- with readers working within the Law Firm and Construction & Engineering industries

- within Wealth Management topic(s)

Introduction

The UK Takeover Panel (the "Panel") has introduced amendments to the definition of "acting in concert" under the Takeover Code (the "Code") and, in particular, the circumstances in which the Panel will presume parties to be acting in concert with each other. These amendments took effect from 20 February 2023 (Instrument 2022/6) and relate to changes in the treatment of groups of companies and investment entities.

The Code defines "persons acting in concert" as "... persons who, pursuant to an agreement or understanding (whether formal or informal), co-operate to obtain or consolidate control (as defined below) of a company or to frustrate the successful outcome of an offer for a company. A person and each of its affiliated persons will be deemed to be acting in concert all with each other". The definition includes categories of persons who are presumed to be acting in concert, which shifts the burden of proof on to such persons to rebut these presumptions (if applicable) in consultation with the Panel.

"Acting in concert" is a key concept in the operation of the Code since persons comprising a concert party are treated as one single person. This can be relevant for (i) disclosure of, and restrictions on, dealings in securities, (ii) setting a minimum amount, or a particular form, of consideration and (iii) the threshold at which a mandatory takeover offer may be required. While important for offerors and offerees, the framework for determining where persons are "acting in concert" and the latest Code amendments will be equally relevant for investors, including hedge funds and activist/arbitrage focused investors, to ensure their investments and engagement with other shareholders do not give rise to unintended consequences.

This note summarises some of the key changes implemented by the new amendments to the Code.

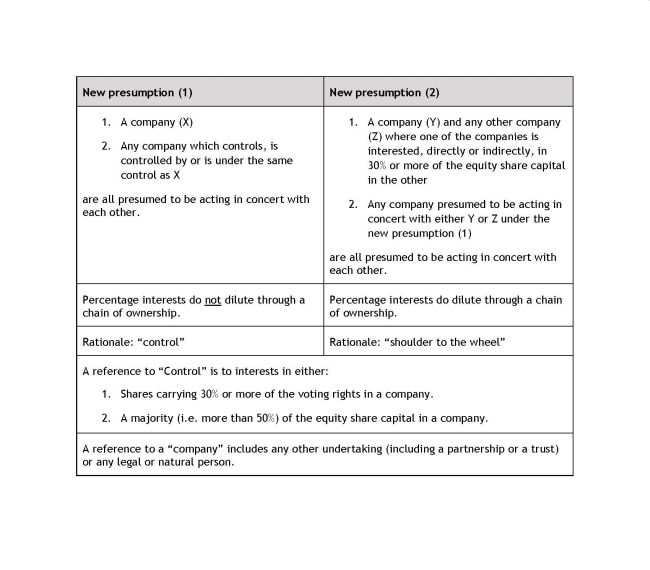

1. Threshold increase and inclusion of both voting rights and equity share capital

Old presumption (1)

Previously, companies were grouped, and presumed to be acting in concert with each other, by reference to the ownership or control of 20% or more of their equity share capital.

New Presumptions (1) and (2)

This approach has been revised by the introduction of the following new presumptions.

In practice, this means that the percentage threshold at which entities are "grouped" and presumed to be acting in concert has been raised from 20% to 30%. Further, the Panel will look at both voting rights and non-voting equity interests (including a limited partner's interests in a fund) when applying presumption (1) and presumption (2), and interests in the form of long economic interests (including derivatives or option positions) are also included towards the 30% threshold.

The key difference between the two presumptions (beyond the 50% / 30% thresholds) is that under presumption (1) the percentage interests do not dilute through a chain of ownership, whereas under presumption (2) they do dilute. However, multiple indirect interests (e.g. investments through various different funds) under presumption (2) must be aggregated.

The Panel has indicated a number of situations where presumptions (1) and (2) may be rebutted, including with respect to joint venture structures and government-owned entities. However, the Panel should be consulted in each case. Unless there is compelling evidence to the contrary, the absence of a relationship beyond being a passive shareholder, or a lack of knowledge of another's positions or intentions, is unlikely to lead to an upfront rebuttal of the new presumptions.

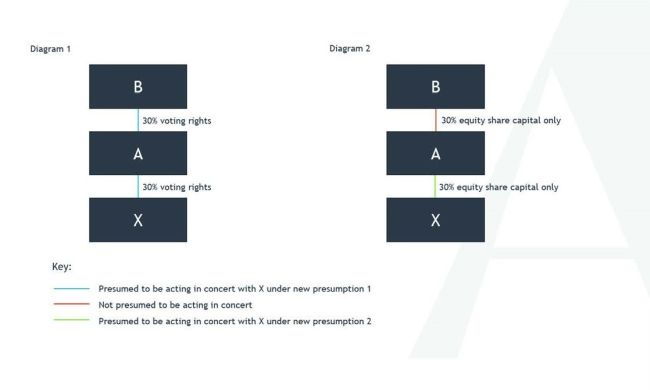

Examples

The following basic examples show how presumptions (1) and (2) work. The Panel's Response Statement (RS 2022/2) sets out some detailed examples showing how the new presumptions would apply in different scenarios.

- Diagram 1 illustrates the companies that would be subject to new presumption (1) by virtue of an interest in a company's shares carrying voting rights. Under new presumption (1), X would be presumed to be acting in concert with AandB (as percentage interests do not dilute through a chain of ownership).

- Diagram 2 illustrates the companies that would be subject to new presumption (2) by virtue of an interest in a company's equity share capital. Under new presumption (2), X would be presumed to be acting in concert with Abut notB (as B's indirect holding of X would be diluted through the chain of ownership to 9% (i.e. 30% multiplied by 30%)).

2. Key changes affecting funds, limited partnerships and fund investors

Application of presumption (1) and (2)

The Panel has confirmed that it will treat funds consistently with companies, with new presumptions (1) and (2) applying to a limited partnership interest in a fund (and therefore impacting investors in a fund) in the same way as non-voting equity share capital in a company.

Accordingly, where (a) a fund invests in a new "Bidco" formed for the purpose of making an offer or (b) acquires an interest in a Code company's shares, new presumptions (1) and (2) apply so as to presume (if the tests are met) an investor in that fund to be acting in concert with that newly formed Bidco or the fund itself, respectively.

However, in a scenario that does not involve an investment in a newly formed Bidco, the requirement to aggregate potentially multiple indirect interests (together with direct interests) is simplified as indirect interests in a fund or company will only be required to be aggregated (together with direct interests) where each link in the chain of interests represents 30% or more of the relevant fund's limited partnership interests or relevant company's equity share capital (as applicable).

New presumption (5)

An investment manager or investment adviser to an offeror, an investor in a new Bidco (formed for the purposes of making an offer) or the offeree, are presumed to be acting in concert with the offeror or offeree (as appropriate), together with any person controlling or controlled by or under the same control as that investment manager or investment adviser.

Interests in securities – treatment of discretionary funds

Old presumption (4), which provided that a fund manager was presumed to be acting in concert with a person whose investments it manages on a discretionary basis has been deleted. Now (i) a fund manager is treated as having an interest in securities which it manages for an investor in that fund on a discretionary basis; and (ii) an investor in a fund is not treated as interested in securities if it has given absolute discretion (or if not absolute, the fund investor has not retained such powers) to an independent fund manager regarding dealing, voting and offer acceptance decisions. Therefore, such investors would not be interested in equity securities for the purposes of presumption (2) but the fund manager would be.

3. Consortium offers

Investors in a consortium were previously treated as acting in concert with the offeror. The amendments to the Code expand this by providing that, where equity financing for an offer is provided by a fund managed on a discretionary basis by an investment manager or adviser, the following persons may be considered as acting in concert with the offeror: (1) the fund itself; (2) the investment manager or adviser to the fund; and (3) any investor in the fund who either: (a) will have a 'see-through' interest in 30% or more of the offeror; or (b) owns more than 50% of the limited partnership interests in the fund.

Where the investment manager or adviser, or the investor, is part of a larger organisation, the other parts of the organisation will usually be presumed to be acting in concert with that person and with the offeror. On a consortium bid, the Panel may be prepared to waive that presumption where the Panel is satisfied that those other parts of the organisation are independent, depending on the circumstances of the case, including the size of the investment in the offeror. The Panel have tightened the bands that it looks at when considering the size of the investment in the offeror as follows:

- 10% or less (no change): the Panel would normally agree to waive the presumption.

- More than 10% but less than 30% (down from 50%): the Panel may agree to waive the presumption depending on the circumstances.

- 30% or more (down from 50% or more): the Panel would not normally agree to waive the presumption.

The changes impact a wide range of market players, ranging from investment entities, government-owned entities, fund managers, private equity portfolio companies to joint ventures. For detailed guidance in respect of these specific entities, please refer to the Panel's Response Statement (RS 2022/2).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.