- in Europe

- with readers working within the Business & Consumer Services industries

3. Taxation of partnerships and other Entities

3.1 Partnerships

In a general partnership (in Danish, termed an interessentskab or I/S), the partners are jointly and severally liable for the obligations of the partnership. Both individuals and legal entities may be partners. The partnership and the relationship between the partners are governed by a partnership agreement and by the general principles of Danish law. General partnerships are also subject to the rules of the Danish Business Enterprises Act (Lov om Erhvervsdrivende virksomheder) governing business names and powers of procuration, etc. General partnerships in which all partners are limited companies or similar companies must be registered with the Danish Commerce and Companies Agency.

A limited partnership (in Danish, kommanditselskab or K/S) consists of one or more general partners and one or more limited partners. Both general and limited partners may be individuals or any kind of legal entities. A general partner has unlimited liability, whereas a limited partner's liability is limited according to the provisions in the partnership agreement. The limited partnership and the relationship between the partners are governed by a partnership agreement and by the general principles of Danish law. Like general partnerships, limited partnerships are also governed by the rules of the Danish Business Enterprises Act (Lov om Erhvervsdrivende virksomheder). A limited partnership in which all partners are limited companies or similar companies must be registered with the Danish Commerce and Companies Agency.

A general or limited partnership, as such, is not liable to pay Danish tax. The partnership is transparent for tax purposes and taxes are levied on the individual partners in proportion to their shares in the partnership.

Depending on the nature of the business carried on by the general partnership, a permanent establishment may be held to exist in Denmark. In that case, all partners who are not already subject to full tax liability will be subject to limited tax liability on income and capital gains derived from the permanent establishment.

3.2 European Economic Interest Grouping (EEIG)

An EEIG may be established in the pursuance of EC Regulation 2137/85. The parties to an EEIG are jointly and severally liable for the obligations of the EEIG. In order to set up an EEIG, business entities from at least two EU countries must be represented. If the EEIG is domiciled in Denmark, it must be registered with the Danish Commerce and Companies Agency. According to the EC Regulation, at Article 40, the EEIG is transparent for tax purposes and taxes can only be levied on the individual participants. The participants are taxed according to national legislation in their respective countries of residence.

3.3. Foundations and Associations

Generally, foundations and associations are taxed in the same way as corporations. However, a number of important exceptions and special provisions apply – depending on the specific nature and characteristics of the foundation or association. Whereas some associations are transparent for tax purposes, other associations are only subject to taxation in respect of income from business activities. Deliveries made by an association to its members are not considered to be taxable business activities.

Contributions to associations and foundations are, as a general rule, tax-free.

Foundations and associations may generally set off distributions against their annual income when the distributions are made pursuant to the objective of the entity in question.

Further, if a contribution to the founding of a foreign foundation is made the contributor is generally liable to pay tax at 20%. The contributor is also liable to pay tax if a contribution is made after establishment of the foundation. These rules are only applicable to foundations set up in countries where foundations are taxed at significantly lower rates than in Denmark.

3.4 Production and Marketing Cooperatives

Production and marketing cooperatives are generally subject to taxation at a rate of 14.3% of their taxable income, which is determined as a specific percentage of their capital (usually in the range of 4% to 6%).

3.5 Investment Associations

Special rules apply to investment associations and investment Companies.

Investment companies are for tax purposes defined as:

(i) undertakings for collective investments in transferable securities comprised by the UCITS Directive (85/611/EEC);

(ii) companies whose businesses consist of investment in securities and where, at the request of the holders, shares in the company will be redeemed by the company or a third party at a price not materially below the net asset value; and

(iii) companies whose businesses consist of investments in securities and which have at least 8 shareholders. Affiliated entities and related parties are regarded as a single shareholder.

However, a company is not considered an investment company pursuant to (iii) above if:

(a) the company, through subsidiaries, primarily invests funds in assets other than securities;

(b) more than 15% of the company's assets are assets other than securities; or

(b) the company solely owns (i) shares, warrants or share rights in another company (the "employer company") that is not itself an investment company, and (ii) cash or cash deposited in an on-demand account not exceeding 15% of the company's total assets, provided that at the time of the purchase of the shares, all the shareholders in the first-mentioned company were employed by the employer company or a company affiliated with the employer company.

If the company has a controlling influence over or is affiliated with another such company, a proportionate part of the other company's assets is included in the calculation of the 15% threshold referred to in item (b) above.

Further, shares in another company that is not itself an investment company, where the shareholding equals at least 10% of that other company's share capital, are not considered to constitute securities. Investment companies are exempt from corporate tax. Instead, gains and losses on shares in investment companies are taxed pursuant to the mark-to-market principle.

Dividends on shares in investment companies are generally taxed at a rate of 25%.

Dividends distributed from Danish companies to investment companies are generally taxed according to a final withholding tax of 15%.

Other accumulating investment associations are generally taxed as corporations.

Distributing and account-based investment associations are usually exempt from tax as the investors are taxed in accordance with the principle of transparency.

3.6 Pension Funds

Pension funds are exempted from corporate tax. However, a special pension yield tax is payable at a flat rate of 15%.

As from the tax year 2010, taxation is applied at the level of the pension saver, whether the pension scheme is set up with a life insurance company, a pension fund or a financial institution.

Following the judgement made by the European Court of Justice on 30 January 2007 in case C-150/04 (Commission vs. Denmark), by which the Court held that Denmark must allow tax deductions for pension contributions to pension funds located in other EU member states, the Danish rules on taxation of pensions and pension funds have been amended in accordance with EU law.

Consequently, payments to pension schemes held by pension providers in other member states may also be deducted. This happens in accordance with an agreement model. This model implies that the foreign pension providers must make a binding agreement with the Danish authorities to report, withhold and pay tax in the same way as Danish pension providers.

Special rules apply with respect to pension schemes held by people moving to Denmark

4. Taxation of individuals

4.1 Tax Liability

As a general rule, an individual will have full tax liability if he is resident in Denmark or present in Denmark for a period of 6 months.

Individuals who are not subject to full tax liability in Denmark may be subject to limited tax liability in respect of income and gains deriving from certain sources in Denmark, including remuneration in respect of employment in Denmark, immovable property situated in Denmark, and dividends or royalties distributed from sources in Denmark.

4.2 Tax Rates

As a general rule, the income tax rate in Denmark has a maximum marginal rate of approximately 51.5% (the "tax ceiling"). The marginal tax rate including labour market contributions (which apply to salaries and wages etc.) is 56.5% (2010).

The income taxes for individuals include state tax, municipal tax, health tax and church tax.

The state tax is calculated as a progressive tax divided into a bottom-bracket tax of 3.67% (2010) and a top-bracket tax of 15%, which is calculated on income exceeding DKK 389,900 (2010). Further, municipal taxes and health tax have to be paid on a flatrate basis (on average 24.9% in 2010).

A church tax of 0.7% (average 2010) is payable by members of the Danish National Evangelical Lutheran Church (Folkekirken). Additionally, a labour market contribution of 8% and minor contributions, for example, to the Danish Labour Market

Supplementary Pension (ATP), are payable. These contributions are deducted before the calculation of income tax.

All fully liable taxpayers are entitled to a personal allowance. In 2009, the personal allowance is DKK 42,900 (2010) for taxpayers who have reached the age of 18 by the end of the income year. Employment is rewarded by an additional employment deduction of up to DKK 13,600 (2010).

4.3 Filing of Tax Returns and Payment of Taxes

The taxation year is the same as the calendar year. In March or April following the end of the calendar year, an income tax return is sent to each individual taxpayer. The tax return includes the figures that are known to the Tax Administration. The taxpayer must correct the figures before 1 May if the pre-populated figures are incorrect.

As a general rule, income tax on individuals is subject to withholding tax provisions. If the estimated tax is not subject to such withholding provisions ("B-tax"), it is collected over the course of 10 instalments during the relevant tax year.

4.4 Calculation of Taxable Income

4.4.1 Income and Capital Gains

The tax base includes worldwide income, including salaries, pensions, fringe benefits, profit-sharing plans and self-employment income.

Benefits are generally included in the taxable income and are based on their market value (for example, for a free company car) or based on standard rates (for example, for multimedia).

Certain healthcare benefits provided by the employer are exempt from taxation provided that the benefits are offered to all employees. Similar rules apply to education.

Employer contributions to pension schemes are tax-exempt. However, contributions are limited to DKK 46,000 (2010) if the pension is paid out as a lump sum.

Taxable income also includes capital gains on real property, shares, bonds, debt, receivables and financial instruments and related income such as interest, rental income and dividends.

Capital gains and interest are generally taxed as capital income at the progressive tax rates described above (but without any addition of labour market contributions). However, capital income which does not exceed a lower threshold of DKK 40,000 (DKK 80,000 for spouses) is exempt from tax.

Share income generally comprises capital gains and dividends on shares. Share income up to DKK 48,300 is taxed at a flat rate of 28%, whereas share income in excess of that amount is taxed at a flat rate of 42%.

4.4.2 Deductions

Individuals are entitled to deduct expenses specifically associated with their work – such as the cost of commuting between home and work, expenses for unemployment insurance, trade union fees and contributions towards early retirement schemes.

Further, as a general rule, net interest payable (negative capital income) such as interest on private loans or other net financial losses can be deducted in other income.

In general, however, individuals may only deduct expenses and losses, including interest expenses, in municipal and county taxes. Apart from interest expenses of up to DKK 50,000 per taxpayer (DKK 100,000 for spouses), the tax value of such deductions will be further reduced until 2019. Following this, the tax value of such deductions will be approximately 25.5%.

As from 2010, pension contributions are only deductible in personal income by up to DKK 100,000 (2010) per year.

Self-employed persons can deduct all expenses that have served to earn, secure and maintain their self-employment income (such as operating costs).

4.5 Employee Equity Plans

Danish tax law offers the following four different tax schemes for share-based employee incentives:

4.5.1 Section 4 of the Danish State Tax Act (Stats - skattel oven) and section 16 of the Danish Tax Assessment Act (Ligningsloven):

As a general rule, warrants and shares (and similar) are treated as cash remuneration and their value is taxed at grant as ordinary employment income. Any subsequent gain derived from the disposal of the shares received upon grant or exercise is taxed as a capital gain on shares (share income).

4.5.2 Section 28 of the Danish Tax Assessment Act:

Employee share options are generally taxed at exercise as ordinary employment income. Any subsequent capital gain derived from the disposal of the shares received in connection with the exercise is taxed as a capital gain on shares as share income.

4.5.3 Section 7A of the Danish Tax Assessment Act:

A tax exemption applies to employee share schemes which are offered generally to all employees or groups of employees. Where the tax exemption applies, no tax will fall due at grant or exercise.

At disposal of the shares, any gain is taxed as share income. The value of tax-exempt options is limited to 10% of each employee's annual salary per year and the shares must be tied up for at least 5 years.

As regards shares, the value must not exceed an amount of DKK 22,800 (2010) and the shares must be restricted from transferability over a period of 7 years.

4.5.4 Section 7H of the Danish Tax Assessment Act:

Under certain conditions, a special tax scheme also makes it possible to postpone taxation of options and shares until the shares acquired under the incentive scheme are disposed of. The share gain will then be taxed as share income – i.e. at a lower tax rate than employment income.

The employee and the company must agree in writing to opt for the regime and the value of the shares and options may not exceed 10% of the employee's annual salary per year. The employer company cannot deduct the cost of the options against its taxable income.

4.6 Expatriate Tax Regime

A special expatriate tax regime applies to foreigners employed by a Danish-resident employer. According to this scheme, under certain conditions the employee may opt for a flat tax rate of 25% over a period of 3 years or, alternatively, a flat tax rate of 33% over a period of 5 years. These rates will apply instead of the ordinary progressive rates and a marginal tax rate of 56.5% (including labour market contributions). However, when using the scheme, the employee will not be allowed to make any deductions on taxable income. To qualify for the scheme, individuals must reside in Denmark during the contract period, and their cash salary (if individuals have not been officially approved as researchers) must exceed DKK 69,348 (2010) per month (excluding contributions to the Danish Labour Market Supplementary Pension (ATP) and other pension contributions).

5. Other taxes

5.1 Special Gas and Oil Tax

Enterprises engaged in oil exploration, extraction and related activities are subject to special legislation on hydrocarbon tax.

5.2 Danish Maritime Tonnage Tax

Denmark has a special tax scheme for shipping companies offering an alternative basis for taxation. Under the scheme, a shipping company's Danish taxes are calculated on the basis of the capacity (tonnage) of the ships used by that company rather than on its profit or loss.

5.3 Value Added Tax

VAT is paid at all stages of the production and distribution of goods and services. Enterprises calculate their VAT liability as the difference between VAT paid on purchase and VAT levied on sales. The VAT rate is 25%.

5.4 Payroll Tax

VAT-exempt businesses are liable to pay a payroll tax (lønsumsafgift). The payroll tax rate depends on the specific VAT-exempt activity of the company. The rate generally varies between 2.5% and 9.13%. The taxation basis is calculated against the background of the company's total payroll.

5.5 Excise Duties and Green Taxes

A levy on the emission of carbon dioxide by companies and enterprises applies. It is possible to obtain a refund from the government in order to offset, in whole or in part, the negative effects of the carbon dioxide tax on energy-consuming companies and enterprises. Levies are imposed on energy, water consumption and waste disposal.

5.6 Registration Duties

Registration duties are imposed with respect to certain registrations such as registration of title to land, mortgages and ownership reservations. The rate of duty on registration of ownership to real property is 0.6% of the purchase price, plus DKK 1,400. The rate of duty on mortgages and ownership reservations is 1.5% of the secured claim plus DKK 1,400.

Duties are also imposed on certain registrations of rights concerning ships and aircraft.

A vehicle registration fee of up to 180% of the value is levied on private vehicles.

5.7 Stamp Duty

Stamp duty is imposed on certain insurance documents only.

5.8 Social Security, Healthcare and Other Welfare System Contributions

Apart from the above-mentioned health tax and labour market fund contributions (which are in fact state taxes paid by the taxpayers themselves), there are no other social security, healthcare or welfare system contributions (from a tax perspective). Further, the employer is not obliged to pay for any unemployment insurances.

However, it should be noted that from an employment law perspective, there are a number of obligatory social payments, including the ATP, FIB, AER and AES. The payment duty and the rates depend on, for example, the number of employees, whether they are paid by the hour and whether they are salaried employees. In the event of dismissal of an employee, the employer is generally not obliged to pay any severance allowance.

The government provides a favourable (and early) pension plan for people who have reached 60 years of age.

5.9 Property Taxes

Real property owners have to pay local taxes on the property value of their land. Depending on the local authorities, the tax rate is between 1.6% and 3.4%.

Homeowners are liable to pay tax on the value of housing property. The tax rate is 1%. However, for any part of the value that exceeds a limit of DKK 3,040,000 (2008), the tax rate is 3% on that amount.

Properties used for certain business purposes may be subject to a municipal service charge of 0.875% of the value of the buildings.

5.10 Inheritance and Gift Tax

5.10.1 Inheritance Tax

Inheritance tax is payable by the estate if, at the date of death, the deceased's country of residence was Denmark. Further, inheritance tax is payable on real property or estates relating to a permanent establishment situated in Denmark.

As a general rule, the tax rate is 15% of the value of the inheritance received by the next of kin. Spousal inheritance is free from any taxation. Inheritance by other persons is, as a general rule, subject to a tax rate of 36.25%.

The basis for calculating inheritance tax is the total value of the deceased's estate. Pensions and life insurances are included in the tax basis unless they accrue to a spouse. The value of the estate is generally the fair market value.

5.10.2 Gift Tax

As a general rule, gifts are taxed as personal income. However, a gift to a next-of-kin is tax-free provided that the value of the gift does not exceed 58,700 (2010). Amounts exceeding 58,700 (2010) in value are taxed at 15%.

Gifts to spouses are not subject to taxation.

6. Binding rulings

The Danish system comprises a set of rules that give taxpayers an opportunity to obtain a "binding ruling" from the Tax Administration.

Any person can obtain a binding ruling from the tax authorities with respect to a transaction that is intended to be executed by the applicant, or has already been executed. However, if the request concerns a third party, a ruling can only be obtained with respect to transactions which have not yet been made.

The request must be made in writing and contain all of the information available that is of importance to the reply. A fee of DKK 300 (2010) applies.

A binding ruling is binding on the tax authorities for a period of five years. However, a shorter time frame may be decided when the ruling is issued. A binding ruling is not binding:

- to the extent that the facts and assumptions on which the ruling is based change, including changes in legislation;

- if the answer is found to be contradictory to EU legislation; or

- if the answer is contradictory to a foreign tax authority's opinion regarding the interpretation of a tax treaty.

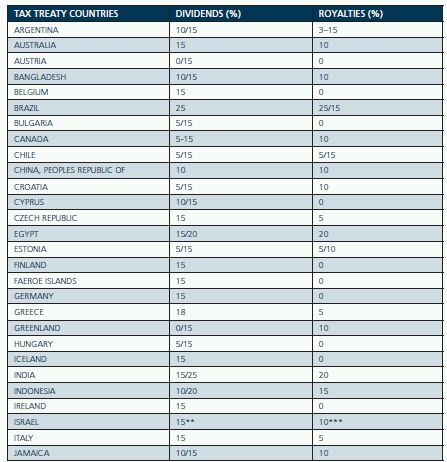

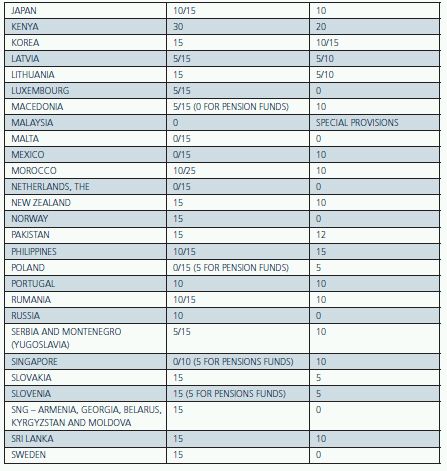

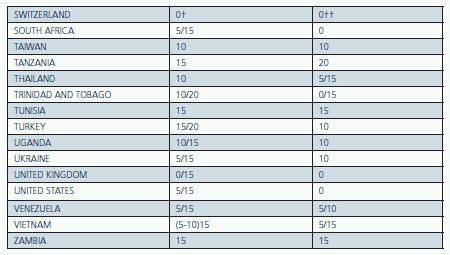

7. Tax Treaties

Denmark has concluded a large number of tax treaties. The tax treaties generally follow the credit method. However, some treaties follow the exemption method.

As mentioned above, dividends paid to a foreign parent company are not subject to any Danish withholding tax (or only to a reduced tax) if the parent company holds "subsidiary shares" or "group shares" (as defined above in item 2.2.21), and if the foreign parent company is resident in another EU country, or in a country with which Denmark has entered into a tax treaty according to which Denmark must grant relief or reduction from withholding tax. Most of the tax treaties concluded by Denmark state that the Danish withholding tax on dividends is reduced.

Further, interest is generally only subject to withholding tax if paid to affiliated entities in low tax countries.

Please note that the applicable regulations and the royalty and dividend definitions should always be examined in the particular tax treaty in question.

The list below reflects the situation as at 1 February 2010:

1 With respect to Greenland, a special rule of transition will be effective in the period 2009 -2012. In case a Greenlandic company has distributed dividends in 2007, Greenland is entitled to tax the dividends that will be distributed in the period 2009-2012, up to an amount that equal the dividends amount distributed in 2007 at a rate of 40.6% i 2009; 39.2% in 2010, 37.8% in 2011 and 36.4% in 2012.

** On 11 September 2009, Denmark and Israel agreed to enter into a new double tax treaty. According to the treaty, the rate will be reduced to 0/10%. It is uncertain from which date the double tax treaty will be effective.

*** On 11 September 2009 Denmark and Israel agreed to enter into a new double tax treaty. The treaty provides that royalties can generally only be taxed in the state where the recipient of the royalties is resident. Further, no tax ceiling has been agreed. It is uncertain from which date the double tax treaty will be effective.

+ On 21 August 2009, Denmark and Switzerland signed a protocol which amends the withholding tax rate for dividends. According to the protocol, the rate will be increased to 15%, but it is uncertain from which date the protocol will be effective.

++ On 21 August 2009, Denmark and Switzerland signed a protocol according to which royalties can generally only be taxed in the state where the recipient of the royalties is resident. Further, no tax ceiling has been agreed. It is uncertain from which date the protocol will be effective.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

To return to Part 1 of this article click 'Previous Page' below: