- within Accounting and Audit and Employment and HR topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Accounting & Consultancy and Transport industries

A. Taxation of various streams of income from AIFs:

AIFs has 3 different categories i.e. Category I (VC Funds, Debt Funds, etc.), Category II (PE funds, Real estate funds, etc.) and Category III (Hedge funds, etc.). Taxation in the hands of investors will vary based on the AIF category.

1. CAT I and CAT II

CAT I and CAT II have been granted pass through status for tax purposes i.e. income (other than business income, if any) is not taxed at fund level, but is taxed in the hands of the investors. Income in the hands of the investors is taxable in the same manner as if the income were accruing or arising to or received by such investor had the investments made by AIF been made directly by such investor.

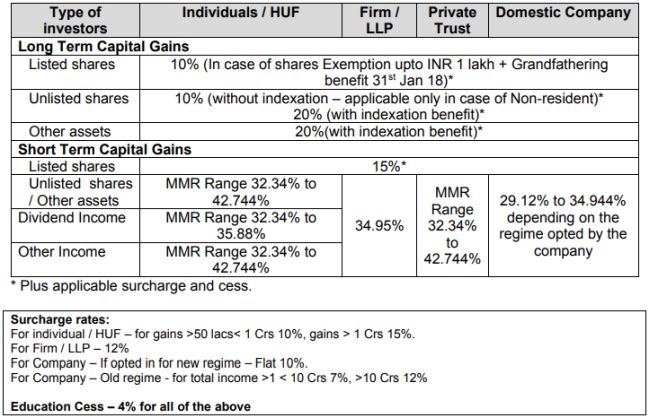

Thus, while the characterization of income would take place at the fund level, the taxation would be at the investor level. In case of investor the tax rates for various streams of income from AIF are summarized hereunder:

In case of non-resident investors, the above rates may be replaced by applicable beneficial DTAA rates on case-to case basis.

Furthermore, when income (other than business income) is distributed by AIF (CAT I & CAT II) to its investors, as per section 194LBB of the Income-tax Act, 1961 ('Act') the same is subjected to withholding tax:

- In case of resident investor, at the rate of 10%;

- In case of non-resident investor, rates under the Act or respective Double Taxation Avoidance Agreement (DTAA), whichever is beneficial

Business income, if any, is taxed in the hands of AIF at the maximum marginal tax rates applicable to such AIF as per the legal status of the AIF. Further, such business income would be exempt in the hands of the investor as per section 10(23FBB) of the Act.

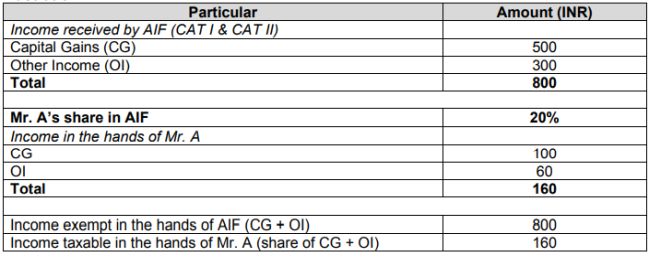

The below illustration provides the various streams and taxation in the hands of the investors:

Illustration:

CAT III have not been granted pass through status for tax purposes and income earned by such AIFs is taxed at fund level depending on the legal form of the AIFs. Indian regulations allows an AIF to be set-up either as a Company or a Trust or a Limited Liability Partnership (LLP).

The taxation in the hands of investors would be as under:

- Where the AIFs is set-up as a Company: An dividend issued by such AIF would be taxable in the hands of investor as dividend income (for rates refer the above table).

- Where the AIFs is set-up as an LLP: Share of profits from the LLP received by the investors would be exempt in their hands under section 10(2A) of the Act.

- Where the AIFs is set-up as a Trust: Taxability in the hands of the trust would be similar to indeterminate trust and thus its income would be taxable at MMR in the hands of the trust. As per section 86 of the Act, share of income from of the investor, who is a member of AOP/BOI, would not be included in his total income where such AOP/BOI is chargeable to tax at MMR.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.