- within Accounting and Audit and Employment and HR topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Accounting & Consultancy and Transport industries

The Finance Bill, 2017 had introduced the concept of 'secondary adjustments' in the Indian transfer pricing regime in order to align transfer pricing provisions with international best practices. Secondary adjustments in the books of accounts were envisaged to reflect the actual allocation of profits between a company and its Associated Enterprises (AEs) in the event of any primary transfer pricing adjustment.

The provisions that were introduced stated that if inter-company transactions were not at arm's length, the taxpayer is required to make a transfer pricing adjustment that is generally referred to as a 'primary adjustment'. Furthermore, if any primary adjustment results in an increase in the total income or a reduction in loss, it would warrant a secondary adjustment. The secondary adjustment would be in terms of repatriation of the excess money which is available with the AE (on account of the primary adjustment). In case the repatriation is not made (within the prescribed time), the amount of repatriation shall be deemed to be an advance made by the taxpayer to such an AE and the interest on such an advance shall be computed (in the manner as prescribed).

Rules for Computation of Secondary Adjustments:

In order to operationalise the secondary adjustments, the Central Board of Taxes (CBDT) has prescribed rules (vide notification no. 52/2017 dated 15 June 2017) for the time limit and the interest to be imputed which is as follows:

1. Applicability:

The provision shall be applicable to primary adjustments exceeding INR 10 million made in Financial Year (FY) 2016-2017 onwards.

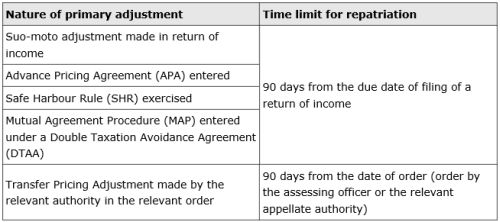

2. Time Limit for Repatriation:

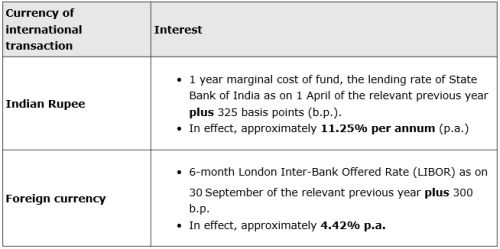

3. Interest to be imputed in case of failure to repatriate within the time limits mentioned above:

SKP's comments

- With this proactive follow-up within months of this initial notification, the expectations of the government are evident. This should provide guidance in ongoing litigation as well.

- The language of the initial provisions were ambiguous and created some doubt as to whether the conditions of INR 10 million and FY 2016-17 are cumulative or mutually exclusive. However, now it is clear that the provisions are mutually exclusive and as such, not applicable in case the primary adjustment value would be less than INR 10 million. This would bring clarity and relief to small multinational enterprises.

- The time limit of 90 days provided is also generally the average credit period that is across most industries. This should ensure an adequate time frame for overseas associated enterprises to arrange for the consequent repatriation to avoid any interest consequence.

- The interest rate that is to be imputed is also in line with the economic realities of the transactions, giving due weight to the currency of the transaction.

- Accordingly, taxpayers should start to relook at their inter-company transactions for the presence of any primary adjustments and determine the consequential impact of secondary adjustments.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.