NUMBER OF THE WEEK: 3

First it was three years, now it's three months. The Senate's attempt to pass a multiyear highway bill ran off the road this week after House Republicans announced they will adjourn one day early for the month-long August recess. The House's early departure forced the Senate to acquiesce to a short-term patch in order to keep the Highway Trust Fund solvent beyond July 31. The three-month patch is paid for by a collection of tax enforcement measures—the same offsets contained in a five-month patch the House passed earlier this month. The deal sets up the next collision of wills between the Senate and House in late October, when the debate over how to pay for a long-term highway authorization will bleed into the tug-of-war over how to handle tax extenders. Read more details below.

LEGISLATIVE LANDSCAPE

Kicking the Can Down the Crumbling Road. Majority Leader Mitch McConnell (R-KY) must have known that his multiyear highway bill faced tough odds with House leaders unimpressed with some of the Senate bill's offsets and staunchly opposed to an amendment reauthorizing the Export-Import Bank.

On Sunday night, the Senate voted 64-29 to attach the Ex-Im Bank amendment to the highway bill, sealing its fate. Just as the time for debate over the amendment and the underlying bill began ticking, the House unveiled a three-month patch and announced it would be jetting out of town before the Senate could even vote on its highway/Ex-Im Bank bill.

With a shutdown of highway and transit projects looming this Saturday, McConnell agreed to the three-month patch, which is expected to pass in the House today and in the Senate soon after. Although the temporary patch authorizes funding for only three months (through October 29) it contains the same offsets as the five-month extension bill that the House passed earlier this month. In other words, funding is in place to carry the Highway Trust Fund through mid-December if the House and Senate can't reach agreement (once again) on a longer-term bill by the end of October. Below is a summary of the key revenue provisions:

- Requires lenders to report additional information on outstanding mortgages to reduce inaccurate reporting.

- Clarifies that six-year statute of limitations applies in cases where the overstatement of basis results in a substantial omission of income.

- Requires estates with positive estate tax liability to provide the IRS with the value of property to prevent overstatement of value by beneficiaries.

- Modifies tax filing deadlines for partnerships, S corporations, and C corporations to increase accurate income tax returns.

- Allows employers to transfer excess defined-benefit-plan assets to retiree medical accounts and group-term life insurance.

- Extends current budget treatment of TSA fees, which reduces outlays by preventing the fees from being spent later.

- Lower taxes on LNG to 14.1 cents (from 24.3 cents) per gallon and LPG to 13.2 cents (from 18.3 cents) per gallon.

Boustany Set to Unveil "Innovation Box" Proposal. After the latest short-term highway patch expires, the House is expected to continue pushing for a longer-term funding solution that includes international tax reforms—including tax breaks for income generated from innovations (i.e. patents and other forms of intellectual property), known as an "innovation box" or "patent box."

Later today, Rep. Charles Boustany (R-LA) is expected to release his innovation box draft legislation. The idea has gained bipartisan momentum on both sides of the aisle recently, and Boustany's bill is co-sponsored by fellow House Ways and Means member, Rep. Richard Neal (D-MA).

Senate Finance OKs Two-Year Extenders Package. The Senate Finance Committee passed a two-year package last week by a vote of 23-3, extending more than 50 currently expired tax breaks for individuals and businesses for the 2015 and 2016 tax years. The $95 billion package includes the modified chairman's mark, along with two amendments adopted during the markup. One amendment, introduced by Sens. Grassley (R-IA) and Cantwell (D-WA), allows a tax credit for domestic biodiesel producers, and the other amendment, offered by Sen. Stabenow (D-MI), makes technical changes to the Mortgage Forgiveness Tax Relief Act. The modified chairman's mark also includes an expansion of the Work Opportunity Tax Credit (WOTC) to include credits for hiring the long-term unemployed as well as a provision providing parity for excise taxes on liquefied natural gas (LNG) and propane, on an energy equivalent basis. It also modifies the business expensing limits under Section 179 by indexing them for inflation. It is unclear when the full Senate will vote on the extenders package and whether the House will opt to follow the Senate's two-year approach, rather than holding fast to its preferred method of permanently extending a select few of the tax provisions.

Jeb Bush: Phase Out Energy Tax Credits. Following Senate Finance's approval of its extenders package, which includes more than a dozen of energy tax provisions, Republican presidential candidate Jeb Bush told an activist in New Hampshire that energy tax credits for oil and gas sectors should be phased out. "I don't think we should pick winners and losers. I think tax reform ought to be to lower the rates as far as you can and eliminate as many of these subsidies," Bush explained. While Bush's call to end fossil-fuel credits may have environmentalists cheering, they may not be so thrilled to hear that Bush would also like to put an end to tax breaks for renewables such as solar and wind: "All of them. Wind, solar, all renewables, and oil and gas."

Hillary Clinton: Renewable Energy to Power Every Home in 10 Years. The Clinton campaign is moving in the opposite direction of Bush when it comes to clean energy production, unveiling a plan that would see more than 500 million solar panels installed in the U.S. by 2011 and every home powered by renewable energy within 10 years. Clinton's "Clean Energy Challenge" would see to the implementation of the current administration's Clean Power Plan. Full of ambition, sparse on details – the clean energy plan is only one part of Clinton's comprehensive energy and climate agenda, which would be unveiled soon according to her campaign. Based on the campaign's fact sheet, Clinton would support the use of tax incentives to "extend federal clean energy incentives and make them more cost effective both for taxpayers and clean energy producers."

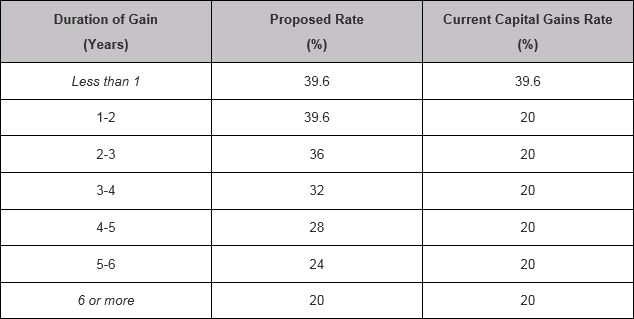

Clinton on Capital Gains. Clinton also announced changes she would support to incentivize longer-term investments by requiring high-income investors to hold onto investments for at least six years in order to receive the 20 percent long-term capital gains tax rate and a sliding scale for shorter holding periods. The proposal would only apply to income above the top tax bracket threshold (in 2015, $413,200 for single filers and $464,850 for joint filers). Investments held for less than two years would be subject to the current top rate for individual income (39.6 percent). Clinton believes that the plan would encourage long-term investments over short-term gains, boosting economic growth in the long run. But critics quickly pounced on the proposal, arguing that it would actually depress business investments overall. Read more critiques here.

Here is a breakdown of the rates on long-term capital gains under Clinton's plan:

REGULATORY WORLD

Proposed Regulation Narrowing Carried Interest. The IRS and Treasury issued proposed regulations last week limiting the use of private equity management fee waiver agreements from generating capital gains. Specifically, the proposed regulations provide that arrangements between partnership and partners that lack "significant entrepreneurial risk as to both the amount and fact of payment" should be treated as disguised payment for services. The purpose of these regulations is to prevent fund managers from shifting earnings from fee to carried interest. The IRS and Treasury did provide, however, that they would add an exception to the safe harbor interest for profits interest addressed in Revenue Procedure 93-27.

CBC Reporting Data Not Available to All. Country-by-country reporting will be between the U.S. and its partners in treaties and tax information exchange agreements for now, said an IRS official. Karen Cate, a senior international tax law specialist at the IRS, elaborated that limiting the reporting would allow the U.S. to protect the confidentiality of data. She emphasized the U.S. wants to make sure the data would be for assessing high-level transfer pricing risks, and not as a "substitute for detailed transfer pricing analyses of individual transactions." Outside of country-by-country reporting, the U.S. remains concerned about various developments of the OECD's BEPS project, according to Cate.

LOOKING AHEAD

Wednesday, 7/29

Senate Banking Committee

The Subcommittee on Financial Institutions holds a hearing on "Role of Bankruptcy Reform in Addressing Too-Big-To-Fail."

Thursday, 7/30

Senate Homeland Security Committee

The Subcommittee on Investigations holds a hearing on "Impact of the U.S. Tax Code on the Market for Corporate Control and Jobs." The hearing will explore the impact of the U.S. corporate tax code on foreign acquisitions of U.S. businesses and the ability of U.S. businesses to expand by acquisition.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.