Trade credit insurances play a vital part in corporate finance in the German market. Yet the important role of credit insurers in restructuring scenarios is underestimated by many companies and their advisors. We examine what a trade credit insurance is and why it is important to keep insurers close in special situations.

German Mittelstand: Stakeholders in traditional corporate financings

It is often thought that stakeholder management in restructurings is all about shareholders, banks, funds and noteholders. This may largely be true of conventional financial restructurings of SPVs or BondCos. Many modern corporate financing structures and reorganisations focus on the lending-specific vehicles above the operating entities. Their complex structures and prevalence tend to draw the industry's attention and we are familiar with cases heavily steered by traditional lenders and professional investors, as recently seen in the restructurings of Vroon, Adler, ED&F Man and Aggregate.

Despite this, numerous production and trade focussed companies - particularly in the mid-market - rely on less sophisticated financing structures. In Germany, corporate finance typically consists of a larger volume syndicated credit facility, with a lower volume of current account facilities, multiple shareholder loans and in some cases corporate bonds or publicly subsidised loans. Other common financing methods include factoring and leasing. In Germany, large parts of the mid-market industrial and manufacturing companies (which are still considered the backbone of German economy - so-called Mittelstand) are financed using this structure. Often the parent or holding company - and in some cases even the operational entities - serve as borrowers. In a restructuring scenario, this commonly results in situations where there are far more stakeholders at the table than merely financial creditors. While the bank syndicates and noteholders remain the most active and demanding creditors, the involvement of public institutions which provided subsidised loans as well as the company's key suppliers frequently add layers of complexity to the stakeholder management process.

One stakeholder group which is often overlooked are the credit insurers. Not only do they play a significant role in the day-to-day business of producing and trading companies, in a financial distress scenario the inherent power of credit insurers can determine the success of the restructuring. Therefore, it is important to take a closer look at what credit insurances are, at their role in the corporate finance landscape, and how effectively to engage them in restructuring negotiations.

What is credit insurance?

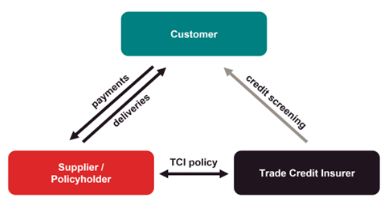

In addition to traditional lending, companies commonly utilise their suppliers as another source of financing. Upon delivery of goods or services, suppliers grant their customers certain payment targets or 'trade credits'. The length of payment targets varies significantly between industries, but in general is between 30 and 90 days. During the period between delivery and payment target, the supplier bears the risk of default. The supplier typically insures this risk by way of credit insurance, or more specifically a trade credit insurance policy (TCI policy).

If a customer defaults on its payments, the policyholder can claim the sum of the outstanding receivables from the credit insurer. The insurer continuously monitors the creditworthiness of the policyholder's customers. An unfavourable rating as a consequence of a customer's financial difficulties usually prompts an amendment of the TCI policies with respect to this customer. The credit insurer issues a notification to the policyholder who supplies to that specific customer that, with respect to forthcoming deliveries, the corresponding default risk is no longer covered by the TCI policies. The company can react accordingly and, for example, cease to grant payment targets, instead opting to demand prepayments for any new deliveries. However, an amendment of the TCI policy cannot relieve the credit insurer from coverage of any payment defaults relating to prior deliveries.

To mitigate their commercial risk, credit insurers assign a limit to every policyholder's customers. This customer-specific limit is based on its creditworthiness and defines the aggregate volume of receivables which is covered by all TCI policies of the relevant insurer. These limits play a pivotal role in the way a company can manage its cash positions: the lower a supplier's credit insurer rates a customer's creditworthiness, the more limited that customer's capabilities will be to use trade credits to manage its cash flow.

Why credit insurers matter in situations of financial distress

It is clear that a credit insurer's rating of a customer indirectly impacts the liquidity of the customer, who otherwise has no links or contractual arrangements with the credit insurer. This has additional consequences.

The German Insolvency Code refers to the state of insolvency or illiquidity (Zahlungsunfähigkeit) where a debtor is unable to meet its payment obligations as they fall due within a three-week period, indicating a lack of readily available funds to satisfy its debts. Where a debtor is in financial distress, a successful restructuring will depend on the debtor's ability to maintain sufficient liquidity to avoid insolvency while undertaking negotiations with relevant stakeholders and engaging advisors to prepare a restructuring opinion. Under German law, the latter is required to enable lenders to make a qualified and founded decision on whether or not to support the company within the restructuring period, e.g. by way of a restructuring loan. However, the reduction or cessation of the credit insurer's limit and the subsequent demand by the supplier for cash in advance in many cases will result in an immediate collapse of the relevant customer's short-term liquidity. This has the potential to force the debtor into insolvency proceedings.

While credit insurers and suppliers are entitled to mitigate their risk, it is clear that the credit insurance position may tip a company into insolvency and therefore this factor should not be underestimated.

How to handle TCI related risks in corporate restructurings

In general, the limits assigned to specific customers by the credit insurers are confidential. Insurers usually have no incentive to disclose limits to their policyholder's customers. A common risk associated with this is that the insurer may silently reduce or cease their limits in the early stages of a company's financial difficulties. Much like banks, credit insurers maintain sophisticated and well-connected risk departments.

A reduction or cessation of the TCI limits can have a negative impact on short-term liquidity. It can even limit a company's ability to maintain its operations if it does not have sufficient liquidity to make prepayments on essential goods and services. This is why it is crucial to involve credit insurers in the restructuring process at an early stage. This should be best practice not only for directors but also for banks and other creditors, as well as restructuring professionals. This can be achieved by proactively providing them with the same comprehensive information on financials and the state of the restructuring process as the lending banks and other stakeholders. We sometimes see credit insurers invited to attend 'all lenders' meetings which seek to update the financing parties on the restructuring process. This is typically welcomed by credit insurers.

In Germany it is a common practice in out-of-court restructurings for all relevant stakeholders to make a contribution in order to avoid the debtor's insolvency. For finance parties this might involve an extension of credit maturities and/or deferral of repayments or in some cases interest.

It is reasonable to expect credit insurers also to contribute to the company's restructuring. Because amending the TCI policy does not eliminate liability for payment defaults on deliveries already made, an insolvency of the customer inevitably cements its payment default up to the prior TCI limit, which the credit insurer must then pay out on. In principle therefore, making a contribution can mitigate the insurer's risk in relation to their existing exposure. Such contribution will typically involve providing as large a TCI limit as necessary to allow the customer to meet the planning assumptions in its restructuring report.

Key takeaways

Due to the large number of creditors and stakeholders often involved in a restructuring, effective stakeholder management and process control are vital to finding solutions and saving time and costs. Trade credit insurances are an indispensable corporate financing component for SMEs in the German market. Even without direct contractual relations with the debtor, they constitute stakeholders who should be treated accordingly. Having credit insurers at the finance parties' table from the outset can give company's an advantage in successfully resolving solvency crises.

Co-authored by Martina Rabe, Senior Consultant, Frankfurt

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.