The Implementation Act of the Arrangement between Korea and Taiwan for the Avoidance of Double Taxation and Prevention of Fiscal Evasion with Respect to Taxes on Income (the Korea-Taiwan Tax Arrangement) officially took effect on December 26, 2023, following endorsement by the National Assembly. For residents of the Republic of Korea, the benefits the Arrangement apply, in respect of taxes subject to withholding, on or after January 1, 2024, and in respect of other taxes, for tax years commencing on or after January 1, 2024. The key highlights of the Arrangement are as follows:

- The Background of Korea-Taiwan Tax Arrangement

Despite Taiwan's status as a significant economic partner in which over 100 Korean companies are present, the absence of a Double Taxation Avoidance Agreement (Tax Treaty) has been posing challenges for Korean companies and residents of high tax burden and instances of double taxation therefrom in the course of trade, investment, and interpersonal exchanges with Taiwan. In an effort to address this concern, both sides signed the 'Arrangement between Korea and Taiwan for the Avoidance of Double Taxation and Prevention of Fiscal Evasion with Respect to Taxes on Income' on November 17, 2021.

Although the Korea-Taiwan Tax Arrangement holds a formal status below the level of a Tax Treaty, its practical effects are equivalent to those of a treaty. This parity arises from the fact that the implementing legislation was passed by the National Assembly in the last December, ensuring the domestic implementation of the Arrangement.

- Key Takeaways for Allocation of Taxing Rights

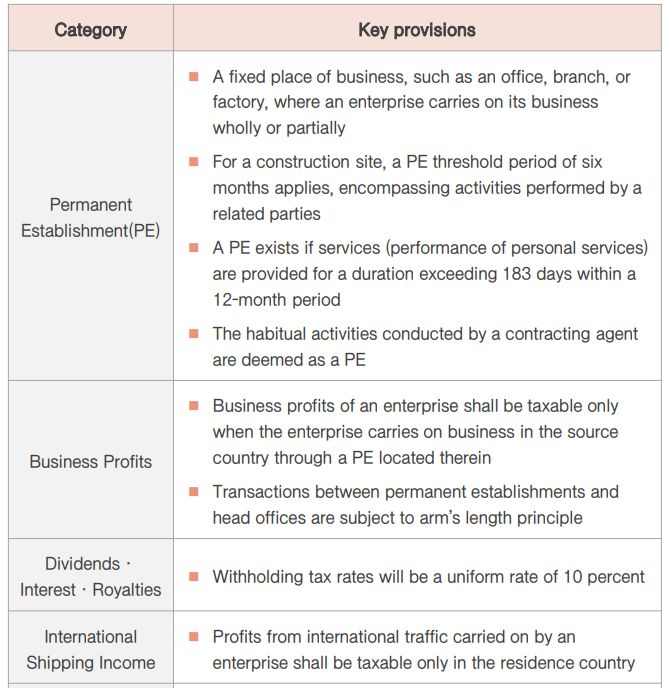

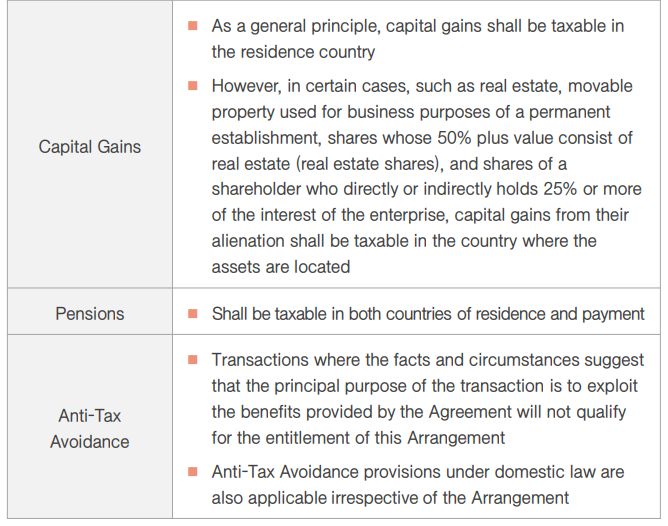

The provisions governing the allocation of taxing rights under the Korea-Taiwan Tax Arrangement are structured on the basis of the OECD Model Treaty, with some provisions reflecting certain elements of the UN Model Treaty. A concise summary of some key provisions is provided as below.

- Cooperation of Tax Administration and the Elimination of Double Taxation

The Korea-Taiwan Tax Arrangement, like other tax treaties, incorporates provisions safeguarding taxpayers and fostering administrative cooperation among tax authorities. These provisions encompass the Nondiscrimination in taxation on residents, permanent establishments, expense deductions, and capital ownership under certain conditions. The Arrangement further establishes a mutual agreement procedure designed to afford relief to taxpayers facing tax measures inconsistent with the agreement, including transfer pricing assessments. Additionally, it facilitates the exchange of information in connection with the enforcement of the Arrangement or domestic tax law.

With respect to the elimination of double taxation, Korean residents may offset the amount of tax paid or payable in Taiwan on their foreign-sourced income against their domestic corporate income tax or individual income tax (the direct foreign tax credit). Furthermore, if there is a dividend income from a Taiwan-based company in which the enterprise holds at least 25% interest, the credit for the enterprise shall take into account the Taiwan tax payable by the company in respect of the profits out of which such dividend is paid (the indirect foreign tax credit). It is important to note that in practice, the requirements for the indirect foreign tax credit under the Corporate Income Tax Law will likely apply which has a more favorable threshold of 10% shareholding (Article 57(4) of the Corporate Income Tax Law).

- Implications of Korea-Taiwan Tax Arrangement

As the implementation of the Korea-Taiwan Tax Arrangement starts in 2024, Korean companies operating in Taiwan will be able to compete on a level playing field with counterparts in Japan, Australia, Germany and other nations that have previously entered into Tax Arrangements with Taiwan while this Arrangement alleviates the tax burden and related double taxation in Taiwan for the Korean companies.

Specifically, in cases where a Taiwanese subsidiary of a Korean headquarters faces taxation in Taiwan due to transfer pricing, Korean companies will have the means to address the double taxation concern through the mutual agreement procedure. Furthermore, Korean companies operating in Taiwan will have the opportunity to leverage bilateral Advanced Pricing Agreement (Article 14 of the International Tax Coordination Law) with the tax authorities of both countries to mitigate transfer pricing risks that may potentially arise in both Korea and Taiwan.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.