 23.8%) ÷ (1 – 43.4%)), before taking into account the benefits of deferral. Again, the savings can be greater for high-margin products.

Costs

Because a DISC has no employees or physical assets, costs to implement and maintain a DISC are very modest. Companies with as little as $100,000 of annual export sales may benefit from a DISC.

Interested?

If your company is a profitable business that has significant export sales, and if it has not already implemented a DISC, it makes sense to investigate the potential benefits that may be available using a DISC. A more comprehensive presentation on DISCs is available on our website, here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.