Climate-related shareholder activism, although not a new phenomenon in Canada,1s no longer the exclusive domain of environmentalists and increasingly a key plank in institutional shareholder and activist campaigns. A new era of climate-related activism is dawning, from "say-on-climate" and other environmental-related shareholder proposals, to proxy fights over the adequacy of companies' climate-related transition plans or emissions-reduction targets, to climate-related litigation against companies and their directors and officers for "greenwashing" and other matters. We anticipate that climate will become the predominate issue in upcoming proxy seasons, particularly for issuers in the mining, metals, energy, industrial and tech sectors, as well as for those issuers' lenders and key service providers.

Canadian companies and their directors and officers wishing to avoid public scrutiny or regulatory intervention need to keep their climate strategy at the forefront, including by embedding meaningful and coherent processes to assess and manage climate-related risks and opportunities throughout their business; developing and implementing plans to fulfill climate-related promises (such as navigating a net zero transition); and engaging proactively with stakeholders.

Canadian capital markets - which have a large number of extractive issuers and venture issuers - face critical challenges as the world transitions to a lower carbon economy while experiencing the physical and financial consequences of extreme weather events. Institutional investors, asset managers and other stakeholders have intensified their demands for enhanced transparency related to issuers' climate transition plans, their integration of climate-related factors into corporate strategy, their management of climate risk and self-assessments of business resilience, their specific emission targets and progress towards effective oversight of climate-related risks and opportunities.2

Since 2019, a paradigm shift in the global allocation of capital to sustainable investments has underscored the need for climate-related risks and opportunities to be factored into the price of investments to ensure efficient capital allocation. Global inflows into sustainable investments have reached over US$4 trillion3 and Canadian investment in sustainable funds more than doubled in 2021.4 As of the first quarter 2022, more than 4,900 entities from over 80 countries, representing approximately US$121 trillion in assets, have signed onto the UN Principles for Responsible Investment (PRI).5In addition, stakeholder pressures have contributed to divestment from many carbon-intensive sectors and increased investment in organizations focused on energy transition.

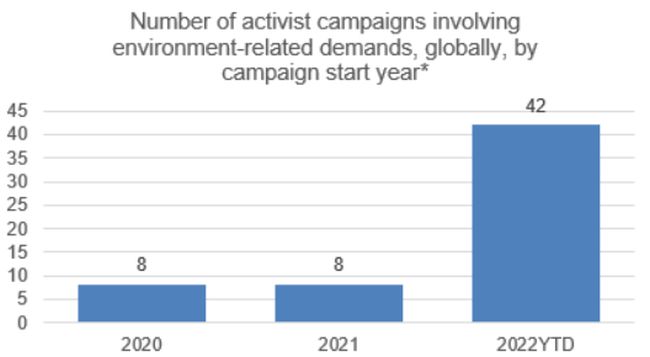

Climate-related activism has dramatically increased over the past five years. Globally, the number of activist campaigns involving public environment-related demands (including environmental demands relating to climate change or greenhouse gas ("GHG") emissions and campaigns with a social or sustainability objective) increased from a mere eight campaigns in each of 2020 and 2021, to 42 during 2022 year-to-date ("YTD"), representing a more than 400% increase relative to last year.6 Consistent with this trend, in the United States, the number of US-based issuers that faced public environment-related activist campaigns increased from just four and three in 2020 and 2021, respectively, to 33 in 2022 YTD.7 According to Insightia, during the first quarter of 2022 alone, half of the activist situations faced by Canadian issuers were focused on climate change, GHG emissions or other sustainability issues.8 And these figures do not account for the significant increase in the number of environment-related shareholder proposals globally and in each of Canada and the US, as discussed further below.

Canadian public companies and federally regulated financial institutions will soon be subject to mandatory climate-related disclosures9 and similar regulatory proposals have been proposed in the US by the Securities and Exchange Commission ("SEC"). While the scope of mandatory disclosures is still being debated, many companies are already voluntarily disclosing climate-related goals, strategies and risks. As with any disclosure, public companies and their leadership face concomitant liabilities, risks and obligations. Enhanced climate-related disclosures is expected to trigger greater stakeholder scrutiny and activism, as investors seek to redouble their efforts to drive further change, whether through public or private campaigns, shareholder proposals, litigation or other efforts aimed at encouraging regulators to commence enforcement actions including through whistleblower programs.

We anticipate that climate-related impact investing and activism will continue to escalate, with activists seeking changes to boards of directors or terminations of C-suite executives, agitating for transformative transactions such as spin-offs and "dirty" asset divestitures, and demanding more robust transition plans, greater progress on emissions reductions and improved climate-related disclosures. In turn, we anticipate an increase in the number and size of complex civil and regulatory actions against issuers. While this might be an inconvenient truth for some, companies should prepare as climate activism is here to stay during the global transition to a low carbon economy.

The growing storm

Canada has long been viewed by many as an activist-friendly jurisdiction. Whether or not that view is fair, the composition of Canada's capital markets and the existence of some uniquely Canadian legal tools available to stakeholders (including the right for 5%+ shareholders to requisition shareholders' meetings and the availability of a statutory oppression remedy), may contribute to more investors targeting Canadian companies with climate-related activism.

Shareholder proposals: Over the prior five years, the volume and levels of support for climate and social-related shareholder proposals have increased rapidly. The primary objectives of these proposals include enhanced company disclosure and accountability. The recent changes by the SEC broadening the scope of permissible shareholder proposals, has resulted in a clear increase in environmental and social shareholder proposals being put to a vote before SEC-registered companies.10 Climate-related proposals in the 2022 proxy season so far have received mixed results, with some investors, including BlackRock, the world's largest fund manager, becoming more critical of and less willing to support proposals that "are more prescriptive or constraining on companies" or that seek to "micromanage companies".11 Regardless of this season's outcomes, climate-related shareholder proposals present significant strategic, business, legal and reputational risks for companies and their directors and officers and, even if unsuccessful, can serve as a strong platform for future change.

A growing number of large companies have held or committed to hold say-on-climate advisory votes - an annual, non-binding advisory shareholder vote on the companies' disclosed climate action plans. In 2021, shareholder advocacy groups filed say-on-climate resolutions for more than 75 companies in North America and over 147 climate-related resolutions were filed in the United States, with 47 of them going to a shareholder vote.12 Both during and prior to the 2022 proxy season, major oil and gas companies globally have faced an unprecedented number of climate-related shareholder proposals seeking them to, among other things, adopt reduced emission targets and to report on climate-related financial risks, typically in accordance with the Recommendations of the Task Force on Climate-related Financial Disclosures ("TCFD").13

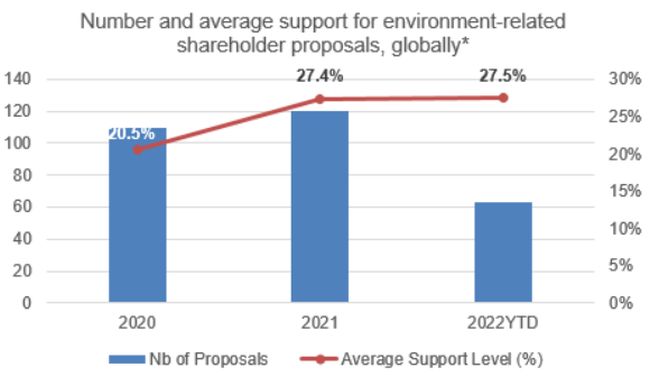

Globally, the number of environment-related shareholder proposals went from 110 for the full year 2020, to 120 for the full year 2021, to 63 already YTD 2022. In the US, the number of environment-related shareholder proposals rose from 28 in 2020, to 39 in 2021 and 36 YTD 2022. And in Canada, the number of environment-related proposals rose from seven and four in each of 2020 and 2021, respectively, to nine YTD 2022.14 In Canada, say-on-climate shareholder proposals are gaining increased prominence, albeit with mixed success.15 In 2021, each of Canada's largest rail companies passed shareholder climate proposals and committed to hold annual climate votes. In 2022, each of Canada's largest banks was subject to say-on-climate shareholder proposals, with some being withdrawn after shareholder engagement agreements were reached and the remaining proposals being defeated by large majorities.16

Even if such proposals are not passed by a majority of shareholders, many believe that securing sufficient minority shareholder support can drive an issuer's management and board to engage on the issue and implement change, failing which a similar (or perhaps even more stringent) proposal could gain support in subsequent years. Importantly, many investors believe that, although the required change in disclosure and accountability may not come this year or even next, particularly given the business, economic, health and geo-political challenges companies currently face, they will come eventually.

Canadian companies are to varying degrees continuing to enhance their climate-related disclosures in response to investor pressures and recent regulatory initiatives.17 At the same time, well-crafted (and reasonable) shareholder proposals to drive greater transparency and accountability on a company's climate plans are gaining traction. Climate-related disclosures, including net zero commitments, are also being carefully scrutinized by investors and, where viewed as being deficient, may help engaged investors pressure companies to commit to enhanced short-term or medium-term targets or take other actions to reduce climate-related business, financial and operational risks. In the 2021 and 2022 proxy season, climate-related shareholder proposals covered a broad range of demands, including seeking:

- an enhanced "science based" net zero transition plan,

- reduced emissions (including scope 3 emissions) and stronger interim emission targets that are detailed, science-based and subject to third party assurance;

- disclosure of corporate lobbying practices and alignment of corporate lobbying practices with decarbonisation;

- adoption of lending and underwriting policies consistent with a transition to net zero;

- ceasing to provide financing to traditional energy companies or decommissioning traditional energy assets; and

- altering constating documents to mandate climate risk reporting or voting.

The level of support for such proposals has generally been on an upward trajectory. For example, globally, the level of shareholder support for environment-related proposals went from an average of 20.5% in 2020 to 27.4% in 2021 and 27.5% YTD 2022. And while YTD 2022 levels of support for environment-related shareholder proposals in each of the US and Canada is relatively lower than in 2021, average support is still up from several years ago. For example, in 2021, 40% of US institutional shareholder votes were cast in favour of environment and social shareholder proposals, the highest level in five years.18 In 2021, a shareholder climate-related proposal against a major oil and gas company requiring that the company disclose its emissions from the use of its energy products in the medium and long term was passed with 61% shareholder approval, which included several large institutional shareholders.19 In addition, last year, shareholder proposals requiring several other major oil and gas companies to align their lobbying activities with decarbonisation goals were also approved by a majority of shareholders.20

While the average level of support for proposals has stabilized or, in several jurisdictions, declined in 2022 YTD, this is partly due to the increased volume in proposals and the prescriptive nature of many of those proposals, which has caused some investors and proxy advisory firms to push-back on perceived overreaching or overly prescriptive proposals (e.g. BlackRock21). For example, on May 25, 2022, nearly two-thirds of investors in ExxonMobil and Chevron rejected proposals for the companies to align their climate strategies with the requirements of the Paris Agreement.22 However, shareholder proposals for enhanced reliable emission disclosures were approved at ExxonMobil and Chevron by 52% and 98%, respectively. Similarly, a proposal put forward at Royal Dutch Shell plc by a climate activist that had received 30% support in 2021 (after receiving only 2.7% support in 2016)23, received only 20% support at Shell's May 2022 annual meeting.24 The ongoing war in Ukraine and its implications on global energy may also be contributing to increased hesitation around climate and emissions proposals in 2022.

While 2022 trends to-date stand in stark contrast to those in 2021, in our view, well-crafted proposals are still likely to receive high levels of support going forward, consistent with past trends. Several large institutional shareholders have also signalled their willingness to hold directors accountable by voting against their re-election where a company fails to provide appropriate climate-related disclosures or sufficient targets for reducing emissions in the short, medium and long term.25 Despite BlackRock's recently stated intention to "support proportionately fewer this proxy season than in 2021", BlackRock remains supportive of proposals that require companies to deliver information that helps investors understand the material risks and opportunities they face, such as their climate action plans (supported by quantitative information such as scope 1 and scope 2 GHG emissions and emissions-reduction targets).26 As institutional shareholders and proxy advisory firms continue to adjust their proxy voting guidelines and report their voting activity, we anticipate continued engagement by shareholders to generate support for climate-related proposals.

Proxy campaigns: Activists, impact investors and other shareholders may also launch withhold campaigns or proxy contests targeting directors and/or officers of issuers that have not taken meaningful steps to address climate-related risks and opportunities, such as failing to develop and implement robust climate plans, failing to provide specific and quantifiable climate-related disclosure or those engaging in "greenwashing".

Proxy fights to replace incumbent directors based on lack of oversight of climate-related risks are not new, 27 but gained global prominence in 2021 after Engine No. 1, an investor then-holding a 0.02% stake in ExxonMobil, mounted a successful proxy campaign to win three seats on ExxonMobil's board. The proxy battle centered on ExxonMobil's poor performance and resistance to developing a low-carbon transition plan. Importantly, the campaign secured the support of key institutional investors. Engine No. 1's victory may have helped open the gates for a new wave of ESG-related activist campaigns by stakeholders who have seen mixed or poor results from other engagement efforts.

It's worth noting that, in the current capital market environment, these developments are also generating additional funding for activist and impact investors from a range of entities, including institutional investors focused on ESG investing. With this growing capital pool, we expect investors and other stakeholders will continue to target select Canadian issuers, particularly those that are underperforming their peers and are perceived to be lacking or having deficient climate-related transition plans or other ESG-related financial metrics, and will seek the support from institutional shareholders both publicly and privately.

Disclosure-related litigation: Given investor focus on issuer disclosure and regulatory initiatives relating to climate-related disclosures, we have also witnessed a steady increase in environmental-related class actions and other proceedings globally against companies and their directors and officers by a wide range of stakeholders, including investors.28 These claims have alleged, among other things:

- Failure to adequately assess and develop strategies to address the impacts of climate change on the company's long-term business, including by developing and implementing a climate transition plan, and misleading shareholders on such impacts and strategy;29

- "Greenwashing", including inaccurate and misleading disclosure relating to climate strategy and targets or a lack of a reasonable basis for net zero or other climate-related plans or commitments;30

- Failure to disclose material climate-related information in the context of a "green" sovereign bond issuance;31 and

- Inaccurate and misleading financial and operational disclosure relating to the impact of climate change on a company's assets and enterprise value, including inappropriate accounting treatment of climate change costs in relation to a resource extraction project.32

Until recently, shareholders have been largely unsuccessful in maintaining these claims. However, we anticipate they will continue to adapt their approaches and the pending mandatory climate disclosure regimes will help bolster such claims and allow them to survive preliminary challenges.

Fiduciary duty litigation: Another avenue for potential recourse is "duty of care" derivative claims brought by interested parties on behalf of companies against their directors and officers for failure to manage the climate impacts of their companies' operations, which in turn negatively impacts the companies' enterprise value.33 For example, in England, an activist shareholder has sought to initiate legal action against Shell's board of directors over the company's alleged mismanagement of its climate-related obligations. The activist has alleged that Shell's directors breached their duties to act in good faith, exercise independent judgment and reasonable care, skill and diligence (notably, directors and officers of Canadian companies have similar duties to their companies). Given the higher burden for commencing derivative actions in Canada, the likelihood of such claims being brought or being successful appears remote compared to other tools available to investors, but such litigation cannot be ruled out.

Similar theories have been advanced elsewhere, such as last year's landmark decision by the Hague District Court, which ordered Shell to reduce its worldwide CO2 emissions by 45% by 2030 (compared to 2019 levels), based on European human rights laws. In this class action claim brought by environmental groups, the Court found that Shell had failed to take sufficient measures to reduce emissions generated by the company in breach of a duty of care to prevent dangerous climate change through corporate policies.34 Shell has appealed the decision, although it is also facing pressure from one of its asset management investors to drop the appeal.35

Regulatory enforcement actions: We also expect investors and other stakeholders will continue to bring formal complaints directly to regulators and other government agencies relating to the inadequacy of or misleading disclosures relating to companies' climate-related plans, yet another potential means of driving corporate change.

Canada and the United States have formal whistleblower programs (some of which provide monetary rewards) through which interested stakeholders can submit complaints alleging inaccurate or misleading climate-related disclosures, breaches of laws, breaches of codes of conduct or other corporate policies, and various other matters. Recent examples of such complaints to regulators include:

- Complaint filed by an environmental group to the Canadian Competition Bureau against a coffee company alleging misleading statements regarding the recyclability of its single-use coffee pods. The complaint resulted in an investigation by the Competition Bureau and a settlement with the company in early 2022 under which it paid a $3 million fine, donated $800,000 to a Canadian environmental organization, changed its product packaging and enhanced its compliance program. 36

- Complaint filed by Indigenous peoples supported by two environmental groups to the Canadian Competition Bureau requesting an investigation of a Canadian bank for allegedly making misleading statements regarding its climate commitments and calling for the bank to make significant reductions in its financing of fossil fuel projects.37

- Complaint filed by certain environmental groups with the U.S. Federal Trade Commission against a major oil company alleging misrepresentations by the company to consumers relating to its investment in renewable energy and reducing carbon emissions. This complaint came on the heels of a number of civil actions commenced in the US alleging "greenwashing" by several large oil and gas companies.38

- Complaint by former head of sustainability of the asset management arm of a global bank to the SEC alleging that the asset management entity overstated its use of sustainable investing criteria for the US $1 trillion of assets under management.39

Given the global focus on climate-related disclosures, we expect heightened regulatory scrutiny of climate-related disclosures and, accordingly, a greater risk that complaints may trigger regulatory investigations and, ultimately, enforcement action.

Even prior to the implementation of enhanced mandatory climate-related disclosure requirements, Canadian and US securities regulators have indicated that that they will hold companies and their directors and officers responsible for their climate-related statements, whether in regulatory filings, voluntary sustainability reports or marketing materials using a range of tools, from disclosure deficiency letters to enforcement proceedings. The SEC recently created a separate climate-related enforcement unit and, in April 2022, commenced the first enforcement proceedings against a US company for false and misleading disclosure in its annual sustainability reports.40

So, how can companies prepare?

- Risk oversight and risk management: A board's responsibility for risk oversight, derived from directors' statutory and common law duties, remains a critical priority for all organizations. This requires that boards obtain reasonable assurance that management has identified an organization's principal risks and put in place appropriate risk management protocols. Climate is clearly one such risk. As such, issuers should develop and implement appropriate analyses and metrics for assessing, monitoring and managing short, medium and long-term climate-related risks and their impact on corporate value and strategy. Having a robust oversight structure in place is crucial for effective board oversight of a company's climate-related risks.

- Planning and crisis management: The board and senior management should regularly review, stress-test and update, as necessary, a company's crisis management plan, to anticipate potential ESG-related issues or events and to ensure the company is adequately prepared to deal with them, including extreme weather events or any other unexpected event that would likely impact the company's operations. This often includes running scenario analysis before the board; identifying appropriate members of any crisis response team and company spokespersons; developing internal and external communications plans; and establishing appropriate insider trading and blackout restrictions.

- Stakeholder engagement: Companies should ensure that shareholder engagement is treated as a key (and regular) feature of their overall governance program and, as appropriate, proactively engage with investors and other key stakeholders. Be mindful that investors, as well as proxy advisory firms and regulators, are watching each company's governance, oversight, execution and response to climate-related risks and opportunities and its performance compared to stated climate-related goals and to the performance of peer companies. Understanding how a company's stakeholders view the organization's efforts in this regard, can provide important early warning of where the company may be falling short.

- Disclosure controls: Companies should treat climate risk disclosures with the same level of care and scrutiny that are applied to other material financial, business and operational disclosures, keeping in mind that ordinary principles of materiality may no longer be sufficient for adequately assessing and preparing disclosures about climate risk matters. As societal expectations evolve, specific disclosures about the qualitative and quantitative climate-related risks and opportunities associated with the business, which will vary from issuer to issuer and across industries, including reporting climate-related information in financial filings consistent with the TCFD (or a similar standardized framework), are becoming the norm, rather than the exception.

- Stay ahead of the issues: While investors like BlackRock may, at least this year, be willing to give some companies more time and leeway to continue to advance their overall climate strategy (provided meaningful progress is being made in their energy transition), companies should not construe this as a license to be stagnant. For example, scope 3 GHG emissions are broadly recognized as posing significant business and investment risk, which companies will at some point be required to tackle (and disclose). Ensuring boards and senior management have the right expertise to understand and respond to these and other ESG-related issues, and are consistently evolving their practices and disclosures in this regard, is now a business imperative.

Footnotes

1. Almost 40 years ago, Greenpeace Foundation of Canada unsuccessfully attempted to submit a shareholder proposal to Inco Ltd. seeking the implementation of "pollution control measures to reduce acid rain by restricting sulphur dioxide emissions".

2. The Institutional Investors Group on Climate Change (IIGCC) is a leading global investor membership body and the largest one focusing specifically on climate change. Its 370+ members - mainly asset owners and managers, specialist investors and select financial service providers - represent over ?50 trillion in assets, and include several Canadian members. Many of Canada's largest pension funds have committed to reducing the carbon intensity of their respective portfolios. At the same time, the recent statement from BlackRock's Investment Stewardship team that it will vote against climate resolutions more often in 2022 is a warning that there are limits to how far institutional investors will go to support environmental governance initiatives. The world's largest asset manager explained its view that shareholder resolutions on climate change have become overly extreme or prescriptive, a reflection that enthusiasm for such measures from activists may currently be outpacing traditional players' appetites for them. BlackRock confirmed its overriding commitment to the pursuit of long-term shareholder value, and stated its aversion to micromanaging the companies in which it invests. See https://www.blackrock.com/corporate/literature/publication/commentary-bis-approach-shareholder-proposals.pdf.

3. Morningstar Research Inc., Sustainable Assets are Teetering on the $4 Trillion Mark, November 1, 2021, https://www.morningstar.co.uk/uk/news/216474/sustainable-assets-are-teetering-on-the-%244-trillion-mark.aspx.

4. Morningstar Research Inc., Sustainable Investing Landscape for Canadian Fund Investors, Q4 2021, January 24, 2022.

5. Principles for Responsible Investment, Quarterly Signatory Update, https://www.unpri.org/signatories/signatory-resources/quarterly-signatory-update.

6. Insightia data. Within Insightia's data set, "environment-related" refers to any public activist demands comprising of animal welfare, climate change & GHG emissions, deforestation, sustainability and waste pollution. Within the category of "climate change & GHG emissions", this includes any activist demands that the company either amend a policy, provide information or address a concern relating to climate change or greenhouse gas emissions.

7. Ibid.

8. Insightia, Shareholder Activism in Q1 2022 (April 2022).

9. On October 18, 2021, the Canadian Securities Administrators (the "CSA") released proposed National Instrument 51-107 Disclosure of Climate-related Matters and its Companion Policy 51-107CP Disclosure of Climate-related Matters for a comment period which ended on February 16, 2022. See also: 2022 Federal Budget, which includes significant measures to build a net-zero economy and to fight climate change, https://budget.gc.ca/2022/report-rapport/toc-tdm-en.html; Office of the Superintendent of Financial Institutions, Building Federally Regulated Financial Institution Awareness and Capability to Manage Climate-Related Financial Risk, January 14, 2022, https://www.osfi-bsif.gc.ca/Eng/fi-if/in-ai/Pages/clrsk-mgm_let.aspx.

10. US SEC, Shareholder Proposals: Staff Legal Bulletin No. 14L (CF) (November 3, 2021), https://www.sec.gov/corpfin/staff-legal-bulletin-14l-shareholder-proposals.

11. BlackRock, Inc., BlackRock Investment Stewardship: 2022 climate-related shareholder proposals more prescriptive than 2021, May 2022, https://www.blackrock.com/corporate/literature/publication/commentary-bis-approach-shareholder-proposals.pdf.

12. Climate Action 100+, 2021 Year in Review, A Progress Update, at p.8, https://www.climateaction100.org/wp-content/uploads/2022/03/Climate-Action-100-2021-Progress-Update-Final.pdf.

13. S&P Global Market Intelligence, Activist investors turning up heat on oil majors in proxy voting season, April 25, 2022, Activist investors turning up heat on oil majors in proxy voting season | S&P Global Market Intelligence (spglobal.com).

14. Supra note vi.

15. Recently, the Investment Stewardship branch of Vanguard, a leading fund manager with over US$7 trillion in assets under management, announced that it does not proactively encourage companies to hold "say on climate" votes given the lack of established standards or widely accepted market norms that govern these votes. Similar to BlackRock, Vanguard stated that "[a] core principle of Vanguard's stewardship program is that we do not seek to direct a company's strategy-including on climate-change plans. Instead, we look to its board to articulate how the strategy is expected to generate shareholder value." See Vanguard, Vanguard Investment Stewardship Policy Insights: Our perspective on Say on Climate proposals (May 2022), https://corporate.vanguard.com/content/dam/corp/advocate/investment-stewardship/pdf/perspectives-and-commentary/policy_insights_sayonclimate_final.pdf.

16. T. Kiladze, Canadian bank investors resoundingly reject push for 'say-on-climate' votes (April 14, 2022).

17. See, for example, the CSA's proposed National Instrument 51-107 Disclosure of Climate-related Matters, https://www.osc.ca/sites/default/files/2021-10/csa_20211018_51-107_disclosure-update.pdf (comment period closed); the SEC's proposed rule, The Enhancement and Standardization of Climate-Related Disclosures for Investors, RIN 3235-AM87, https://www.sec.gov/rules/proposed/2022/33-11042.pdf (open for public comment); the International Sustainability Standards Board's IFRS Sustainability Disclosure Standard, March 2022, https://www.ifrs.org/content/dam/ifrs/project/climate-related-disclosures/issb-exposure-draft-2022-2-climate-related-disclosures.pdf (open for public comment).

18. Broadridge Financial Solutions and PwC Governance Insights Center Initiative, Proxy Pulse, 2022 Proxy Season Preview, broadridge-proxypulse_2022-season-preview-and-2021-review.pdf.

19. Reuters, Chevron Shareholders Approve Proposals to Cut Customer Emissions (May 26, 2021), https://financialpost.com/pmn/business-pmn/chevron-shareholders-approve-proposal-to-cut-customer-emissions-2. See also: Chevron Corporation, 2022 proxy statement, April 7, 2022, https://www.sec.gov/Archives/edgar/data/0000093410/000119312522098301/d292137ddef14a.htm.

20. SHARE, Phillips 66 Shareholders Vote in Favour of SHARE Proposal on Climate Lobbying (May 17, 2021), https://share.ca/blog/phillips-66-climate-lobbying/.

21. Supra note xi.

22. The Washington Post, Investors Reject Climate Proposals targeting ExxonMobil, Chevron (May 26, 2022), https://www.washingtonpost.com/politics/2022/05/26/investors-reject-climate-proposals-targeting-exxonmobil-chevron/.

23. Supra note xiii.

24. S. Nasralla and R. Bousso, Shareholders back Shell's climate strategy after raucous meeting (May 24, 2022), https://www.reuters.com/business/environment/climate-protestors-disrupt-shell-shareholder-meeting-2022-05-24/.

25. BlackRock, Inc., Our 2021 Stewardship Expectations, Global Principles and Market-level Voting Guidelines, https://www.blackrock.com/corporate/literature/publication/our-2021-stewardship-expectations.pdf.

26. Supra note xi.

27. In 2003, Ethical Funds Inc. almost obtained majority support (49.20%) at a contested meeting for a shareholder proposal requesting that IPSCO Inc. "establish a policy of disclosing facility-specific toxic emissions data and greenhouse gas emissions data."

28. See for example Goldman Sachs Grp., Inc. v. Arkansas Tchr. Ret. Sys., 141 S. Ct. 1951, 210 L. Ed. 2d 347 (2021); Ramirez v. Exxon Mobile Corporation, 334 F. Supp. 3d 832 (N.D. Tex. 2018); McVeigh v. Retail Employees Superannuation Pty Ltd ACN 001 987 739 (November 2, 2020), Australia NSD1333/2018 FCA)).

29. See, for example, In Re Exxon Mobil Corporation, Civil Action No. 2:19-CV-16380-ES-SCM (D.N.J. Sep. 15, 2020). City of Birmingham Retirement and Relief System v. Tillerson, 3:19-cv-20949 (D.N.J. Dec 2, 2019); Ramirez v. Exxon Mobil Corp., 334 F. Supp. 3d 832 (N.D. Tex. 2018).

30. See, for example, Beyond Pesticides v. Exxon Mobil Corporation, D.C. Super. Ct. Case No. 2020-CA-002532 (non-profit sued ExxonMobil, claiming it greatly overstated its engagement in cleaner forms of energy); Jochims v. Oatly Group AB, 1:21-cv-06360 (S.D.N.Y. Oct. 26, 2021) (class action alleging that an oat milk company made false and misleading statements about the company's sustainability).

31. See, for example, O'Donnell v. Commonwealth of Australia [2021] FCA 1223.

32. See, for example, Ramirez v. Exxon Mobil Corp., 334 F. Supp. 3d 832 (N.D. Tex. 2018); NY AG v. Exxon Mobil Corporation, 452044/2018 (Sup. Ct. N.Y. Dec. 10, 2019); City of Birmingham v. Tillerson, No. 3:19-cv-20949, Verified Stockholder Derivative Complaint ¶¶ 3-5 (D.N.J. Dec. 2, 2019).

33. ClientEarth, We're Taking Legal Action Against Shell's Board for Mismanaging Climate Risk (March 15, 2022), https://www.clientearth.org/latest/latest-updates/news/we-re-taking-legal-action-against-shell-s-board-for-mismanaging-climate-risk/.

34. Hague District Court, Milieudefensie et al. v Royal Dutch Shell plc, NL:RBDHA:2021:5339 (May 26, 2021). See also https://www.reuters.com/article/us-usa-ftc-greenwashing-idUSKBN2B82D7.

35. Reuters, Shell Filed Appeal Against Landmark Dutch Climate Ruling (March 29, 2022), https://www.reuters.com/business/sustainable-business/shell-filed-appeal-against-landmark-dutch-climate-ruling-2022-03-29/. See also open letter by Odey Asset Management LLP to Shell plc dated May 19, 2022, https://www.rns-pdf.londonstockexchange.com/rns/1591M_1-2022-5-19.pdf.

36. Government of Canada, Keurig Canada to Pay $3 Million Penalty to Settle Competition Bureau's Concerns over Coffee Pod Recycling Claims (January 6, 2022), https://www.canada.ca/en/competition-bureau/news/2022/01/keurig-canada-to-pay-3-million-penalty-to-settle-competition-bureaus-concerns-over-coffee-pod-recycling-claims.html.

37. Wealth Professional, Big Bank 'Strongly Disagrees' with Greenwashing Claims (April 22, 2022), https://www.wealthprofessional.ca/investments/socially-responsible-investing/big-bank-strongly-disagrees-with-greenwashing-claims/366021.

38. Reuters, Green Groups File FTC Complaint Against Chevron over Climate Claims (March 16, 2021), https://www.reuters.com/article/us-usa-ftc-greenwashing-idUSKBN2B82D7.

39. The Wall Street Journal, U.S. Authorities Probing Deutsche Bank's DWS Over Sustainability Claims, August 25, 2021, https://www.wsj.com/articles/u-s-authorities-probing-deutsche-banks-dws-over-sustainability-claims-11629923018.

40. US SEC, SEC Charges Brazilian Mining Company with Misleading Investors about Safety Prior to Deadly Dam Collapse (April 28, 2022), https://www.sec.gov/news/press-release/2022-72.

To view the original article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.