In connection with the Indonesia's payment system reformation as outlined by Central Bank of Indonesia ("BI") on its Payment System Blueprint 2025, BI has issued three new regulations which applicable to (i) Payment Service Operators/Penyelenggara Jasa Pembayaran ("PJP") and, (ii) Payment System Infrastructure Operators/ Penyelenggara Infrastruktur Sistem Pembayaran ("PIP"). The objective of these new provisions is to establish a safe, reliable, and economical electronic payment ecosystem.

We have prepared below the list of Frequently Asked Questions regarding the new provisions sets out by BI for Indonesia's payment system operator.

1. What are the legal frameworks for payment system operator set out by BI?

The legal framework for payment system operator issued by BI are as follows:

- BI Regulation No. 22/23/PBI/2020 on Payment Systems;

- BI Regulation No. 23/6/PBI/2021 on Payment Service Operators ("PJP Regulation"); and

- BI Regulation No. 23/7/PBI/2021 on Payment System Infrastructure Operators ("PIP Regulation").

((i), (ii), and (iii) together referred to as "Payment System Regulations")

The enactment of PJP and PIP Regulation as of 1 July 2021 has revoked and replaced the following regulations:

- BI Regulation No. 18/9/PBI/2016 on Regulation and Supervision of Payment System and Rupiah Currency Management; and

- Licensing provisions on PBI 14/23/PBI/ 2012 on Money Transfer.

Furthermore, any implementing regulation of the following regulations shall remain valid for the next 1 (one) year as long as it is in conformity with the new Payment System Regulation:

- BI Regulation No. 11/11/PBI/2009 on Operation of Card-Based Payment Instruments and its amendments;

- BI Regulation No. 18/40/PBI/2016 on Operation of Payment Transactions Processing;

- Bank Indonesia Regulation No. 19/12/PBI/2017 on Operation of Financial Technology; and

- Bank Indonesia Regulation No. 20/6/PBI/2018 on Electronic Money.

2. What are the activities of PJP and PIP?

PJP: Pursuant to Art. 2 (1) of PJP Regulation, a PJP may carry out the following activities:

- Account Information Services/Penyediaan Informasi Sumber Dana, which include providing account information based on the users' authorization for the payment initiation purposes ("Activity 1");

- Payment Initiation and/or Acquiring Services, which include transmitting of payment transaction ("Activity 2");

- Account Issuance Service/Penatausahaan Sumber Dana, which include authorization of payment transaction ("Activity 3"); and/or

- Remittance services, which include acceptance and execution of fund transfer instruction, in which the sources of funds were not invented from remittance service operator. ("Activity 4").

PIP: BI provides that, PIP may carry out these two activities:

- clearing services, including, reconciliation, confirmation, and calculation of PIP members' rights and obligation prior to the settlement process; and/or

- settlement services, including, execution of settlement, which is final and binding, by debiting and crediting the PIPI members' account based on the clearing process (Art. 2 (1) of PIP Regulation).

To operate as a PJP, the operator must first obtain business license from BI, meanwhile the PIP must be appointed by BI.

3. How does the new BI regulations provide the PJP/PIP licensing regime?

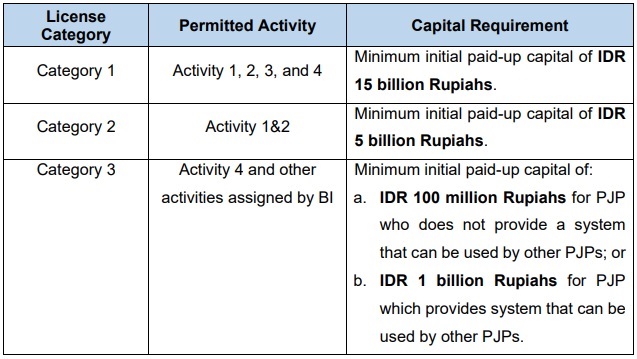

PJP licensing: BI classifies PJP licensing into three categories, each category has different capital requirement, detailed as follows:

Note: Any PJP in the form of bank ("PJP Bank") shall continue to subject to applicable capital requirements pursuant to the prevailing laws and regulations on banking sector (Art 24 (3) PJP Regulation)

PJP licenses shall remain valid unless if it is being revoked. BI as the issuer of PJP license, reserves the right to evaluate each issued PJP license in every three years or at any time if deemed necessary.

PIP Appointment: Pursuant to Art. 26 (2) of PIP Regulation, a prospective operator must fulfill the minimum initial capital of IDR100 billion Rupiahs to be appointed as PIP by BI.

Fit and Proper Test by BI: During the application process for PJP license or PIP appointment, BI may carry out a fit and proper test to: (a) any shareholders with 25% share ownership or shareholders with effective direct/indirect control over PJP/PIP; and (b) prospective directors & commissioners of PJP/PIP.

Approval or Reporting of Payment System Development Activities: The new Payment System Regulation requires any development and cooperation arrangement of payment system services/products to be approved or reported to BI.

If the developments or arrangements are deemed to be low risk, the PJP/PIP players shall file a report of the same to BI. However, PJP/PIP must first secure BI approval prior to implementing a medium or high-risk development to its payment system.

4. Is there any limitation foreign ownership limitation for PJP and PIP players?

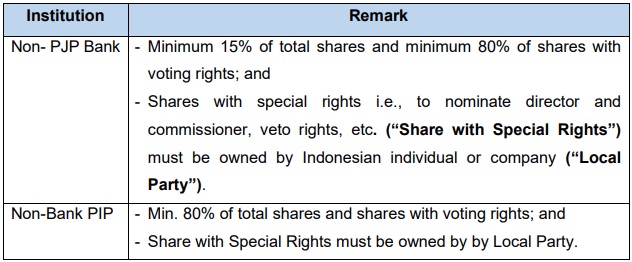

To promote Indonesia's payment system innovation whilst still ensuring consumer protection, BI stipulates that PJP and PIP players are subject to the following shareholding structure and domestic control requirements:

In addition to the above, BI on its sole discretion, is allowed to set out further assessment on the share ownership and control to prospective PJP and PPI.

5. What are the implications of the new Payment System Regulation to the Existing PJP/PIP license holders?

The following are implications of new Payment System Regulation to the existing PJP/PIP license holders:

- Existing PJP/PIP must increase its initial paid-up capital to comply with the new Payment System Regulation; and

- BI will conduct assessment and conversion to the existing PJP license/PIP appointment to comply with new Payment System Regulation. BI will conduct further evaluation such existing license holders in the next 2 or 3 years to decide whether such licenses/appointments will remain valid or shall be revoked.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.