With effect from 1st January 2024, Payment Service Providers ('PSPs') will face new record keeping and reporting obligations. These additional recording and reporting obligations will be introduced with the aim to combat VAT fraud associated with e-commerce.

IFR Champions Cup 2022

Who will be impacted by the new rules?

The new rules will impact PSPs as defined under Directive (EU) 2015/2366 ('PSD II') namely credit institutions, electronic money institutions, post-office giro institutions and payment institutions when the above mentioned entities provide payment services. Persons exempt in terms of Article 32 of PSD II will also be impacted by the new record keeping and reporting obligations.

In which scenarios will PSPs have the obligation to maintain records and make these records available to the VAT Authorities?

PSPs will be required to maintain records and report when they provide payment services that:

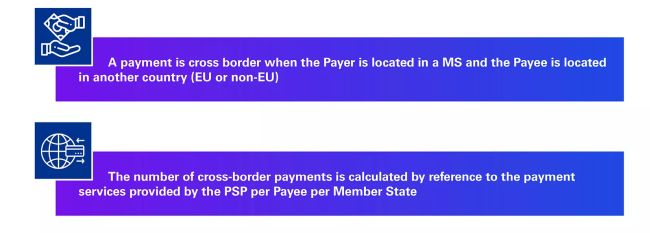

- qualify as 'cross-border payments'; and

- where in a calendar quarter the number of cross-border payments per payee per Member State exceeds 25.

The PSP of the Payer is exonerated from the obligation to maintain records and reporting if at least one of the PSPs of the Payee is based within the EU.

This means that:

There are no reporting obligations for PSP with respect to transactions where both the Payer and the Payee are based within the same EU Member State or where the Payer is based outside the EU.

In all the other circumstances, the PSP of the Payee providing payment services in respect of cross-border transactions is required to record and report the transactions. Where the PSP of the Payee is based outside the EU, this obligation shifts onto the PSP of the Payer.

What are the record keeping obligations under the new rules?

PSPs that provide payment services in respect to more than 25 cross-border payments per payee per quarter and that have the obligation to maintain records and report, will be required to keep records containing the following information in electronic format for a period of three calendar years from the end of the calendar year of the date of the payment:

- BIC or other code that unambiguously identifies the PSP

- Name of the payee, as it appears in the records of the PSP

- If available, any VAT ID Number or other national tax number of the payee

- IBAN or similar unique identification that gives the location of the payee

- BIC that unambiguously identifies and gives location of the PSP acting on behalf of the payee where the payee receives funds without having a payment account

- If available, address of payee as it appears in the records of the PSP

- Details of the cross-border payment and any related refund

namely;

- The date and time of payment or of the payment refund.

- The amount and currency of the payment /payment refund.

- MS of origin of the payment received by or on behalf of the payee, the MS of destination of the refund as appropriate, and the information used to determine the origin or the destination of the payment or the payment refund.

- Any reference which unambiguously identifies the payment.

- Where applicable, information that the payment is initiated at the physical premises of the merchant.

In addition to maintaining the records, PSPs will be required to make such records available to the tax authorities of the relevant MS through a new system – the CESOP.

KPMG's Observations

While the growth of e-commerce facilitated the sale of goods and services across various Member States, it has also provided fraudulent businesses with the opportunity of gaining an unfair market advantage by evading their VAT obligations. Given that the vast majority of online purchases made by consumers are executed through PSPs, the new rules are aimed at PSPs as they have access to information which once communicated to the tax authorities enables the said authorities to detect fraudulent businesses and control VAT liabilities.

Ahead of these rules, PSPs should review the manner in which information is currently being captured for regulatory reporting purposes and assess whether the system may require updating to capture the information necessary to fulfil the new recording and reporting obligations effective as from 1st January 2024.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.