Overview

Over the last few years, the Family Limited Partnership (FLP) has become an increasingly popular vehicle for asset protection and succession planning within wealthy families. They have been particularly useful in complementing or as an alternative to the trust or foundation, which may not be suitable for tax reasons and/or due to an unsympathetic treatment of such vehicles in certain jurisdictions.

The FLP first became popular in the UK after the imposition of significant tax charges on UK domiciled settlors contributing assets to a trust. The potential 20% up-front tax charge prompted the requirement for a non-trust structure which still provided for controlled and tax-efficient succession planning. Since then, the flexible nature of the FLP has also become attractive to international families who do not necessarily have a base in the UK.

Basic Principles

A Limited Partnership is a vehicle offered by a number of jurisdictions but it is particularly well-established in the UK and Ireland. The key features of all limited partnerships are:

- A General Partner (GP) must be appointed to manage the assets on behalf of the Limited Partners (LPs). Typically, the GP contributes a minimal amount of capital but is instead paid a fee for the management of the assets. The liability of the GP is unlimited (although in practice this can be remedied by the GP taking the form of a limited liability company).

- One or more LPs contribute capital to the LP to be invested. As they do not take part in the management of the assets, their liability is limited to the capital contributed.

- A limited partnership is generally considered tax transparent. That is, members are taxable on their share of profits but the partnership itself has no taxable presence.

- There is a high degree of flexibility in the way the business and relations between the partners are governed. This is typically determined by the Partnership Agreement where there is absolute flexibility on matters such as voting, profit sharing and distributions.

Typical Structure for International Families

The FLP is most suited to families owning large multi-jurisdictional businesses where individual family members will often be resident in multiple jurisdictions for reasons of work, study, family and perhaps wider economic and political reasons. Exposure to multiple legal systems, tax rates and risk factors requires a flexible but robust asset protection/succession planning vehicle for the family assets.

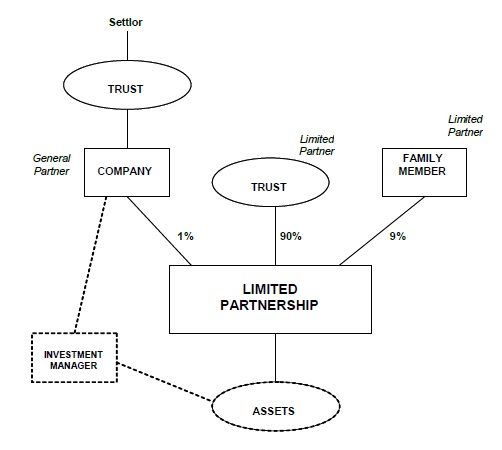

A typical FLP structure might look as follows:

It will be seen from the above example that the FLP often augments existing trust structures established by family members, but this is not necessarily the case. Whilst trusts may provide an added layer of asset protection, confidentiality and may reduce tax exposure, they may not be appropriate in jurisdictions where they are poorly understood and / or considered an aggressive tax avoidance tool by local tax authorities. In such cases, it may be more effective to substitute trusts for simple companies acting as partners in the FLP.

In the example structure illustrated above, the principal family shareholder with a controlling stake in the business would have already established a trust (from which he or she can benefit) for the purposes of asset protection. He or she now wishes to use a more flexible and transparent vehicle, in the form of the FLP, to give away tranches of the business to future generations whilst retaining control. To achieve this:

- The trust becomes an initial 99% capital and profit-sharing partner in a new FLP, by contributing shares in the family business in exchange for an FLP partnership interest.

- A second trust is settled by the controlling shareholder which, through an underlying company, becomes the general partner with a nominal 1% capital share. Through operation of the trust, the shareholder retains control over the management of the assets of the FLP. Use of a trust reduces risk of direct attribution of income and capital to the shareholder or of the possibility that the structure may be viewed as a sham.

- Management of the assets, particularly investments, may be subcontracted to an investment advisor on an arm’s-length basis.

- Over time, tranches of the FLP interest are gifted to family members as the controlling shareholder sees fit, with any capital gains / estate taxes mitigated by the overarching offshore trust structure.

- The controlling shareholder / General Partner retains control over income and capital distributions by virtue of the Partnership Agreement. Although a pro-rata profit and capital-sharing arrangement may be appropriate, it is not a necessity and this may be restricted by the Partnership Agreement, particularly in the early years.

- The underlying transparent nature of the FLP lends itself well to individual tax planning by the partners. The commercial rationale of the structure may also lend more credence to tax authorities than pure trust structures.

- Individual partners can add further structuring to protect against tax charges in their jurisdiction of residence.

Application to UK Residents

As noted above, FLPs are particularly attractive for UK residents since the changes to the UK trust tax regime were introduced, which have made it difficult to settle assets on trust in a tax-effective way.

UK Resident Non-Domiciliary

A UK resident non-domiciliary controlling an international business or businesses will again often have immediate family members residing in many jurisdictions throughout the world. An example of this is the established businessperson who has recently taken up UK residence under a Tier 1 Investor Visa.

The non-domiciliary will have the opportunity, during their first 15 years of residence in the UK, to settle offshore trusts without any UK Inheritance Tax (IHT) charges. Such a move is normally advised since, after that point, the individual becomes deemed domiciled for IHT purposes, which has the effect of bringing the worldwide estate into the UK IHT net.

For such individuals, the FLP has become an additional structuring vehicle employed when succession planning becomes an important consideration. Providing proper structuring has been undertaken, it will be possible for this succession process to be effected free of capital gains and inheritance taxes.

UK Resident Domiciliary

A UK domiciliary cannot generally settle assets on trust without incurring an immediate IHT charge (with the exception of small amounts settled within the IHT nil rate band). For this reason, the FLP can become a complete replacement for traditional trust structures as an alternative means to pass down wealth in families.

In particular, the contribution of assets to the FLP in exchange for a commensurate partnership interest will not trigger any IHT charges as there will be no diminution in the value of the transferor’s estate. Other tax advantages for a non-domiciliary as compared with a trust include:

- The gift of an interest in the FLP to future generations is not a chargeable lifetime transfer for IHT but a transfer which is entirely exempt providing the donor survives seven years from the date of gift (i.e. what is known as a Potentially Exempt Transfer or PET).

- No 10-yearly inheritance tax charge.

- Possible capital gains holdover relief available on transfer of shares or other assets to the FLP.

- Transferor retains an interest without being deemed to have a “reservation of benefit” over assets given away.

- Possibility of utlilising basic rate tax bands of family members.

Summary

The Family Limited Partnership provides a flexible and controlled way to manage succession planning within wealthy families, particularly where family members are resident in multiple jurisdictions. Such structures may complement or serve as an alternative to traditional trusts and foundations.

The tax transparency of the FLP gives the advantage of a zero tax presence; instead, individual partners can structure their interests to ensure minimum tax leakage according to their jurisdiction of residence.

For UK residents, the FLP is particularly attractive in enabling succession planning without the punitive tax charges sometimes associated with trusts.