On September 29, 2021, by a vote of 4-1, the U.S. Securities and Exchange Commission (SEC) proposed to expand the information that mutual funds, closed-end funds, exchange-traded funds (ETFs), and other registered investment companies must disclose about their proxy votes.1 Among other things, the proposed rules would require funds to tie the description of each voting matter to the issuer's form of proxy and categorize each voting matter. In addition, any person who files Form 13F (known as an "institutional investment manager") would be required to file Form N-PX to begin reporting proxy votes for the first time but limited to say-on-pay votes. The SEC says the changes would help investors to identify votes of interest and compare voting records, thereby increasing transparency. Public companies, institutional shareholders, funds, and investment managers all would be affected and will have potentially different views and interests as the rulemaking proceeds.

I. Background

The proposed requirements for reporting say-on-pay votes would complete rulemaking originally begun in 2010 in response to a direction to the SEC from Congress in the Dodd-Frank Wall Street Reform and Consumer Protection Act.2 Had the SEC limited itself to the mandated say-on-pay rulemaking, there likely would have been little debate among the Commissioners. Instead, the decision to revisit and expand Form N-PX generated significant discussion.

One Commissioner voted against the proposed package in its entirety based on a philosophical objection that Form N-PX already provides more information about proxy voting than is warranted by actual levels of interest in the topic by fund investors.3 Another Commissioner voted in favor of proposing the rules but pointedly said his vote should not be taken as support for final rules unchanged from the proposal. His statement highlights reservations with respect to (1) the proposed taxonomy for categorizing proxy proposals, which he said would be difficult to administer and could become dated almost as soon as published, and (2) the proposed requirement to report when securities are not voted because they are out on loan, which he said can give the impression that not recalling securities to vote them is problematic when it should be in the discretion of individual firms to reach their own judgments on the value of the vote.4

II. Proposed Additions to Form N-PX

1. Say-on-Pay Disclosures

Under the proposal, any person who files Form 13F also would now be required to file an abbreviated version of Form N-PX to disclose say-on-pay votes.5 An institutional investment manager would report annually on Form N-PX how it voted proxies relating to shareholder advisory votes on executive compensation matters over which the manager exercised voting power to influence a voting decision.6 If a manager did not exercise voting power over any securities that held say-on-pay votes during a given reporting period, the SEC proposes to require that the manager file a Form N-PX affirmatively stating this fact.

Importantly, the SEC suggests that a determination not to vote is itself the exercise of voting power, so that each such nonvote would be reported. This is notwithstanding comments to the original 2010 proposal noting that certain types of managers, high-frequency trading firms being a prominent example, may have determined and disclosed to their clients that they will not vote proxies.7

While being a reporting person for purposes of Form 13F triggers the potential application of these proposed rules for institutional investment managers, elements of the proposal deviate significantly from Form 13F. For example:

- Say-on-pay vote reporting by institutional investment managers would not be on Form 13F and instead would be on Form N-PX, a form historically used only by funds.

- Form 13F reporting is limited to "Section 13(f) securities," whereas this rule would not be.

- Form 13F has a de minimis exception for small holdings, whereas this rule would not.8

- Form 13F reports holdings as a quarter-end "snapshot," whereas this rule would require reporting votes of any position held at any time during the applicable reporting period (the result, of course, is that more portfolio holdings information would be reported).

- Form 13F requires disclosure of securities over which the reporting person exercises "investment discretion," whereas this rule would apply only to securities over which the reporting person actually made or influenced the voting decision (the result here being that the positions reported on Form 13F may differ from the positions with say-on-pay votes reported on Form N-PX).9

There are also three proposed versions of optional joint reporting that are broadly familiar to Form 13 filers and are intended to reduce duplicative filings. These would permit (1) a single manager to report say-on-pay votes when multiple managers exercise voting power; (2) a fund to report its say-on-pay votes on behalf of a manager exercising voting power over some or all of the fund's securities; and (3) affiliates to file joint reports on Form N-PX notwithstanding that they do not exercise voting power over the same securities. In all three cases, when another reporting person reports say-on-pay votes on a manager's behalf, the report on Form N-PX that includes the manager's votes would be required to identify the manager (and any other managers) on whose behalf the filing is made and separately identify the securities over which the nonreporting manager exercised voting power. The manager's report on Form N-PX also would identify the other managers or funds reporting on its behalf.

2. Voted and Loaned Shares

Currently, funds report only on matters as to which the fund was entitled to vote. The SEC proposes to apply the entitled-to-vote standard to portfolio securities on loan as of the record date for the meeting because the reporting person (whether fund or manager) has the ability to recall and vote them.

Further, under the proposal, the SEC would require disclosure of the number of shares voted and the number of shares loaned and not recalled for voting as of the record date of the meeting. This would include scenarios when the securities are loaned directly or indirectly through a lending agent but not when the manager is not involved in lending shares in a client's account.

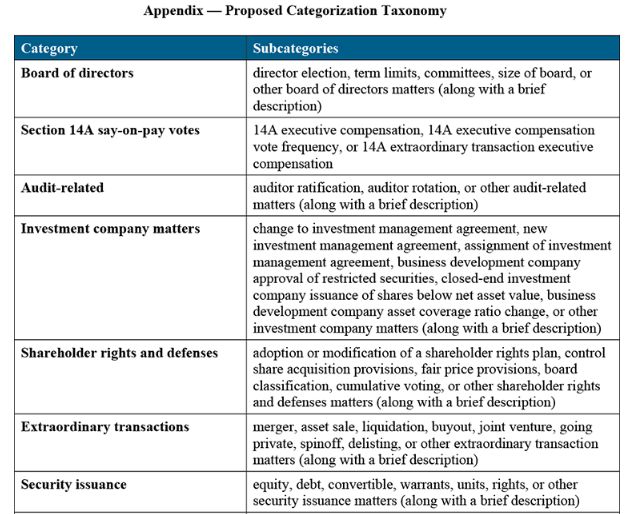

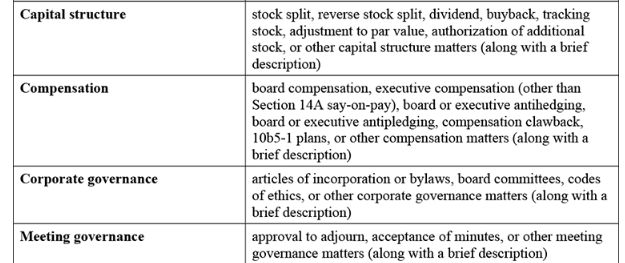

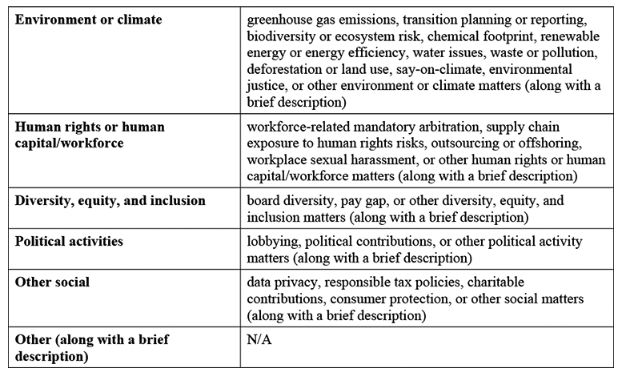

3. Categorization Framework

Funds would be required to list matters on which they voted under a standardized categorization framework. The appendix to this note lists the proposed categories and subcategories. A quick review will show that selecting among different categories and subcategories could be a regular challenge. Because the proposed categories and subcategories were derived solely from SEC staff analysis of the 2020 proxy season, one Commissioner noted that it also is possible that the listing could be skewed by the priorities of the current context and become dated quickly — especially given high levels of current attention to environmental, social, and governance (ESG) matters.10

4. Other Aspects of Amended Form N-PX

In addition to categorization, instructions to the form would require that funds do more to tie the description of voting matters back to the issuers' form of proxy and to categorize voting matters by type. Each voting matter would be reported in the same order as presented on the issuer's form of proxy.

Funds offering multiple series of shares (sometimes called series trusts in which each series is its own fund having its own investment program and shareholders) would provide Form N-PX disclosure separately by series. The SEC observes that this is a current requirement, but some funds simply note which series voted on which matters rather than organizing the entire report on a series-by-series basis.

The SEC proposes to amend the form to allow for additional information so long as it does not, by its nature, quantity, or manner of presentation, impede the understanding or presentation of the required information. Optional disclosure would be placed at the end of the cover page, or, if it relates to a particular vote, a reporting person could provide additional information about the matter or how it voted after disclosing the required information about that vote.

The SEC also proposes to amend the current requirement in Form N-PX that funds identify whether a matter was proposed by the issuer or by a security holder to also require funds to identify whether such matters are proposals or counterproposals. A technical amendment to Form N-PX would require reporting persons to disclose whether each reported vote was "for or against management's recommendation" (as opposed to "for or against management" as the form currently states).

Finally, to improve access to the information, reporting would be subject to structured data (electronic "tagging") requirements. Fund reporting also would be required to be available on a firm's website instead of filed solely with the SEC as today.

III. Confidentiality

Form N-PX (like Form 13F) is publicly filed via the EDGAR database on the SEC website. The SEC proposes instructions in Form N-PX to provide an opportunity to prevent confidential information protected from disclosure on Form 13F from being disclosed on Form N-PX.11 These instructions provide that a person requesting confidential treatment of information filed on Form N-PX should follow the same procedures set forth in Form 13F for filing confidential treatment requests. The SEC also prescribes the required content of a confidential treatment request and the required filing of information that is no longer entitled to confidential treatment. The SEC says that it believes confidential treatment for proxy voting could be justified only in narrowly tailored circumstances and explicitly states that it would not be justified solely in order to prevent proxy voting information from being made public.

IV. Compliance Dates

Proposed compliance dates would vary depending on when the amendments become effective but in general would provide that reporting be made only for periods six months after the effective date of the new form. The SEC offers several examples in the release, with the earliest presumed effective date being February 1, 2022, which would trigger reporting of votes occurring six months later, commencing August 1, 2022, for the reporting period commencing July 1, 2022. Because reporting under Form N-PX is made on a July 1–June 30 cycle, this example results in the first public reporting being for the 12-month period ended June 30, 2023, with the form due August 31, 2023. Notably, for managers who exceed the Form 13F reporting threshold during a calendar year (Y), as their initial Form 13F to report their fourth quarter of Y positions is not due until February 14 of the following year (Y+1), the SEC proposes that their initial Form N-PX reporting cycle will begin July 1 of Y+1, with their initial Form N-PX due August 31 of Y+2.

V. Our Take

The proposed rules may appear to be technical, but they present fundamental questions around the value of this kind of reporting (and from that, who should be required to report and in what kind of detail). Nor can disclosure ever be assumed to be purely neutral. Practices may evolve in response. For example, would the new securities-on-loan reports affect securities lending markets, or would operational burdens associated with proxy voting (again, just tracking say-on-pay votes would be a challenge for some managers) affect the relationship between investment managers and clients? There also are real prospects for confusion in aspects of the proposal — notably the proposed categorization requirements and the interplay between Form 13F rules and practices and those under Form N-PX. In this regard, the extension of scope to include Form 13F filers certainly will capture persons unfamiliar with Form N-PX, including certain hedge fund managers, family offices, and companies that manage their own pension funds.

Footnotes

2Securities Exchange Act Release No. 34-63123, 75 FR 66621 (Oct. 18, 2010).

3Statement of Commissioner Hester M. Peirce, Enhanced Reporting of Proxy Votes by Registered Management Investment Companies; Reporting of Executive Compensation Votes by Institutional Investment Managers (Sep. 29, 2021). To make her point, Commissioner Peirce said she would have voted in favor of at least circulating these proposals for public comment had the commission agreed to invite feedback on the following question:

5Form 13F reports quarter-end holdings in "Section 13(f) securities," generally being U.S. exchange-traded equities and certain options. An "institutional investment manager" is defined for this purpose as any person, other than a natural person, investing for its own account or having investment discretion over $100 million or more in Section 13(f) securities. It is important to recognize that the definition of an institutional investment manager is broader than some assume, as it does not require management of a securities portfolio on behalf of clients or customers. For example, corporations managing their own pension plans can be institutional investment managers.

6Say-on-pay votes are nonbinding shareholder advisory votes on executive compensation matters for public companies pursuant to Section 14A of the Securities Exchange Act of 1934 and generally include three categories: (1) approving compensation of certain named executives; (2) frequency of say-on-pay votes (every one, two, or three years); and (3) approving "golden parachute" compensation in connection with a merger or acquisition. 7For these types of firms, the requirement simply to track the occurrence of say-on-pay votes, so that they can then report on Form N-PX that they did not vote, will seem especially burdensome.

8Filers on Form 13F are permitted to exclude positions with a dollar value below $200,000 and consisting of less than 10,000 shares.

9Accordingly, for institutional investment managers two thresholds would apply. First would be whether the manager exercises "investment discretion" over Section 13(f) securities of sufficient value to be required to file Form 13F throughout the year; next would be whether the manager actually made or influenced the voting decision over a say-on-pay vote (including the determination not to vote, if applicable), and only this latter standard would trigger the proposed requirement to file Form N-PX. To illustrate, the SEC offers these examples in the release:

The focus on a manager's exercise of voting power could result in the manager's reports on Form N-PX differing from its reports on Form 13F. For example, if a manager exercises investment discretion over a particular section 13(f) security held in a client's account, but the client retains all rights to vote proxies for that security, the manager generally would report that security on its holdings report on Form 13F. However, it would not be required to report any say-on-pay votes with respect to that security. Conversely, a manager that exercises voting power over a security, but is not required to report the security on Form 13F because it does not have investment discretion over the security or because it did not hold the security at the end of a calendar quarter, would nonetheless be required to report say-on-pay votes on Form N-PX for that security.

10Roisman Statement.

11The SEC noted that confidential treatment would not be

available to funds that file Form N-PX and already disclose all of

their portfolio holdings.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.