- within Real Estate and Construction and Intellectual Property topic(s)

- with readers working within the Accounting & Consultancy industries

Mergers open doors for rapid inorganic growth, which is aimed at corporations across the world. We have seen what mergers are, their stages, types, and inbound and outbound mergers. July 2021 marked thirty years of economic reforms post which the companies in India were exposed to international competition. The late 1990s witnessed a trend of mergers in the Indian market. There are various kinds of mergers and motives behind each.

A reverse merger is also known as a reverse IPO (Initial Public Offering), where a private company acquires a publicly listed company.

The public company is a mere shell, and most shareholders are from private companies. We know that there are motives behind any merger, acquisition, or amalgamation, and such motives can be value creation which consists of revenue synergies and cost synergies. Other purposes include diversification, asset acquisition, and tax purposes. IPO can, at many times, be risky, time-consuming as well as expensive for the corporates that want to go public; they tend to choose other rapid growth methods, one of them being reverse mergers.

This article focuses on the procedure of reverse mergers, motives, and challenges that arise in the context of the Indian market and the approach of the judiciary towards the same.

The Procedure Followed

To understand how a reverse merger takes place, we first need to understand the approach of the private companies that aim for a reverse merger. Many public companies have shares already listed on some public stock exchange or over-the-counter (OTC) markets. These public companies are known as shell companies; they become targets of the reverse merger.

Then the private company buys at least 51% of the majority of the shares of the shell company. After this, the shares of the private company are swapped for the new shares of the public company acquired. There is no capital raised in a reverse merger like an IPO. Therefore, less time is required for the paperwork. This way, it becomes easier than a conventional IPO.

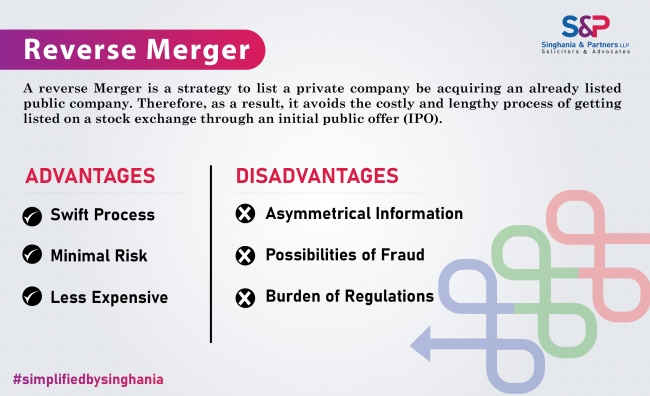

The Pros and the Cons

The advantages of a reverse merger include less expenditure as the deal is between a private and public shell company and there is no need to create a hassle. It involves multiple parties like investment banks in between. Although it is referred to as reverse IPOs, the profit is not dependent on the market conditions like in the case of IPOs. The disadvantages are there is risk involved; therefore, due diligence on a reasonable scale is required for the interest of everyone. There is also additional regulatory compliance to be followed in case of reverse mergers, as we will see below.

The Indian Scenario

There are various examples of reverse mergers in India which go as far back as the year 1994 when Godrej Soaps did a reverse merger with its loss-making subsidiary unit "Gujarat Godrej Innovative chemical" and adopted the name 'Godrej Soaps Ltd.' This was one instance when the company retained the name of the loss-making company.

Another example is that of ICICI group, which did a reverse merger with its offspring, ICICI bank, with the aim of becoming the largest bank became second largest in India. This merger brought various developmental institutions into the domain of retail banking. K.V Kamath, the founder, internally code this merger as a 'project dream.'

The Role of Reverse Mergers

If we consider the point of view of a layman, for him or her merger might appear as a mere way to achieve the same goal. Here, it becomes essential for us to understand why reverse mergers are important. One of the many motives is tax saving; there are provisions that permit the combined entity to pay lower taxes.

In India, Section 72A1 of the Income tax Act, 1961, is framed in a manner to support the sick companies by merging with healthier industrial companies by giving tax incentives. Section 72A states that amalgamation must be between companies, and none of them should be a firm of partners or sole proprietors. The incentive under this section is not given to companies engaged in trading activities or services, and an application must be given to a "specified authority" for recommendation to the Central Government to grant relief if satisfied.

The conditions of Section 322of the Act, which carries forward unabsorbed depreciation, should not be violated. The loss must be from "Profits and Gains from business or Profession" and not under capital gains or speculation. After the amalgamation, the sick company or the shell company should survive. The amalgamation must be in the public interest; in the end, it should be aimed to safeguard the interest of consumers, employees, shareholders, and promoters of the company.

Companies Act and SEBI: A look at the regulatory framework

The Companies Act of 1956 did not restrict or prohibit reverse mergers in any manner, but the Companies Act of 2013 seeks to put certain restrictions on backdoor IPOs or, in other words, reverse mergers. Section 232(h)3 of the Companies Act 2013 states that in case of amalgamation between a listed and an unlisted company, the final entity will be treated as an unlisted company. This provision is significant as it prevents private companies from getting the benefits of publicly listed companies through the backdoor. Under the Companies Act of 2013, listed companies that were supposed to undergo mergers needed approval from the Court and stock exchange.

Now, the Securities and Exchange Board of India (SEBI), through its circulars dated 4th February 2013 and 21st May 2013, clearly stated that listed companies undergoing mergers need mandatory approval from SEBI. Now there are stringent requirements for listed companies that intend to go through mergers. As per the current situation, the reverse merger is not prohibited but is strictly regulated by the Companies Act 2013 and SEBI.

Conclusion

Reverse mergers are also known as backdoor IPO. It opens doors for sick companies to recover, save time, and also provide tax incentives. Earlier, there were no strict regulations over reverse mergers in India, but now with the Companies Act, 2013 and SEBI regulations, there are strict regulations to ensure private companies do not reap benefits like publicly listed companies.

Reverse mergers are a quick way of corporate restructuring, but risks come with profit. The Parliament intends to protect the public and ensure that these mergers are for the entity's overall development and public welfare.

Footnotes

1. The Income Tax Act, 1962, § 72A, No. 43, Acts of Parliament, 1962 (India).

2. The Income Tax Act, 1962, § 32, No. 43, Acts of Parliament, 1962 (India).

3. The Companies Act, 2013, § 232(h), No. 18, Acts of Parliament, 2013 (India).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.