- within Real Estate and Construction topic(s)

- in United States

- within Real Estate and Construction topic(s)

Luxury brands are grappling with a new reality. The initial optimism about their post-pandemic resilience has given way to a string of profit warnings and decelerating growth. Yet, amid the market slowdown, leading luxury groups like LVMH, Kering, and Chanel are strategically investing more capital into stores and real estate, with record-breaking property acquisitions in prime locations and investments in their existing stores.

The importance of stores and luxury real estate cannot be overstated. High-profile locations and the capital invested in design, fixtures, and product displays act as monumental advertisements for luxury brands. These coveted addresses and the subsequent investments serve a dual purpose: signaling the brand's prestige to attract discerning customers and forming a powerful barrier to entry for competitors, as the astronomical costs of acquiring and maintaining these locations effectively exclude brands without financial muscle.

The conversation has moved from "bricks vs. clicks" to how luxury brands can create seamless, experiential retail for customers.

The shift in investment strategy is a rebalancing, of sorts. The waning impact of the pandemic on luxury consumer behavior into the less profitable, higher growth digital channel, coupled with increasing cost of capital, has led to a pendulum swing toward more balanced investment into stores. Luxury brands are now reprioritizing their investments toward regional expansion, strengthening their physical retail networks, and redeploying capital into new and existing stores. Furthermore, the recent struggles of pure-play online luxury retailers only reinforces the point.

The power and profitability of physical stores endure. Despite their slower growth, they allow luxury brands to serve customers with a fully-integrated, experiential retail model, which is essential for the overall health of luxury brands.

Balancing exclusivity and demand in real estate: AlixPartners' six-point decision flow

Unlike mainstream retailers focused on maximizing customer reach through higher store counts, luxury brands navigate a delicate balance. Preserving brand desirability and exclusivity while growing the top and bottom lines remains the objective. However, store count oversaturation risks diluting brand prestige, while limited physical presence can hinder growth and profit potential. Questions beyond store count are also important: Where should those stores should be located)? What is the experience and role of the store itself? How much capital should be invested, and what economic returns are these stores expected to generate?

To navigate this tightrope, we have developed a decision flow for luxury brands to support the complex choices required. In our experience, a blend of strategic capital planning, data-driven store and real estate insights, and local market understanding is required.

#1: Where should we deploy our store capital, geographically (store location, macro)

Luxury brands must adopt a data-driven, dual-pronged approach to optimize store location and format. At a macro level, understanding wealth migration patterns is crucial. Recent wealth migration data shows wealthy and soon-to-be wealthy Americans moving from traditional hubs like New York and San Francisco to cities such as Miami, Austin, Scottsdale, and Nashville, driven by warmer climates, lifestyle changes, and tax benefits. Globally, cities like Dubai, Singapore, and Tokyo are attracting the world's wealthy, while London and Hong Kong face an exodus due to political and economic uncertainties. Luxury brands that are strategically located in these emerging hubs will thrive in this new era of wealth mobility.

#2 – 4: Micro-level precision is paramount for store location and format optimization

Answering the harder questions around store location and format requires a unique way of thinking. Long term success requires a data-driven approach to determine the trade areas to target, with optimal store formats and store quantities, to maximize a luxury brand's omni sales and ROI over time. At a lower level, an analytic approach provides the insights needed to understand the crucial match between customer and wealth demographics, and between location and omnichannel demand.

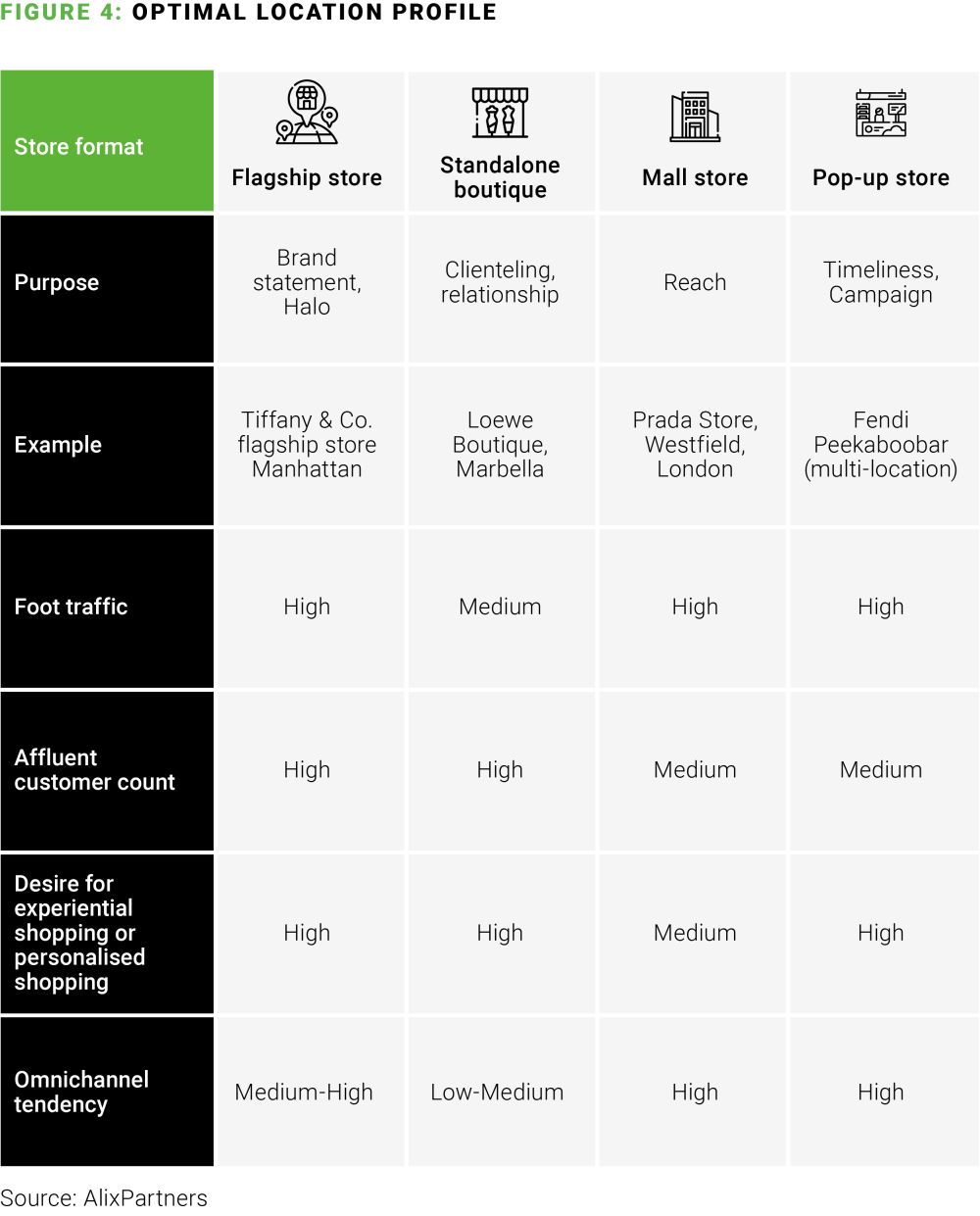

For example, after determining the target trade area, a typical luxury format decision is whether the store should be a dedicated men's or women's boutique, or a combined format? A proper assessment that thoughtfully merges real estate, demographic, competitive, brand, channel demand, store experience expectations, and financial data is the way forward. Whether a flagship, standalone, pop-up, or in-mall presence, the goal is to create a store that delivers maximum revenue and ROI, by aligning the numerous factors noted above.

The best luxury brands we work with are strategic and structured in how they think about aligning the factors. A simple table below shows one potential outcome. Starting with the store format and role of the store, the optimal location profile makes sense. A luxury brand's flagship store, with the role of acting as a brand statement and halo for other stores, will perform best in high foot traffic areas, attracting highly-affluent customers who desire both experiential and personalized shopping. When there is a mismatch between format and role, poor results follow.

#5: How much capital should we invest in our stores, and when?

Luxury store development and related capital decisions are unique. Whereas non-luxury brands and retailers often lead with financial analysis, luxury often leads with the store's design, aesthetics, experience, and most importantly, contemplation of how the store will elevate the image and brand. In this way, store designers and architects are allowed space, and capital, to be creative and inspire.

That said, luxury brands must be aware that constraints exist, especially when capital is deployed at scale and in a higher cost of capital environment. Issues can also arise because custom store development is the norm in luxury, making brands susceptible to long and costly development cycles. These are constraints no brand wants to face, luxury or otherwise, and this represents a significant consideration given the broader financial challenges faced in the Commercial Real Estate sector, explored in more detail in our recent report.

We are seeing luxury brands adapt. Higher sophistication is going into project planning and financial reviews, earlier in the development cycle. Additionally, metrics such as ROIC, sales per square foot, and time to completion are more prominent in luxury's planning language, providing a subtle counterbalance to softer design and experience criteria.

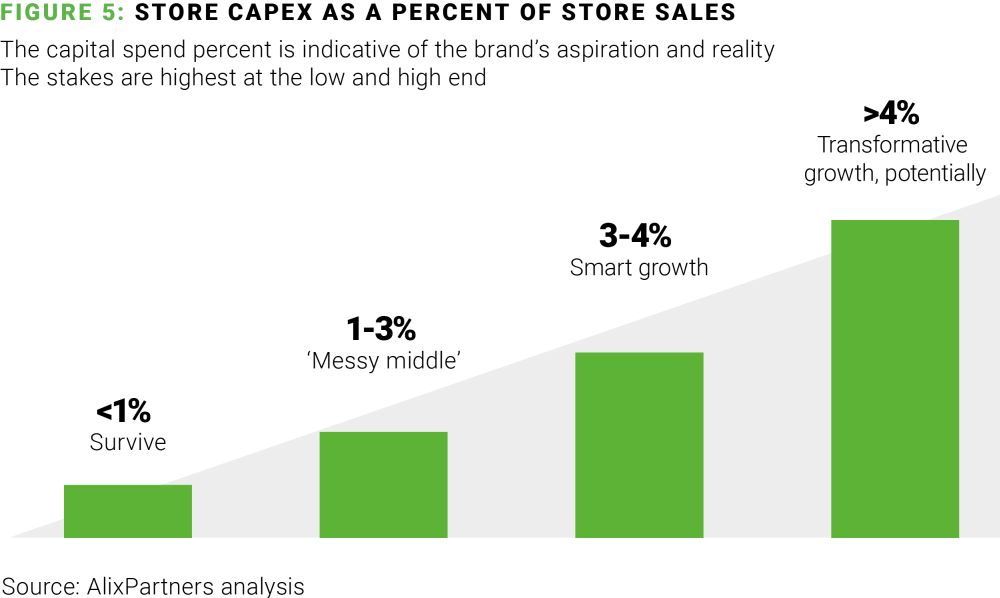

To this point, one method of answering how much capital to invest in stores is starting with a simple yet powerful metric: store capex as a percentage of store sales.

In our experience, store capex as a percentage of store sales works because it is indicative of brand's aspiration and reality. For brands, the stakes are highest at the low- and high-end tranches.

At less than 1%, it is about survival or in extreme cases. Financially distressed brands, or many brands during COVID, reduced their store capital to this level. This level, however, is not sustainable and will lead to worsening P&L.

The "messy middle" (or 1% - 3%) shows luxury brands that are growing steadily but maintaining their trajectory. Brands can invest in some but not all stores or make slight modifications to the experience. A steady P&L will follow.

"Smart growth" is the 3% - 4% tranche. Luxury brands here have aspirations, and capital is available. In this range, larger store projects can be undertaken, or true experience changes can be constructed chainwide. A stronger, higher growth P&L typically follows.

At the highest tranche of greater than 4%, store transformation is possible, potentially. These are the largest, image and brand changing bets. The risk is, of course, that when no limits or cost controls are in place, worsening ROIC is possible. If a brand invests at this level, where the highest returns are possible, careful attention must be paid each step of the way.

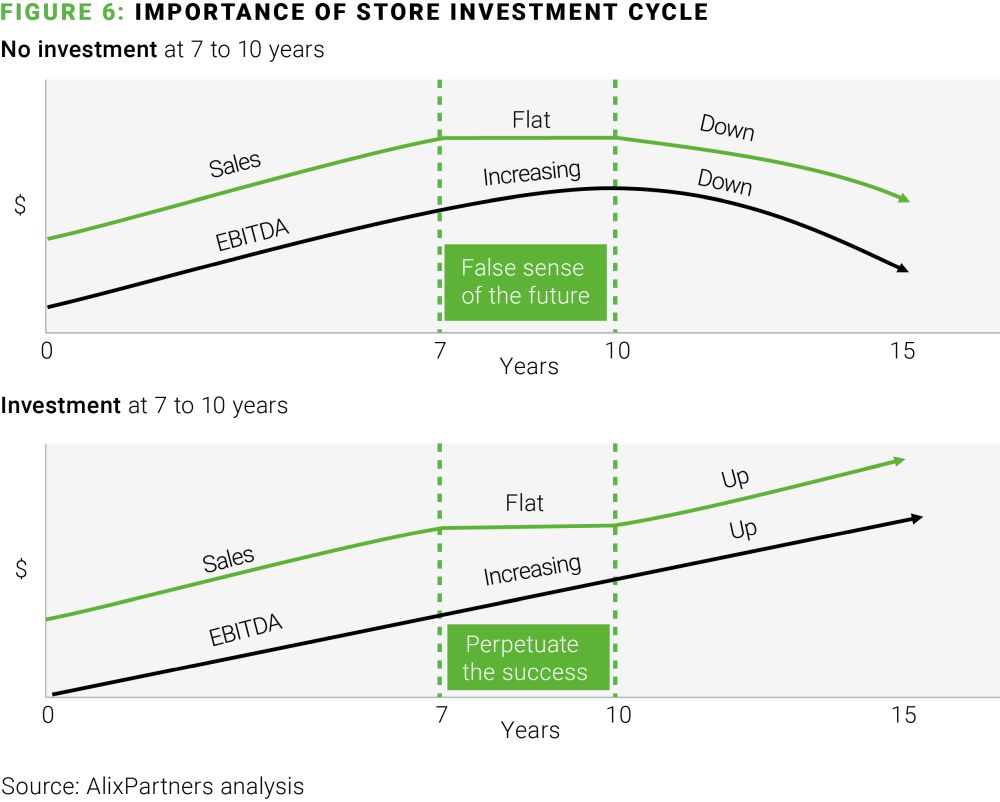

The question of when to invest in stores, especially for remodels, should not be overlooked. Luxury brands who deploy store capital in a timely manner—as measured in time since remodel—to achieve the highest, most consistent returns. The two charts below illustrate the point.

When a store reaches the critical 7–10-year window since the last remodel, a capital decision is required. Luxury brands who believe in the store but choose not to invest, often create a false sense of the future. While profits can remain high, the lack of investment starts the decline, from which it is difficult to recover. On the other hand, luxury brands who believe in the store and choose to invest often perpetuate the store's success. Profits are reinvested during the crucial 7-10-year window, and the next 7 to 10 years play out as before.

#6: How do we maximize the store's post capital deployment returns?

Given the escalating costs of new store builds, remodels, and retail operations, luxury brands cannot afford to see their stores be unproductive. Every dollar invested must see a return. While brand building and customer experience are foundational, return on invested capital (ROIC) remains the best metric for store capital efficiency.

To enhance ROIC, performance indicators such as incremental sales per square foot and incremental EBITDA after capital deployment are key. These metrics are the byproduct of a productive store environment, often indicated by increasing sales, conversion rates, and salesforce productivity. Here, the role of the customer-facing selling team is crucial. A luxury brand's ability to hire, train, and properly incent, along with the selling team's ability to grow customer relationships for the already affluent or aspirational, is the tell on whether the investment was worth it.

Ultimately, luxury success hinges on a delicate balance of aesthetics, exceptional customer experiences, and operational efficiency. The more aligned these elements are, the more luxury brands can solidify their financial position while maintaining their coveted brand image. In our next installment, we delve into specific strategies to maximize store performance. Stay tuned.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.