The Indonesian Director General of Mineral, Coal and Geothermal

("Director General") issued Regulation No. 376.K

("Regulation 376.K"), which clarified

the restrictions on the use of related party mining services

companies under Law no. 4 of 2009 (the "2009 Mining

Law"). Regulation 376.K opens up the possibility of

up to five Izin Usaha Pertambangan (IUP) or Izin Usaha

Pertambangan Khusus (IUPK) concession holders using a related

party mining services company, which will enable a certain degree

of risk and cost sharing between investments.

Prior to the enactment of the 2009 Mining Law, related party mining

services companies had been commonly used for two purposes. The

first is to enable a foreign party to exercise a degree of

operational control over domestic companies holding kuasa

pertambangan (KP) concessions under the previous law. The

second purpose is to facilitate a degree of risk and cost sharing

between mining concessions.

The 2009 Mining Law rendered the first use redundant as it opened

up the new IUP concessions for direct foreign ownership. However, a

key principle of the 2009 Mining Law was to establish each IUP

concession as a separate company with a separate profit centre. As

such, a Ministerial Decree was enacted to restrict the use of

related party mining services companies without consent from the

Director General. Regulation 376.K provides additional colour to

the Ministerial Decree by granting approval for IUP holders to use

related party mining services companies in which the IUP holder

owns at least 20% of the equity.

In practice, the use of related party mining services companies

enables an owner of multiple concessions to offset profits from the

first producing concession against development costs for future

concessions. At the very least, this could result in a significant

deferral of taxable revenues - and in the event future concessions

proved to be unsuccessful, potentially setting the losses off

against profits from earlier successful concessions. By permitting

related party mining services companies to conduct the mines

operations, Regulation 376.K once again opens up this possibility -

although to some extent limited in its application.

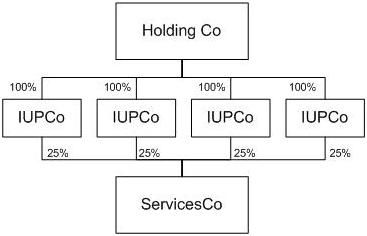

As Regulation 376.K requires each IUP holder to own 20% in the

related party mining services company, this limits the theoretical

number of IUP holders that can use the same service provider to

five. In practice, however, a 20% stake is unlikely to be

efficient, as post-tax dividend income from the mining services

company would be subject to taxation a second time in the IUP/IUPK

company level. For this reason, it is likely to be far more

efficient to pool services amongst four IUP holders each with a 25%

stake in the mining services company, thus enabling the IUP/IUPK

holders to rely on a participation exemption against double

taxation in portfolio companies. Accordingly, there is a practical

limit of four IUP/IUPK holders that can benefit from shared risks

and costs through one related party mining services company, with

an indicative structure as follows:

We believe Regulation 376.K opens up the potential to add a

valuable element of risk and sharing for holders of multiple

IUP/IUPK concessions through the use of related party mining

services companies.

Furthermore, the variety of sensible options available for mining

companies to share the risks and costs between multiple IUP/IUPK

concessions is enhanced by combining other structuring options such

as the use of common centres for equipment leasing and

financing.

O'Melveny & Myers LLP routinely provides advice to clients on complex transactions in which these issues may arise, including finance, mergers and acquisitions, and licensing arrangements. If you have any questions about the operation of the applicable statutory provisions or the case law interpreting these provisions, please contact any of the attorneys listed on this alert.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.