The liability proxy is a key component of an effective liability hedging strategy. In this article we explore why it is important and what pension schemes can do to get their hedging right.

Much of the commentary around the 2022 liability driven investment (LDI) crisis has focused on collateral considerations and the impact on pension schemes which found themselves short of collateral assets. But the large moves in interest rates and inflation expectation also highlighted a second issue for some individual pension schemes whose hedging portfolios didn't move as closely in line with liabilities as expected. In this article, we explore how the effectiveness of a hedge depends on the construction of the "liability proxy".

Before you can build a hedging portfolio, you need to understand the scheme benefit design and how the benefits are valued

Hedging inflation and interest rate risk requires a good understanding of the underlying scheme benefits and their characteristics together with clarity on the manner in which the liabilities will change under different interest rate and inflation environments. How a hedge will perform over time as interest rates and inflation expectations change depends on how effectively the hedge captures the shape and duration of future benefit payments and the sensitivity of the liabilities to inflation. For hedging, the shape and characteristics of the liabilities are combined into a "liability proxy". The liability proxy aims to capture the interest and inflation sensitivity of the liabilities.

The first step in any liability proxy construction is making sure there is a common and clear understanding of the aim of the hedge. This could range from trying to hedge a best estimate measure of the liabilities to trying to keep the technical provisions or buy-out funding level stable to trying to protect the pound amount of the surplus and beyond. The liability proxy could differ significantly depending on the chosen aim.

Having agreed the objectives, the liability proxy can then be constructed. This is not always a simple task. Pension schemes typically have a range of different pension increases that apply to different members and tranches of benefit. The increases also commonly differ before and after retirement. The challenge is that these different linkages need to be captured and turned into something that the hedging portfolio can invest to match these increases. Furthermore, the sensitivity of the liabilities to changes in interest rates and inflation will depend on the assumptions being used within the liability measure itself.

Careful thought also needs to be given to how member options such as early retirement, transfer values and commutation lump sums are treated since these can affect the duration and the sensitivity of the liabilities (e.g. are the scheme's commutation factors treated as being fixed or is there a link to markets), as can other demographic assumptions such as mortality.

Typically, the demographic and inflation assumptions that are used for funding purposes were not chosen with hedging in mind and may not necessarily be appropriate for the construction of the liability proxy depending on the objective of the hedge.

Getting the liability proxy wrong can have material financial consequences

The consequences of getting the liability proxy wrong can be very material and have a significant impact on pension scheme funding.

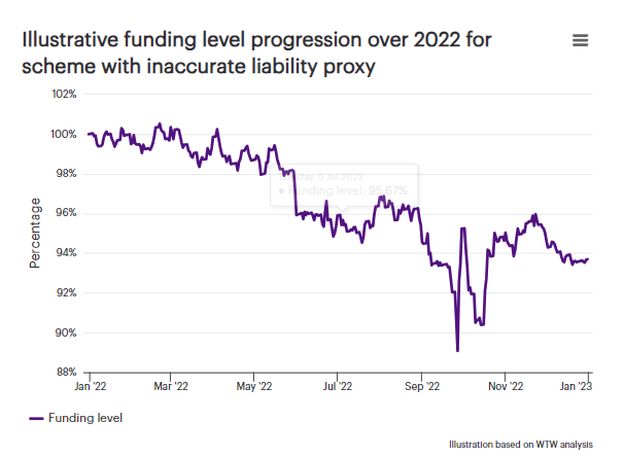

As an example, the chart below shows how much the funding level for a scheme thought to be "100% hedged" could have changed over 2022 where the liability proxy didn't properly differentiate between the increases that apply before and after retirement.

At one point in the year, getting the liability proxy wrong in this way could have pushed the funding level out by more than 10%.

As another example, for a scheme where the duration of the liability proxy was overstated by just two years (e.g. due to the use of inappropriate assumptions regarding commutation and overly prudent mortality), rising interest rates in 2022 would have caused the funding level to drop by 6%.

Implications for liability proxy projects?

Given the importance of getting a scheme's hedging right, we recommend that liability proxy construction projects are carefully planned, with the different roles and responsibilities clearly identified. Input from the Scheme Actuary will be important here given their more detailed working knowledge of the liabilities and benefits. For example, we suggest involving the Scheme Actuary in the choice of assumptions used to project future benefit payments for hedging purposes, as opposed to automatically using the funding valuation assumptions without careful consideration of what it is you are trying to hedge.

We also suggest checking that the liability proxy will be constructed based on cashflows that capture all of the inflation linkages, both before and after retirement.

Liability proxies should also be kept under regular review and updated to capture material changes in inflation expectations or scheme experience (e.g. where there are higher than expected outflows due to transfers out or high retirement rates). With input from the Scheme Actuary, an interim update to a liability proxy to capture such changes can often be done quickly and pragmatically.

Finally, we think it is worth considering the division of responsibilities. In some cases it will be more efficient and more robust for the Scheme Actuary to calculate the liability proxy, with the investment adviser feeding in relevant assumptions (e.g. inflation sensitivity). In other cases, a fully integrated approach, combining the calculation work and advice on the choice of assumptions (both demographic and financial) for liability hedging purposes may be more appropriate.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.