- within Litigation, Mediation & Arbitration and Compliance topic(s)

- in United States

- with readers working within the Business & Consumer Services and Healthcare industries

1. Introduction

The new failure to prevent fraud offence was introduced into the Economic Crime and Corporate Transparency Bill (the "Bill") during its progress through the House of Lords. Following our initial briefing regarding the proposed offence, we analyse the latest developments, key elements of the new offence (as currently drafted), areas of ongoing debate, and some practical illustrations of the implications of the new offence for companies who are planning the steps they may need to take in response to the new offence.

2. Parliamentary background and timing

The proposed new failure to prevent fraud offence follows a long-running debate regarding potential corporate criminal liability reforms, including, most notably, the Law Commission's options paper. The identified options included, among others, the introduction of a new failure to prevent fraud offence, and were discussed in our previous briefing. There are however certain differences between the Law Commission's recommendations and the Government's proposal, which are analysed further below.

The Bill did not initially contain a failure to prevent fraud offence, but the Government committed to add this following cross-party attempts to introduce a very broad-ranging offence during the Bill's initial progress through the House of Commons. The Government first proposed a failure to prevent fraud offence in amendments to the Bill on 11 April 2023, with further amendments proposed on 4 May 2023 by Lord Sharpe (Parliamentary Under-Secretary of State in the Home Office). A series of further draft amendments by Peers have also been debated, and on the whole rejected, and the Bill has now concluded in committee stage within the House of Lords. It will now move to the report stage before it returns to the House of Commons for consideration. This briefing considers the most recent version of the Bill as it has emerged from Committee, but it therefore remains subject to further amendment.

The Bill is expected to receive Royal Assent before Parliament rises for the Summer recess, on 20 July 2023. It is less clear when the offence will be brought into force. The Government's Economic Crime Plan 2 (the "Plan") suggests it will be "introduced" in Q3 2023, but this seems ambitious given the need for guidance to be drawn up (and, hopefully, publicly consulted upon) and for companies to prepare. We expect that Q4 2023 or, more likely, H1 2024, would be a more realistic timeframe.

Further information about the introduction of the offence can be found in the Government-issued press release, impact assessment (the "Impact Assessment") and factsheet (the "Factsheet").

More information about the Bill generally can be found in our previous briefing. More broadly, introducing a failure to prevent fraud offence is part of the Government's wider legislative reforms and its strategy aimed at tackling high levels of fraud and enhancing enforcement, as detailed in its Fraud Strategy (May 2023) and the Plan. Further reforms to the identification doctrine are also expected in due course (as referred to in paragraph 6.16 and Action 39 of the Plan), although they do not form part of the Bill.

3. Failure to prevent fraud: an overview

Our previous briefing summarised the key elements of the proposals.

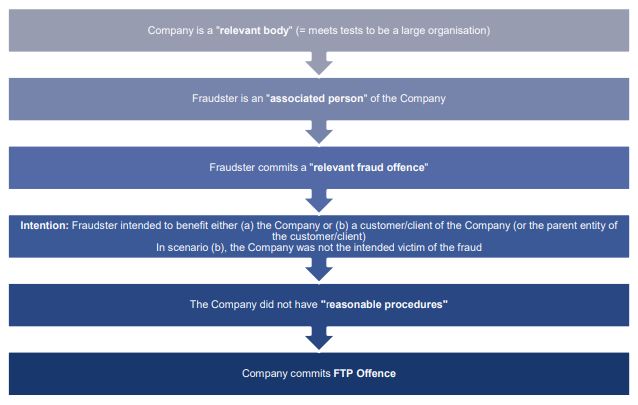

As a reminder, a corporate offence (an "FTP Offence") is committed where:

- an "associated person" of a "relevant body" commits a "relevant fraud offence" (all of these concepts are discussed further below);

- intending to benefit (directly or indirectly) the relevant body or any person to whom, or to whose subsidiary, the associate provides services on behalf of the relevant body; and

- the relevant body did not have in place reasonable fraud prevention procedures.

A relevant body can be a company or a partnership (and references in this briefing to a "company" or "corporate" are for convenience). However, the FTP Offence currently applies to large organisations only, defined (using the standard Companies Act 2006 definition) as organisations meeting two out of three of the following criteria: (1) more than 250 employees (2) more than £36 million turnover and (3) more than £18 million in total assets.

No FTP Offence is committed where the fraudster intended to benefit the client/customer of the relevant body, and the relevant body was itself a victim of the fraud offence (or was intended to be).

If convicted, an organisation may be liable to an unlimited fine

Further practical examples are provided in section 5 below, and the components of the offence can be illustrated as follows:

Click here to continue reading . . .

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.